Photo: Sony Pictures

June 29, 2023

- S&P 500 futures rise, ignoring hawkish Fed.

- US Q1 GDP rises 2.0%, more than expected.

- US dollar rallies into month end.

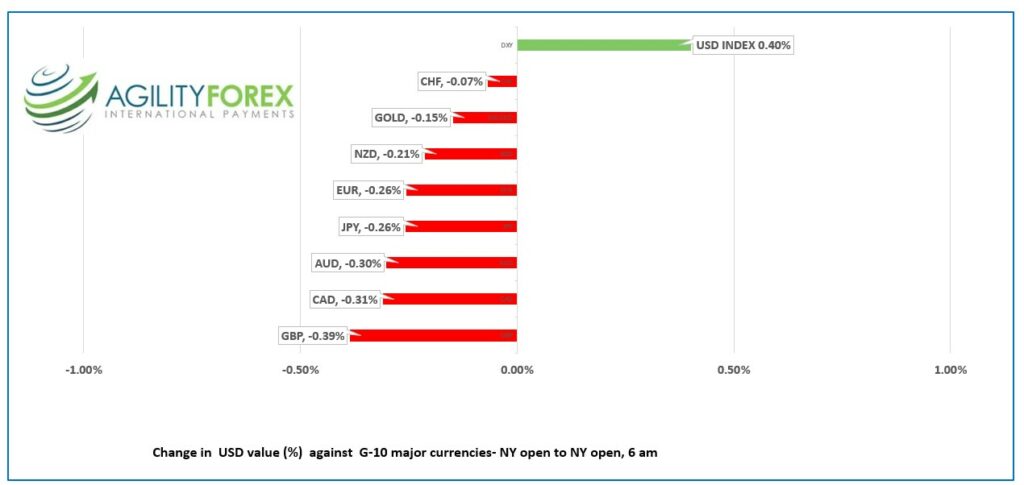

FX at a glance

Source: IFXA Ltd

USDCAD Snapshot: open 1.3267-71, overnight range 1.3245-1.3277, close 1.3259

USDCAD rallied yesterday against a backdrop of downgraded Bank of Canada rate hike expectations for July, hawkish comments by Fed Chair Jerome Powell suggesting higher rates for a longer period, and stop loss buying on the break of resistance at 1.3190 and 1.3230.

The weaker-than-expected headline inflation data overshadowed the more important BoC inflation indicators, which remained well above the BoC’s 2.0% target.

Tiff Macklem and his colleagues have spent a lot of time explaining the lags between policy action and its impact on the economy. Tiff recently said that these impacts could take up to two years to be seen in the data. However, his actions seem to contradict his comments, as he is reacting to market data similar to how a public company CEO reacts to quarterly earnings statements.

WTI oil prices are rangebound and are bouncing in a range of $67.13-$70.13, which has contained price action for the past week.

USDCAD Technical Outlook

The USDCAD technicals are bullish while trading above 1.3240, looking for a decisive break above 1.3280 to extend gains to 1.3350. A move above the 1.3350 level points to a retest of the 100 and 200-day moving averages at 1.3493 and 1.3412, respectively.

However, the downtrend from the 1.3855 March peak is intact while prices are below 1.3550.

For today, USDCAD support is at 1.3240 and 1.3180. Resistance is at 1.3280 and 1.3330.

Today’s range 1.3220-1.3320.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

Wall Street is ignoring the hawkish rhetoric coming out of Sintra, Portugal. A group of central bankers has commented on sticky inflation, necessitating higher interest rates for a longer period.

Yesterday, Fed Chair Jerome Powell suggested that rate hikes were possible in July and September. He claimed, “Although policy is restrictive, it may not be restrictive enough, and it has not been restrictive for long enough.”

The theme did not continue in Asia as the Nikkei 225 index closed with a minimal 0.12% gain, while Australia’s ASX 200 remained unchanged. However, European bourses are more upbeat. The French CAC 40 index is up 0.61%, the German Dax has gained 0.19%, and the UK FTSE 100 index is down 0.36%. as of 5:45 am PDT.

S&P 500 futures have gained 0.20%, down from their session peak after the modest rise in the US 10-year Treasury yield, which increased from 3.71% at the close to 3.80%%, in the wake of the strong US GDP and jobless claims data.

Wall Street traders do not appear to agree with the Fed’s outlook for US rates, preferring to believe that the Fed is very close to ending the rate hike cycle. S&P 500 futures jumped and are up 0.35% post-GDP and jobless claims reports.

FX traders are keenly focused on the prospect of higher US rates, and the greenback is trading higher, post-data.

The FX focus was rewarded this morning. The US economy was far stronger than expected with Q1 GDP rising 2.0% y/y compared to the forecast for a 1.3% increase. Weekly jobless claims dropped 26,000 to 239,000, supporting the Fed’s view of two more rate hikes.

EURUSD dropped from the top of its 1.0882-1.0941 range, to 1.0905 in the wake of the US data. However, EURUSD is underpinned by higher than expected German CPI which rose 6.4% y/y in June (forecast 6.3%). Harmonized CPI rose 6.8% y/y vs forecast for a 6.7% increase and well above the 6.3% reading in May.

GBPUSD consolidated yesterday’s losses in a 1.2616-1.2665 range. Yesterday, Bank of England Governor Andrew Bailey seemed to push back against expectations for significantly higher rates, saying, “They’ve got a number of further increases priced in for us. My response to that would be: ‘Well, we’ll see.'” The GBPUSD technicals are bullish above 1.2600.

USDJPY dropped from its overnight peak of 144.69 to 144.14 then rebounded to 144.70 as the US 10-year yield jumped to 3.80% from 3.75 before the data. The story remains the same. The hawkish Fed and dovish BoJ monetary policy outlooks are fueling the rally, and the only resistance is from “verbal” intervention.

AUDUSD traded in a 0.6597-0.6629 band and continues to trade defensively due to the hawkish Fed outlook and the dovish RBA stance. Prices bounced from the low after Australian retail sales rose 0.7% m/m, compared to the expected increase of 0.1%.

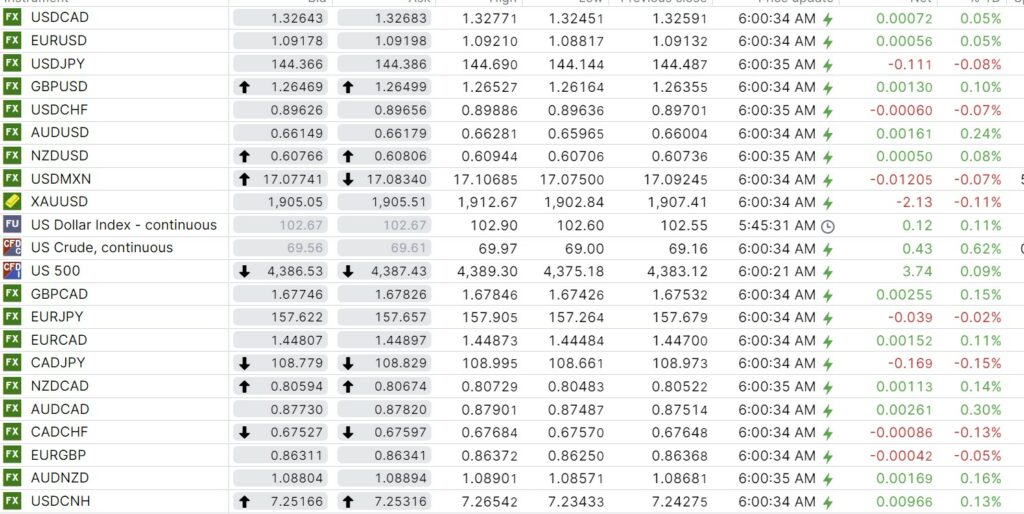

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

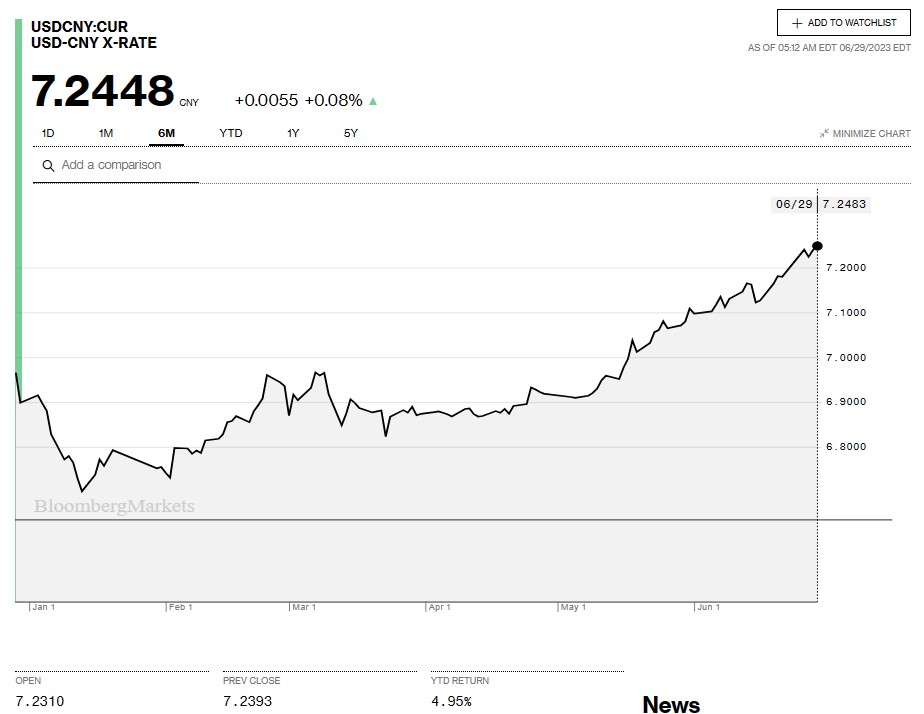

China Snapshot

Bank of China Fix: 7.2208, previous 7.2101

Shanghai Shenzhen CSI 300 fell 0.49% to 3821.84.

Chart: USDCNY 6 month

Source: Bloomberg