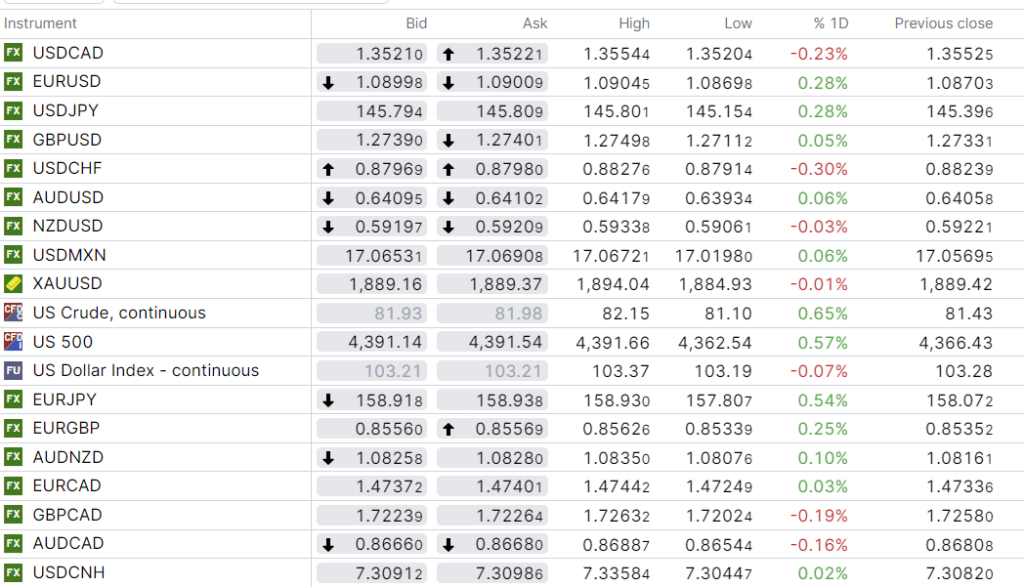

Source: IFXA/R

USDCAD Snapshot: open: 1.3520-24, overnight range: 1.3497-1.3554, close 1.3552.

USDCAD continues to consolidate its gains after breeching resistance in the 1.3490-1.3500 area. The risk that the Bank of Canada hikes rates by 25 bps at its September 6 meeting in response to stronger than expected economic data is acting as a drag on topside moves. Nevertheless, it is the Fed that is driving the bus.

WTI oil prices are steady and close to the top of its $81.10-$82.19 trading range due to the mixed US dollar performance overnight and speculation that the worst of the hedge fund unwind of long crude positions is over. Prices continue to be supported by tight supply but concerns about China’s economic growth is limiting gains.

Canada new house price data is on tap.

USDCAD Technicals

The intraday USDCAD technicals are modestly bearish while prices are below 1.3550 and looking for a break below support in the 1.3490-1.3505 area to extend losses to 1.3470.

Longer term, the USDCAD uptrend channel from the beginning of August is looking to extend gains to 1.3590 while above 1.3470. A topside break would target 1.3660.

For today, USDCAD support is at 1.3490 and 1.3460. Resistance is at 1.3570 and 1.3610. Today’s range 1.3470-1.3550.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

Summer reruns are a mainstay of the major television networks, and it would seem, the financial press, ahead of the Kansas City Fed’s annual Jackson Hole Symposium. Once again, Fed Chair Jerome Powell headlines an array of central bank governors and presidents delivering remarks.

Mr. Powell is expected to acknowledge that inflation is heading lower but say it is still too high. He will reiterate that interest rate moves will be data-dependent and may remain at elevated levels for longer than expected. Nothing new there.

The Fed has made three major policy announcements at this symposium, which is why this bun-fest gets so much attention. The first occurred in 2010 when Ben Bernanke signaled the second round of quantitative easing (QE). The second was in 2012, with Mr. Bernanke hinting at more monetary stimulus which turned out to be QE3. The third time was when Jerome Powell used the Jackson Hole podium to unveil “average inflation targeting.”

That means the odds of a major policy announcement on Friday are just 25%, but even so, talk of “what ifs” will ensure a cautious trading week ahead.

China’s quasi-surprise rate cut that lowered the 1-year Loan Prime Rate by 0.10 bps to 3.45% from 3.55% was met with a collective “meh” as it was smaller than expected. Traders were also disappointed because the PboC left the 5-year LPR unchanged at 4.20%. UBS cut its China GDP growth forecast for 2023 to 4.8% from 5.2%, joining a slew of major investment banks that have downgraded Chinese growth. Beijing deflected attention from the negative news by ramping up its air and naval harassment of Taiwan.

EURUSD drifted in a 1.0870-1.0914 range and is trading in an uninspiring session. Germany’s July PPI index was lower than expected, falling 1.1% compared to the forecast of a 0.2% m/m decline. Topside moves were curtailed by the increase in US Treasury yields.

GBPUSD traded unenthusiastically in a 1.2711-1.2765 range with traders content to not get involved ahead of Fed Chair Powell’s speech on Friday. UK house prices fell 1.9% in August.

USDJPY marched higher and is at the top of its 145.15-145.98 range in the wake of the US 10-year Treasury yield climbing to 4.30%.

AUDUSD is directionless in a 0.6393-0.6421.band but trading with a negative bias due to China’s economic woes.

There are no US economic reports today.

Top of Form

FX high, low, close

Source: Saxo Bank

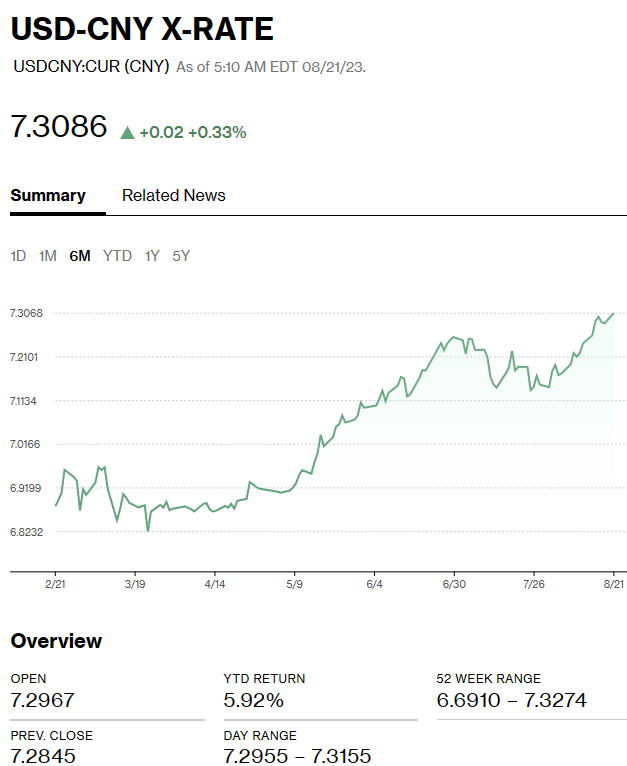

China Snapshot

Bank of China Fix: today 7.1987, expected 7.2893, previous 7.2006.

Shanghai Shenzhen CSI 300 fell 1.44% to 3729.55.

PboC cuts 1-year Loan Prime Rate (LPR) to 3.45% from 3.55%. -year LPR unchanged at 4.2%.

Chart: USDCNY 1 month

Source: Bloomberg