September 20, 2024

- Option expiries suggest a messy morning.

- BoJ and PBoC leaver rates unchanged.

- US dollar remains on the defensive.

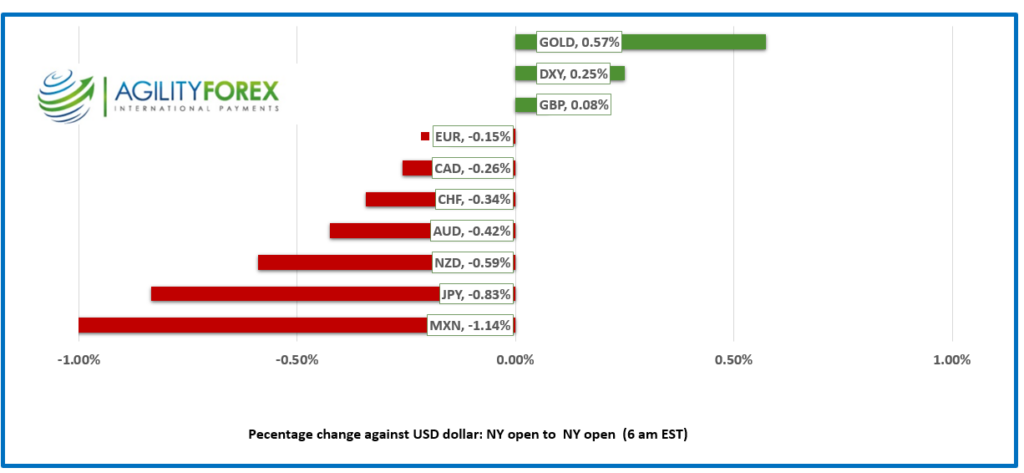

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3573, overnight range 1.3553-1.3577, previous close 1.3560

USDCAD has bopped and weaved on ever-shifting US dollar sentiment. USDCAD had limited downside following the Fed’s 50 bp rate cut because BoC Governor Tiff Macklem hinted that a similar move was in the cards in an interview last Sunday. Unfortunately, Mr Macklem did not speak about the outlook for Canadian monetary policy in his speech today. He merely chatted about the potential long term impact of AI on productivity, inflation and economic growth.

Canada Retail Sales rose 0.9% in July m/m in July compared to -0.3% in June, while Retail Sales, ex-autos rose 0.4% (previous 0.3%). The retail sales headline growth appears strong, but underlying sector weaknesses suggest the data is not as robust as it seems. The overall increase was driven by gains in motor vehicle sales, while key sectors like gasoline and building materials saw declines, masking broader weaknesses.

Deflation risks are rising. Industrial Product Prices decreased by 0.8% m/m in August (previous -0.1%) while Raw Materials Prices fell 3.1% m/m (previous 0.7%)

WTI oil prices are firmer, rising from 70.50-71.20 due to increased Middle East tensions.

USDCAD may see heightened volatility around the 10:00 am option expiry window when $2.4 billion of strikes between 1.3570 and 1.3585 roll off.

USDCAD technicals

The intraday USDCAD technical are undecided. The downtrend from August 8 comes into play at 1.3610 while the uptrend from August 28 is intact above 1.3530. A break either side of these levels suggests a 100 bp move is likely.

Longer term the USDCAD 200 day moving average in the 1.3585 area is acting as a pivot while the 100 day moving average at 1.3685 caps gains.

For today, USDCAD support is at 1.3530 and 1.3510. Resistance is at 1.3590 and 1.3620.

Today’s Range 1.3510-1.3610

Chart: USDCAD daily

Source: Investing.com

Let the Easing Cycle Begin (for some)

The Fed kicked off its highly anticipated easing cycle on Wednesday with a 50 bp rate cut, which also managed to put an end to accusations that policymakers were “behind the curve.” Now traders are demanding to know “what’s next?” The dot-plot projections suggest that there will be another 75 bps of rate cuts by year-end. Things are different in Asia and the UK. The BoJ, PBoC, and the BoE all left their policy rates unchanged. So, who is behind the curve now?

Something Wicked This Way Comes.

Market volatility could take a nasty turn today. It is the quarterly “Triple-Witching” day, and $5.3 trillion of stock, index, and ETF options expire. FX markets are not immune. EURUSD has $2.7 billion of 1.1100 strikes maturing, GBPUSD has $1.8 billion of 1.3250-60 strikes expiring, and AUDUSD has $1.1 billion of 0.6790-00 strikes rolling off.

EURUSD

EURUSD is choppy but rangebound in a 1.1152-1.1182 range, with prices supported by general US dollar weakness. The uptrend channel from the beginning of August is intact while prices are between 1.1030 and 1.1330.

GBPUSD

GBPUSD is at the bottom of its 1.3272-1.3341 overnight range following Thursday’s Bank of England decision to leave rates unchanged at 5.0%, and Governor Bailey’s hawkish comments. Mr. Bailey said that policymakers must be careful not to lower interest rates too quickly or too much. Traders decided he meant that rates would be unchanged at the November meeting as well. UK Consumer Confidence took a hit and dropped to -20 from -13 in August. GfK blamed the drop on the UK government’s plans to hike taxes.

USDJPY

USDJPY dropped then popped in a lively overnight session with prices bouncing in a 141.74-143.96 band. A dovish BoJ monetary policy meeting was behind the volatility. The BoJ left its benchmark rate unchanged at 0.25%, but it was dovish-sounding comments from Governor Kazuo Ueda that sparked USDJPY gains. He suggested that the BoJ is in no hurry to change monetary policy due to global economic uncertainties.

AUDUSD and NZDUSD

AUDUSD consolidated its post-FOMC gains in a 0.6801-0.6830 range and is trading at its session low in NY. Prices got a bit of support from USDCNY losses, but that support faded, and traders are looking ahead to Tuesday’s RBA meeting.

NZDUSD traded like its antipodean cousin in a 0.6225-0.6260 range and is poised to end the week with a 1.6% gain.

USDMXN

USDMXN surged from 19.2614 to 19.4930 due to self-inflicted wounds. The governments planned judicial reforms raises concerns about how impartial judges will be in disputes between investors and the government. Some analysts worry about how the reforms will impact the review of the United States-Mexico-Canada (USMCA trade agreement in 2026. USDMXN snapped the week-long downtrend channel with the move above 19.3330 and is targeting 19.8530.

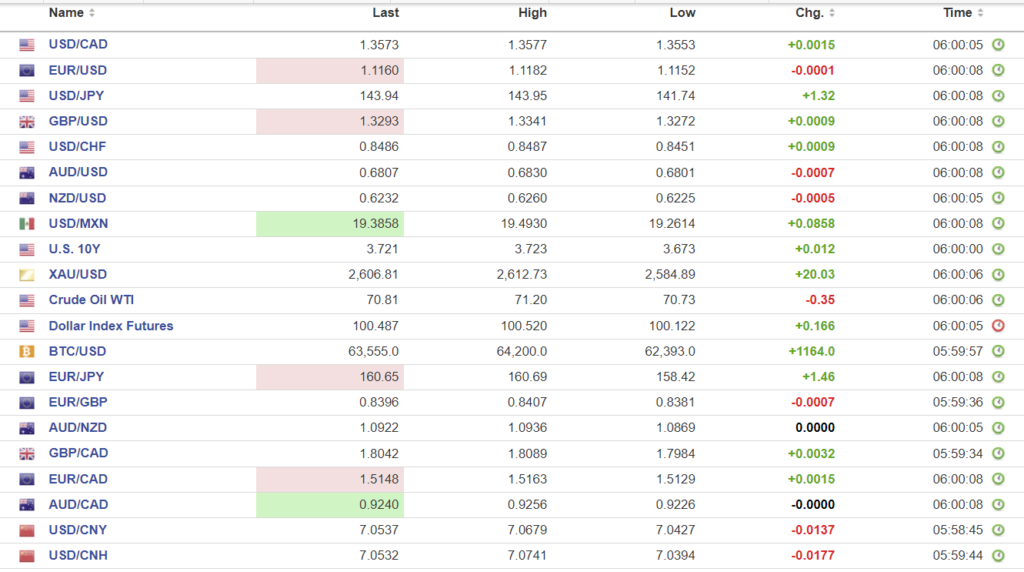

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0644 vs exp. 7.0637 (prev. 7.0983))

Shanghai Shenzhen CS! 300 rose 0.16% to 3201.06.

PBoC leaves rates unchanged despite Fed’s 50 bp rate cut. The one-year loan prime rate (LPR) stayed at 3.35%, while the five-year LPR was unchanged at 3.85%.

There are reports that Chinese State banks were buying USDCNY to help slow the pace of yuan gains.

Authorities are considering removing some home purchase restrictions which would allow non-local buyers to purchase property in Shanghai and Beijing, They are also considering removing the distinctions between first and second property purchases for mortgages .

Chart: USDCNY and USDCNH

Source: Investing.com