April 2, 2024

- Data supports Fed rate cut patience.

- JOLTS Job openings report today.

- US dollar recoups some losses.

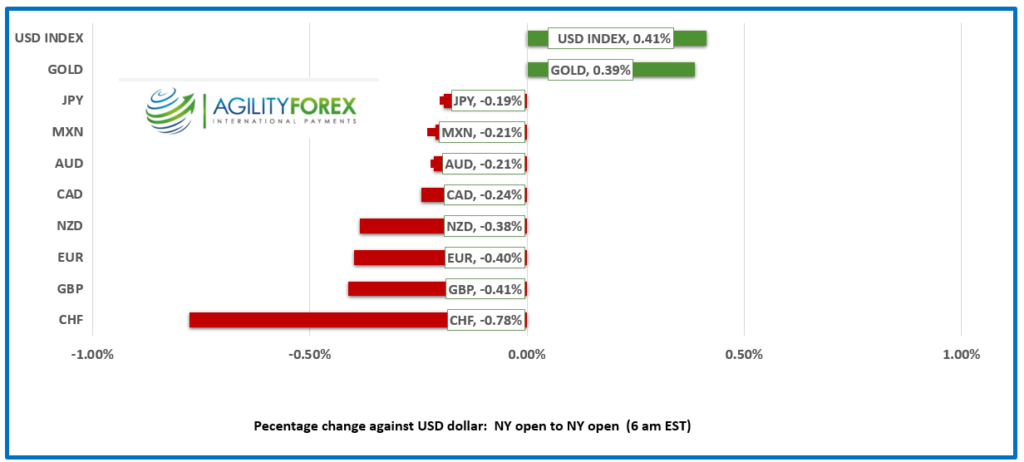

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3560-64, overnight range 1.3555-1.3585, close 1.3573

USDCAD rallied alongside broad US dollar demand after yesterday’s US ISM Manufacturing report, but the rally petered out in front of resistance in the 1.3600 area.

The Bank of Canada’s quarterly Business Outlook Survey will not give policymakers any encouragement to lower interest rates in the near term. The Survey showed that wage growth was still elevated, and consumer inflation expectations were little changed in the short-term.

WTI oil traded with a bit of a bid in $83.86-$85.44 range due to ongoing geopolitical tensions and from news that Ukrainian drones attacked a Russian oil terminal .

USD/CAD Technicals

The intraday USDCAD technicals are moderately bearish below 1.3590, looking for a break below 1.3550 to target 1.3520. A break, above 1.3600 targets 1.3630 and 1.3660. The reality is USDCAD is rangebound in a 1.3500-1.3600 band and will likely remain that way until after Friday’s US and Canadian employment reports.

The longer term technicals are unchanged with the uptrend line from the end of December/beginning of January guiding prices higher while above 1.3480.. The 100 and 200 day moving averages converge in the 1.3495 and 1.3485 areas, respectively, which will also be support.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3590 and 1.3620. Today’s range is 1.3510-1.3590.

Chart: USDCAD 4 hour

Source:Investing.com

Patience is a virtue.

The data is confirming what Fed officials have been saying: “There is no hurry to cut rates.” Bond traders appear convinced. They sold bonds and drove the US 10-year yield up to 4.35% this morning from a low of 4.19% yesterday. Equity traders are not convinced, but global stock indexes remain elevated.

Yesterday, US ISM Manufacturing PMI popped into expansion territory for the first time since September 2022, with a 50.3 reading for March. However, manufacturers were paying more for supplies as the Prices Paid component rose to 55.8 from 52.5. From the Fed’s perspective, rebounding manufacturing and higher prices mean there is no need to trim interest rates.

Gold Shines

Gold prices continued to rally and rose to $2266.80 from $2187.43 on Thursday thanks to heightened geopolitical tensions. Israel took out a terrorist compound in Damascus. Iran claims it was their consulate, which is really admitting that Israel is correct. Meanwhile, Ukraine launched another attack on Russia’s oil infrastructure.

Jobs Data Due

The JOLTS Job Openings data is expected to show that job openings declined in March, which, if correct, is an indication that the labor market is normalizing.

EURUSD

EURUSD see-sawed in a 1.0724-1.0756 range and is at the top of that band in NY. Eurozone and German Manufacturing PMI data were disappointing as it continue to show a weak manufacturing sector, although it is inching higher.

GBP

GBPUSD consolidated yesterday’s losses in a 1.2539-1.2577 range with prices pressures due to divergent Fed and UK interest rate paths. The Bank of England turned neutral to dovish at their latest meeting while the Fed is content to sit on the sidelines. GBPUSD technicals are pointing to further gains while prices are above 1.2540.

USDJPY

USDJPY traded defiantly in a 151.50-151.80 range with traders ignoring more verbal intervention by the Finance Minister and other officials.

AUDUSD and NZDUSD

AUDUSD attempted to recoup yesterday’s losses and traded firmer in a 0.6483-0.6512 range despite dovish RBA minutes. The minutes confirmed the central bank’s shift to a neutral stance; the board did not even consider hiking rates. TD inflation data was mixed. March inflation rose 0.1% m/m (previous -0.1%) while the year-over-year number rose just 3.8% vs. 4.0% previously.

NZDUSD traded in a 0.5943-0.5960 range, with prices weighed down by last week’s comments by RBNZ Governor Adrian Orr. He suggested that RBNZ rates have peaked and that it would soon be time to lower them.

USDMXN

USDMXN popped to 16.6790 yesterday after the US ISM data, then drifted lower in a 16.5922-16.5930 range overnight. Last week, Mexico’s Finance Secretary left its 2024 GDP growth range unchanged at between 2.5-3.5% for 2024 while forecasting inflation at 3.8% by year-end.

The US data calendar has factory orders and JOLTS Job Openings

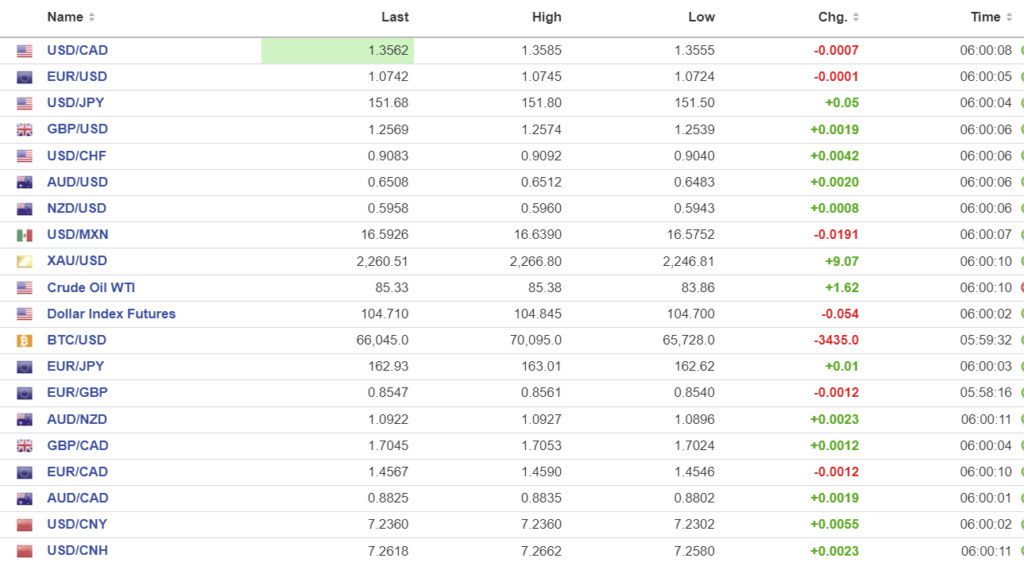

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: mid-point at 7.0957 vs exp. 7.2433 (prev. 7.0938).

Shanghai Shenzhen CSI 300 fell 0.42% to 3580.68.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com