Picture: wannapik.com/vector/12795

- FX and Equity markets jumpy ahead of US holiday week

- Canada retail Sales better than expected

- US dollar rallies without obvious catalyst

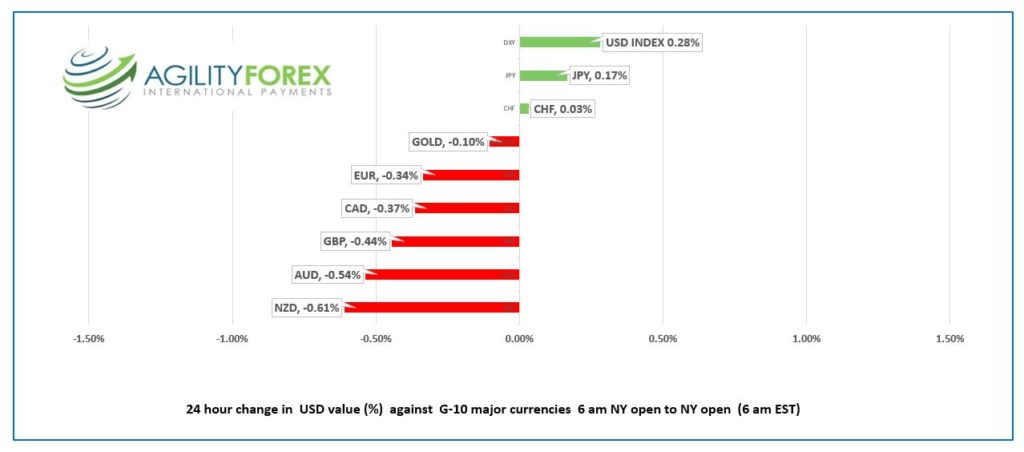

FX at a Glance:

Source: IFXA Ltd/RP

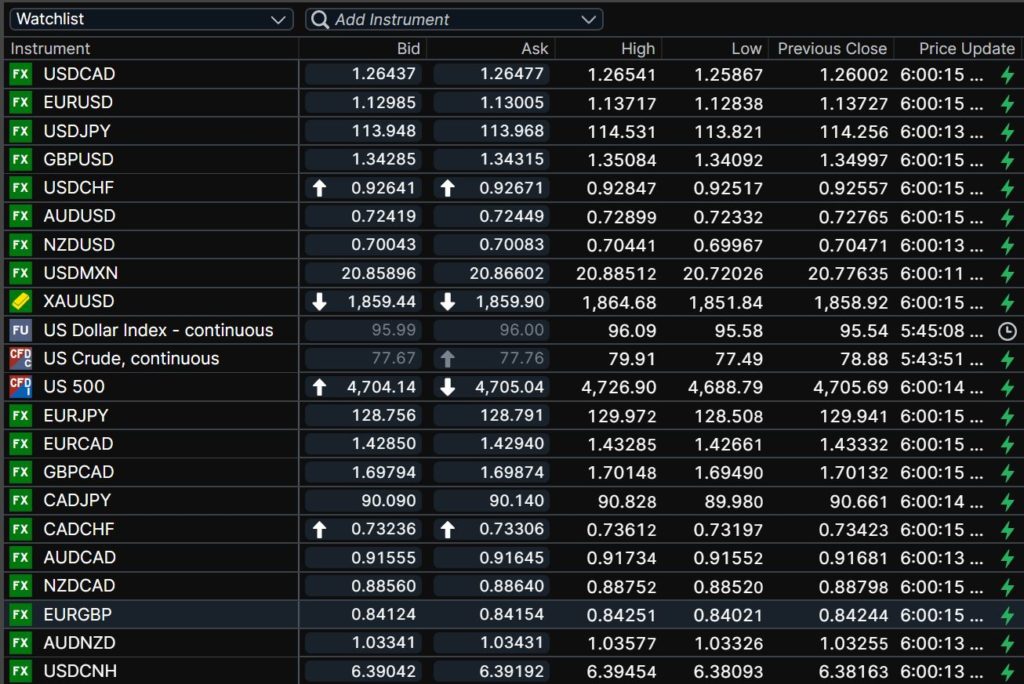

USDCAD Snapshot Open 1.246-50, Overnight Range 1.2587-1.2660, Previous close 1.2600

USDCAD drifted sideways in Asia then shot higher in Europe on the back of, well nothing. USDCAD gains followed on the heels of widespread US dollar demand that sank the G-10 majors except JPY.

The surge in the US dollar boosted the US dollar index to 96.09 from 95.58 at Thursday’s NY close, but Treasury yields were not the catalyst. The US 10-year Treasury yield dipped to 1.541% in early NY from an overnight peak of 1.60%

The US dollar rally exacerbated a drop in WTI oil which fell from $79.91 in Asia to $77.49 just before NY open. Oil traders continue to be unnerved by news that the US and Chinese presidents discussed releasing Strategic Petroleum reserves.

Canada September Retail Sales fell 0.6% m/m compared to the consensus forecast for a 1.7% drop. Statistics Canada noted that Q3 retail sales rose 2.7% q/q. they also predict that October retail sales will rise 1.0%.

USDCAD will continue to trade erratically as liquidity deteriorates into next week’s US Thanksgiving holiday.

Technical view: The USDCAD technicals are bullish. Prices have been grinding higher since posting a low of 1.2285 on October 25 but the rally stalled at 1.2654 overnight, just below the 61.8% Fibonacci retracement level of the September-October range which is in the 1.2660 area. A topside break will extend gains to 1.2750, while a move below 1.2580 targets 1.2500.

For today, USDCAD support is at 1.2610 and 1.2580. Resistance is 1.2660 and 1.2710. Today’s range 1.2590-1.2660

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The weekend is looming, and traders are as jumpy as a rabbit in a stew pot. The increasing numbers of COVID-19 cases across Europe and the WHO reporting a 5% rise in deaths sparked a harsh and somewhat regressive reaction in various countries.

Austria banned unvaccinated people from going outside. Germany is adopting a similar but less stringent policy to Austria. They banned unvaccinated people from public places, including concert halls and restaurants. Sweden requires a health pass to attend events of more than 100 people. The Czech Republic is also banning the unvaccinated from public events.

Traders were also wary ahead of the weekend due to the risk that Joe Biden would announce a new Fed governor.

The major Asia equity indexes closed higher except for Hong Kong’s Hang Seng Index, which lost 1.07% partly because Alibaba released a weak earnings report. European bourses opened higher, but all are in negative territory. DJIA and S&P 500 futures are down 0.54%, and 0.23% as of 6.50 am ET. Gold prices are a tad higher from Thursday’s close, while WTI oil is down about 1.2%. US 10-year Treasury yields dropped to 1.541%.

EURUSD inched lower in Asia, falling from 1.1372 to 1.1350 just before Europe opened. Then the bottom fell out, and EURUSD plunged to 1.1283. Coronavirus fears and more dovish comments from ECB President Christine Lagarde weighed on the currency. Ms Lagarde repeated concerns about “premature tightening” and that inflation wiould retreat from current levels. Traders ignored news that the Eurozone posted a trade surplus of €19 billion in September, and German PPI rose 3.8% m/m in October. EURUSD will test 1.1170 on a break of 1.1260.

GBPUSD lost a big figure, mirroring EURUSD price action. GBPUSD fell from 1.3508 to 1.3409 but has since bounced to 1.3438. Traders were not impressed with news UK retail sales rose 0.8% m/m in October and instead tracked broad US dollar sentiment. UK trade negotiator David Frost reported “significant gaps” between EU and UK over the Irish border and that Article 16 is still on the table. GBPUSD remains bearish below 1.3500.

USDJPY dropped to 113.82 from 114.53 due to the retreat in US Treasury yields. Japanese inflation was weaker than expected at 0.1% (forecast 0.5%)

AUDUSD and NZDUSD were steady in Asia but plunged in Europe due to broad US dollar demand

There are no US economic releases of note, but Fed Vice Chair (and insider Trader) Richard Clarida is speaking.

Chart of the Day: EURUSD

Source: Yahoo Finance.com

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

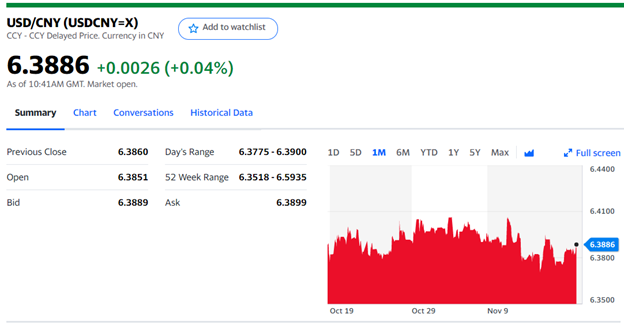

China Snapshot

Today’s Bank of China Fix 6.3825 Previous 6.3803

Shanghai Shenzhen CSI 300 rose 1.06% to 4,890.06

China considering cutting some taxes and fees to around CNY 500 billion

US and China swap prisoners but don’t call it a swap, just a coincidence

Biden considering a diplomatic boycott of Beijing Olympics

Chart: USDCNY 1 month

Source: Yahoo Finance