January 22, 2024

- It’s a big week for central bank meetings.

- BoJ expected to leave rates unchanged tomorrow.

- US dollar opens mixed-CAD outperforms.

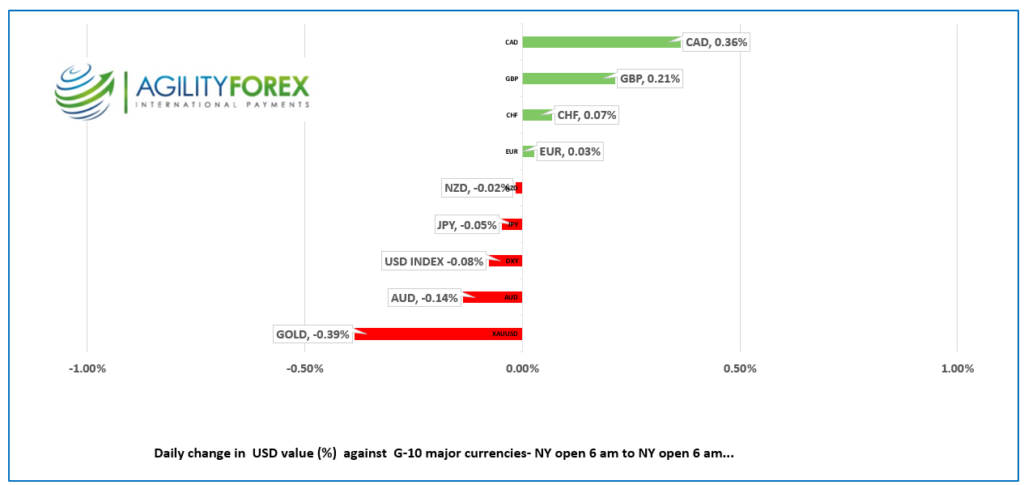

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3422-26, overnight range 1.3414-1.3447, close 1.3430.

USDCAD is under pressure due to concern that the Bank of Canada (BoC) will adopt a hawkish bias to its interest rate outlook at Wednesday’s meeting. That’s because the Banks own measures of inflation, CPI-trim and CPI median Core rose in December. This meeting also includes the quarterly monetary policy report. The risk of a spring rate cut has lowered and that is weighing on USDCAD.

Oil prices are neither here nor there. The continue to bounce in a $71.00-$75.00/barrel range and USDCAD traders are ignoring the moves.

USDCAD Technicals:

The intraday USDCAD technicals are bearish below 1.3450, looking for a breach of 1.3405 to extend losses to 1.3360. A move below 1.3460 targets 1.3380. A move above 1.3460 suggests a retest of 1.3510.

For today, USDCAD support is at 1.3405 and 1.3370. Resistance is at 1.3460 and 1.3480.0. Todays range 1.3410-1.3460.

Chart: USDCAD daily

Source: DailyFX

G-10 FX recap

It wasn’t a good weekend for Florida Governor Ron DeSantis or Buffalo Bills fans. The governor, who once referred to Trump as the “orange menace” while describing him as a failed leader, had a “come to Jesus” moment after he only got 21.2% of the Iowa primary votes compared to Trump’s 51%. Not only did he quit his presidential bid, but he also realized the orange menace was really the orange savior and endorsed him. Hallelujah!

The Buffalo Bills fared worse. Placekicker Tyler Bass channeled his inner Scott Norwood and missed a 44-yard, game-winning field goal.

Traders are cautious ahead of the central bank monetary policy meetings this week. The BoJ is tomorrow, the BoC on Wednesday, and the ECB meets Thursday. In addition, the US unloads a lot of data on Thursday, including Q4 GDP.

Asian equity markets finished on a firm footing, undeterred by the Chinese stock market performance. Australia’s ASX rose 0.75% and Japan’s Nikkei 225 index gained 1.62%. Chines stocks tanked with the in Hong Kong Hang Seng index falling 2.27%.

European bourses are in positive territory but off their bests levels. The German Dax has edged out the French CAC 40 index for the lead with a gain of 0.35% vs 0.34% for the CAC-40. S&P 500 futures have gained 0.34 The US 10-year Treasury yield has slipped to 4.08% from 4.12% earlier.

EURUSD is adrift inside a 1.0880-1.0910 range. The single currency is supported by a three month uptrend while prices are above 1.0840 and by is underpinned by ECB policymakers downplaying the odds of an early rate cut.

GBPUSD has a bullish bias as it nears the top of its overnight 1.2687-1.2731 range. Sterling is seeing demand while prices are above 1.2620 as analyst suggest Bank of England rate cuts will be later and less than previously expected.

USDJPY is trading nervously in a 147.74-148.31 range and of tomorrow’s Bank of Japan monetary policy meeting. Some traders fear that the yield curve control cap could be tweaked due to recent weaker than expected inflation data which reduced the urgency for policymakers to tighten policy.

AUDUSD traded negatively in a 0.6581-0.6614 range due to falling stock market prices in China. The steep equity losses in Hong Kong and mainland China underscored the weakness of the Chinese economy, which is bad news for Australia, as it is its largest trading partner.

There is no US data of note today.

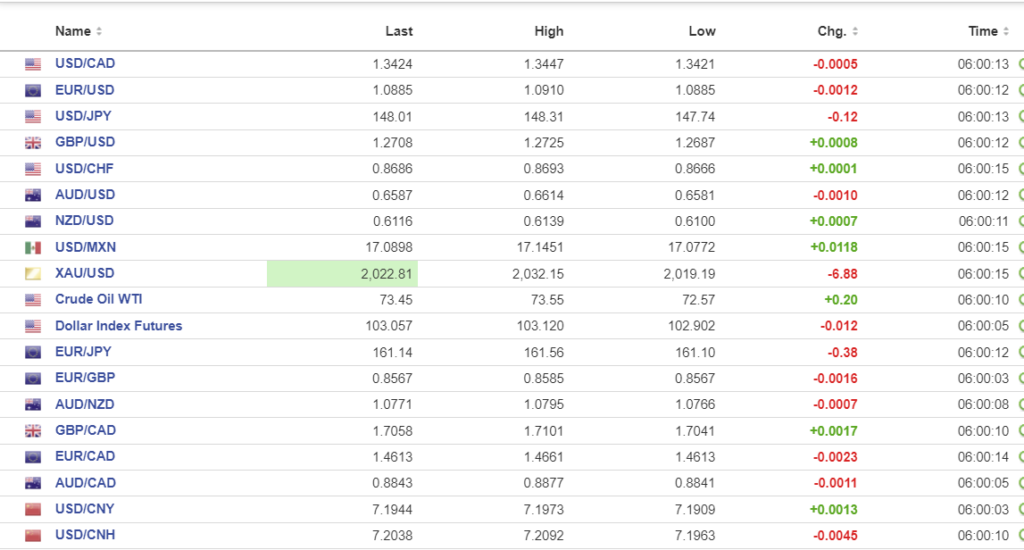

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1105, previous 7.1167.

Shanghai Shenzhen CSI 300 fell 1.56% to 3218.90.

China leaves 1 and 5 year Loan Prime Rate (LPR) unchanged at 3.45% and 4.20% respectively.

Chart: USDCNY and USDCNH daily

Source: Investing.com