Source: clipground.com

- Canada gains 153,700 jobs; US NFP well below estimates

- Risk sentiment improves, global equity indexes rise

- US dollar opens higher across the board, plunges after NFP data

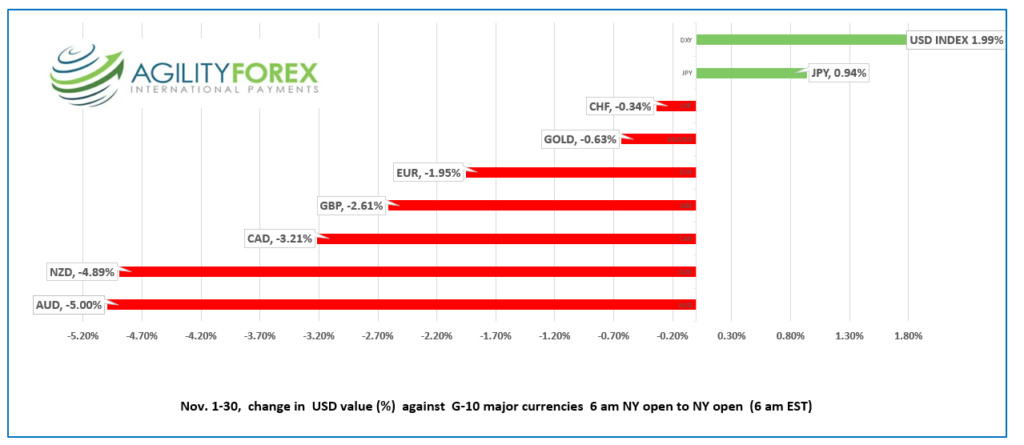

FX at a Glance for November

Source: IFXA Ltd/RP

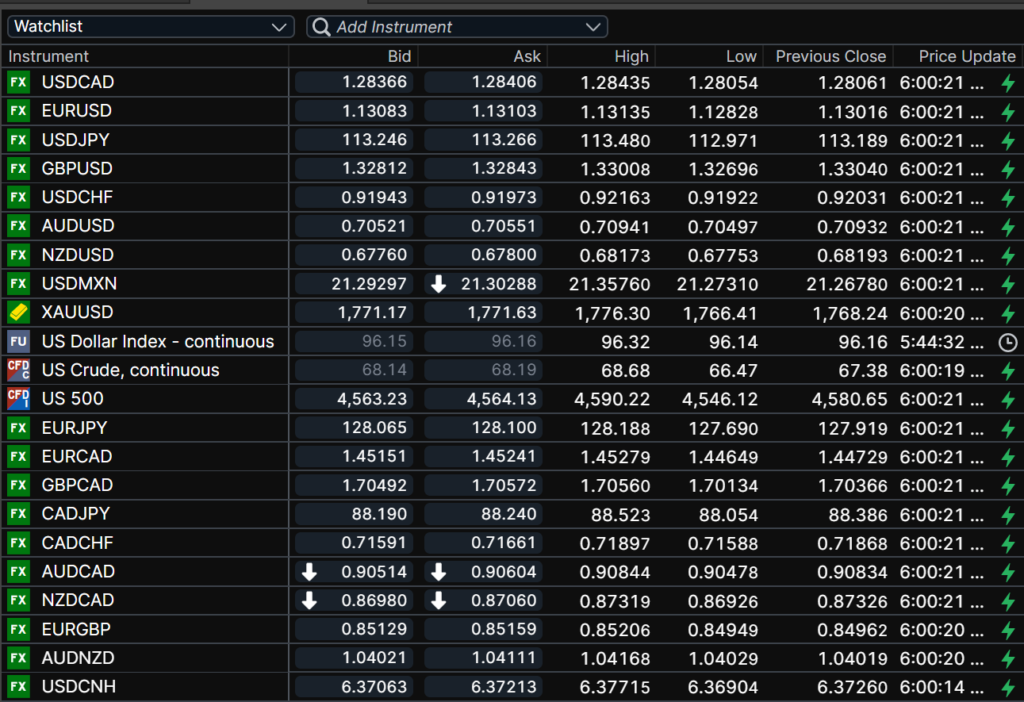

USDCAD Snapshot Open 1.2837-41, Overnight Range 1.2764-1.2844, Previous close 1.2806

USDCAD plunged from 1.2840 pre-employment data to 1.2764 immediately after Stats Canada reported 153,700 new jobs in November and the unemployment rate dropped to 6.0% from 6.7%. It is a solid report with private sector employment rising 107,000. Total unemployment fell to 1.24 million but remained 98,000 higher than in February 2020

Source: Statistics Canada

The employment data helps to shelter USDCAD from the hawkish Fed outlook as Canadian interest rates may rise sooner than those in the US. The Bank of Canada Monetary policy is next week and today’s employment data combined with inflation that is well above the Bank’s target, raises the risk for a hawkish statement. However, the Omicron virus may temper their remarks.

USDCAD deviated from tracking the rise and fall of oil prices in overnight action. WTI climbed steadily, rising from $66.47/b in Asia to $68.68/b in Europe before drifting to $68.25 in early NY trading. The oil price rally was another example of “sell the rumour, by the news.” WTI slid ahead of the delayed Opec/Russia announcement about January production. The cartel agreed to continue with their program of increasing production by 400,000 bpd.

Technical view: The daily USDCAD technicals are bullish above 1.2750 which is the uptrend line form mid-November, looking for a break above 1.2850 to extend gains to 1.3000. The 1.3000 area is thick with resistance from previous tops and bottoms suggesting it will not be easy to overcome. A break below 1.2700 will alleviate the upward pressure and suggest 1.2550-1.2850 consolidation.

For today, USDCAD support is at 1.2750 and 1.2710. Resistance is at 1.2850 and 1.2890. Today’s Range 1.2740-1.2720

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Today’s US nonfarm payrolls report missed big time. Interest rate hike hawks were sharpening their talons in anticipation of 550,000 new jobs. Instead, only 210,000 jobs were added. It wasn’t all bad. The Unemployment Rate fell to 4.2% from 4.6%.

The Omicron variant is everywhere. Traders are no longer care if judged by global equity indexes. Asia markets closed higher, led by a 1.0% rise in Japan’s Nikkei 225 index. European bourses and Wall Street equity futures eked out gains post NFP.

The US dollar has an underlying bid due to hawkish comments from Fed officials. Atlanta Fed President Bostic said it may be “appropriate to full forward the lift-off.” San Francisco Fed Chair Mary Daly said officials might need to craft a plan for raising rates. Cleveland Fed President agrees with the others acknowledging that if inflation remains elevated, “we are in a position to be able to hike if we have to.”

US interest rates may rise, but equity traders appear to be taking direction from the bond market and not the Fed. The US 10-year Treasury yield languishes at 1.443%, down from 1.669% on November 23.

EURUSD traded quietly in a 1.1283-1.1314, rising to 1.1333 after NFP. The gains were not sustained. Prices are weighed down by mixed economic data, broad US dollar demand and dovish comments from ECB President Christine Lagarde. She told Reuters that a rate hike next year is very unlikely. Eurozone and German Services PMI data was a tick lower than forecast due to ongoing supply issues. Retail sales ticked higher, rising 0.2% m/m. EURUSD technicals are bearish below 1.1380.

GBPUSD drifted in a 1.3270-1.3300 range, tracking broad EURUSD moves. Dovish comments from BoE MPC member Michael Saunders weighed on GBPUSD. He said rate increases should be delayed until there is further data from the new Omicron variant is available.

USDJPY bounced around in a 112.97-113.48. Safe-haven demand for yen and Treasury yield weakness pressured prices while hawkish Fed comments and broad US dollar strength provided support.

AUDUSD traded lower with traders ignoring Australia composite and services PMI data. The upcoming RBA meeting on Tuesday is shaping up to be a non-event.

US Services PMI and factory orders are due today.

Chart of the Day: US dollar Index

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

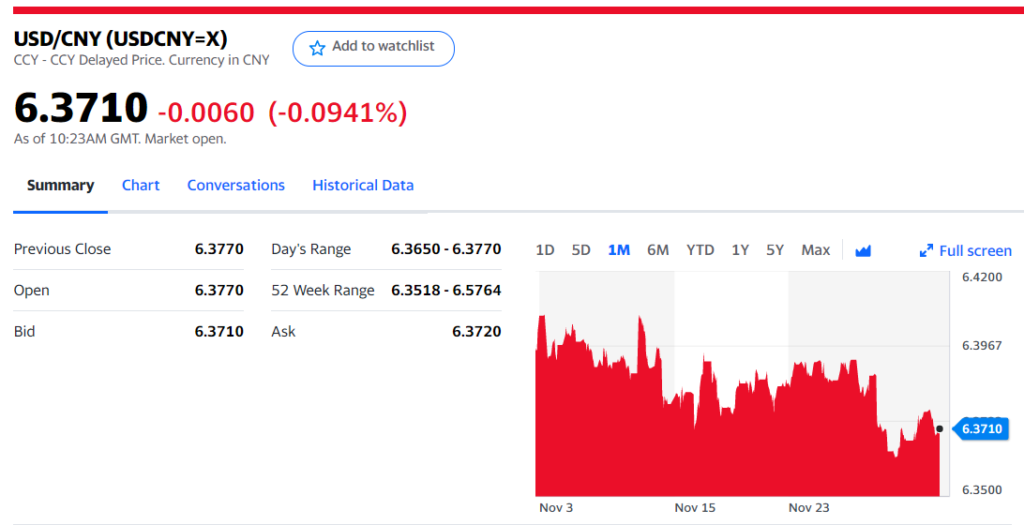

China Snapshot

Today’s Bank of China Fix 6.3738 Previous 6.3719

Shanghai Shenzhen CSI 300 rose 0.92% to 4,901.02

Caixin November Services PMI 52.1 vs October 53.8

Chart: USDCNY 1 month

Source: Yahoo Finance