Source:educatorclips.com

- BoC decision ahead; statement only, no press conference

- GBP pressured by fears of new COVID-19 restrictions in UK

- US dollar steady overnight, retreats from Tuesday’s opening levels

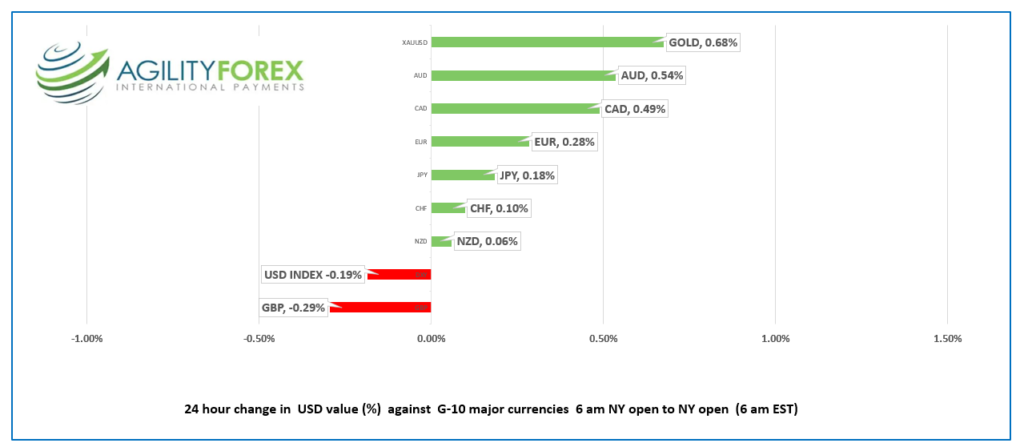

FX at a Glance

Source: IFXA Ltd/RP

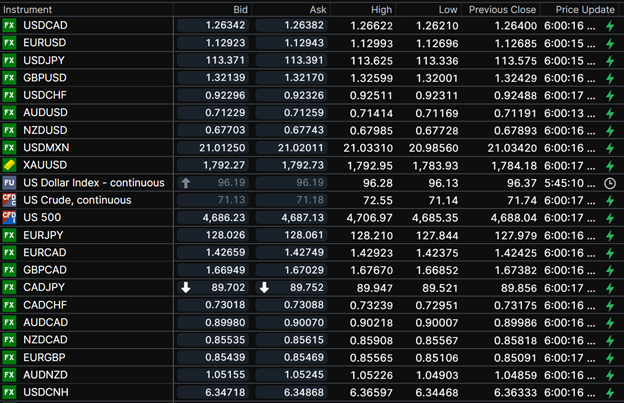

USDCAD Snapshot Open 1.2634-38, Overnight Range 1.2618-1.2662, Previous close 1.2640

USDCAD tested key support at 1.2620 overnight which held, but it is being retested in NY. The currency pair is weighed down by the rebound in WTI oil prices and downgraded concerns around the Omicron variant.

USDCAD is also seeing downward pressure from pre-BoC policy meeting positioning. The BoC may follow the RBA’s lead and downplay concerns about the latest COVID-19 variant, while providing an upbeat outlook for 2022. Analysts suggest that existing high inflation levels, and strong employment data will force the BoC to raise interest rates in March or April.

However, there is a high risk that the statement will be bland and a non-event. That’s because there is not a press conference and there are no new economic projections.

Technical view: The intraday USDCAD technicals are bearish below 1.2760. the currency pair needs to chop through resistance in the 1.2580-1.2620 area to suggest that a short-term peak occurred at 1.2850 and shift the focus to 1.2360 and 1.2220.

For today, USDCAD support is at 1.2605 and 1.2580. Resistance is at 1.2660 and 1.2690. Today’s Range 1.2580-1.2660

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

FX markets traded quietly in an uneventful session overnight content to await Friday’s UK and European data, although the main focus will be on the US inflation numbers.

Wall Street closed with impressive gains yesterday, and Asia equities followed suit. Japan’s Nikkei 225 climbed 1.42%, Australia’s ASX 200 rallied 1.25%, while Hong Long’s Hang Seng closed flat. European bourses are in the red, led by a 0.62% decline in the German Dax (Welcome to the Chancellor’s office, Mr. Scholz). The UK FTSE 100 is the outlier, rising 0.19%. WTI oil fell 0.72%, while Gold gained 0.49%. Both commodities are stuck in well-travelled ranges. The US 10-year yield was stuck in the 1.43% area overnight but popped to 1.503% in NY

President Biden and Putin’s video chat yesterday ended without disruptions for markets, although it could be disruptive for Ukraine. No decisions were announced. Biden threatened sanctions, and Putin wanted an end to NATO expansion.

EURUSD rallied yesterday and extended those gains overnight, trading in a 1.1270-1.1299 band due to modestly positive risk sentiment as fears around Omicron fade. ECB policymaker Luis de Guindos downplayed risks from the Omicron variant while forecasting that inflation will remain higher, for longer. His colleague, Ollie Rehn, repeated that “uncertainty was high for monetary policy.” There were not any economic data releases of note. The intraday technicals are bullish, looking for a break above 1.1300 to extend gains to 1.1360.

GBPUSD is trading with a negative bias as prices dropped from 1.3259 to 1.3188 in early NY trading, after reports that Prime Minister Johnson is considering new COVID-19 restrictions and a shift to Plan B. Measures in Plan B include, possible covid passports, mandatory face mask wearing, and a return to work from home.

USDJPY is trading near the bottom of its 113.32-113.63 range after the US Treasury yield rally stalled. Japan Q3 GDP fell 0.9% q/q.

AUDUSD and NZDUSD rallied due to improved risk sentiment lifting commodity prices, and broad US dollar weakness. AUDUSD continues to benefit from the latest RBA outlook which downplayed risks from the Omicron variant. Some analysts suggest that the RBA could hike rates sooner than expected.

Today’s US data includes the JOLTS jobs openings report, which is usually a non-event.

Chart of the Day: GBPUSD

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

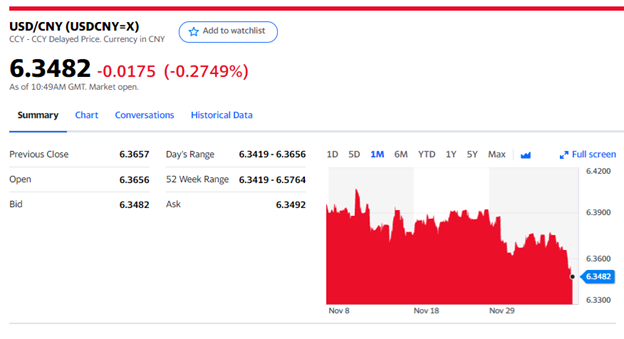

China Snapshot

Today’s Bank of China Fix 6.3677, Previous 6.3738

Shanghai Shenzhen CSI 300 rose 1.50% to 4,995.93

Chart: USDCNY 1 month

Source: Yahoo Finance