Source: myparkingsign

- Year-end flows and rising stock markets govern FX direction

- Traders remain cautious as Omicron cases spike in Canada and US

- US dollar retreats, opens at or near, session lows

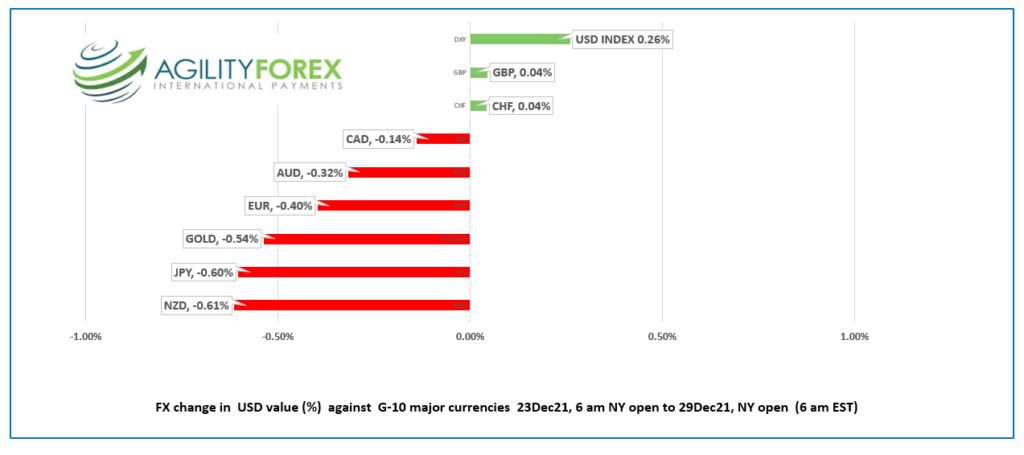

FX at a Glance

Source: IFXA Ltd/RP

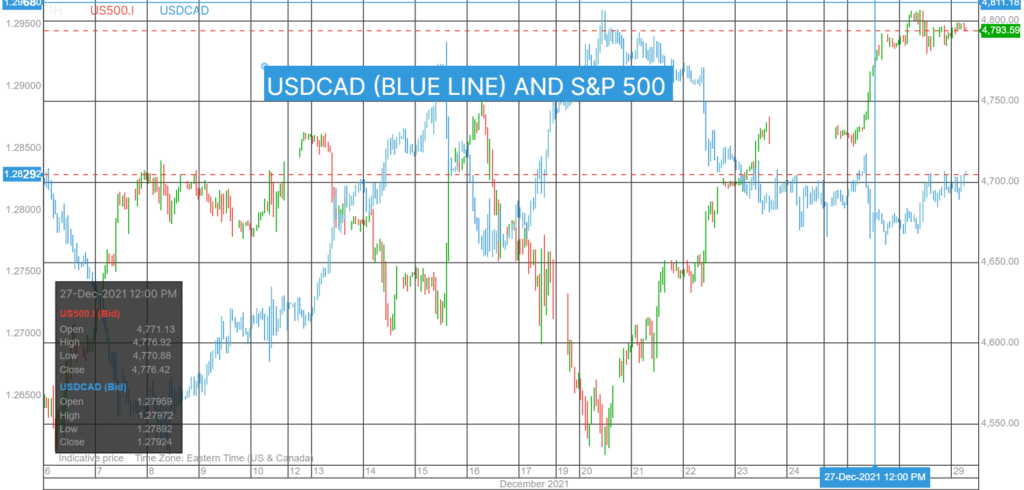

USDCAD Snapshot Open 1.2832, Dec. 23-29 Range 1.2772-1.2845, Dec. 23 close 1.2808

USDCAD chopped and churned in a relatively narrow range since Thursday’s NY close. Financial market closures in various regions from Friday to Tuesday sapped liquidity and exaggerated price moves. Many take the entire week off and don’t return until January 4.

But while you were away, the oil mice did play. Prices climbed on hopes for renewed demand as Europe and the UK failed to impose another round of restrictions and lockdowns in the face of soaring Omicron cases. Prices were underpinned by API reporting a 3.0 million drop in US crude inventories for the week ending December 24. WTI climbed from $72.30/b on Thursday to $76.86 yesterday, then consolidated in a $75.80-$76.30/b range overnight.

USDCAD gains may be limited as many forecasters are predicting USDCAD weakness in the first part of 202. That’s because they expect the first BoC rate hike in April, which is two months ahead of the Fed, and higher oil prices.

USDCAD direction is highly correlated with S&P 500 moves, and that won’t change this week.

Technical view: The intraday USDCAD technicals are bullish above 1.2770 which represents the uptrend line from October 27, looking for a break above 1.2870 to target 1.2950. A move below 1.2770 targets 1.2720 then 1.2660.

Note: The technicals are close to useless due to month-end and year-end flows in a poor liquidity environment.

For today, USDCAD support is at 1.2770 and 1.2720. Resistance is at 1.2840 and 1.2880. Today’s Range 1.2770-1.2850

Chart USDCAD and S&P 500 (hourly chart)

Source: Saxo Bank

G-10 FX recap and outlook

The Christmas break is in full swing but for some traders there is still work to be done. Month-end and year-end portfolio rebalancing flows will be evident for the rest of this week and the early part of next week.

Omicron news dominates the headlines with cases soaring worldwide. However, “studies” suggesting that Omicron is less severe than Delta, combined with pandemic fatigue, suggests traders are less concerned with this outbreak, at least those that haven’t been infected.

Rising interest rates and over-target inflation are the key themes for 2022 in a mildly risk positive environment. However, global growth is expected to a tad lower than expected as supply chain issues linger.

EURUSD closed at 1.1338 Thursday and spend the next three trading days in a 1.1268-1.1332 range. European markets were closed from Friday

GBPUSD rallied from 1.3362-1.3460 range since Thursday, with prices underpinned by expectations for another hawkish BoE outcome at the February 3 meeting.

USDJPY climbed steadily rising from a low of 114.32 on Monday to 115.02 in early NY today. USDJPY is underpinned by year end flows.

AUDUSD and NZDUSD retreated from peak levels on Tuesday as the global stock market rally paused and Omicron cases rose in Australia and New Zealand.

The US data (Pending Home Sales) will be a non-event.

Chart of the Day: USDJPY 4 hour

Source: Yahoo Finance

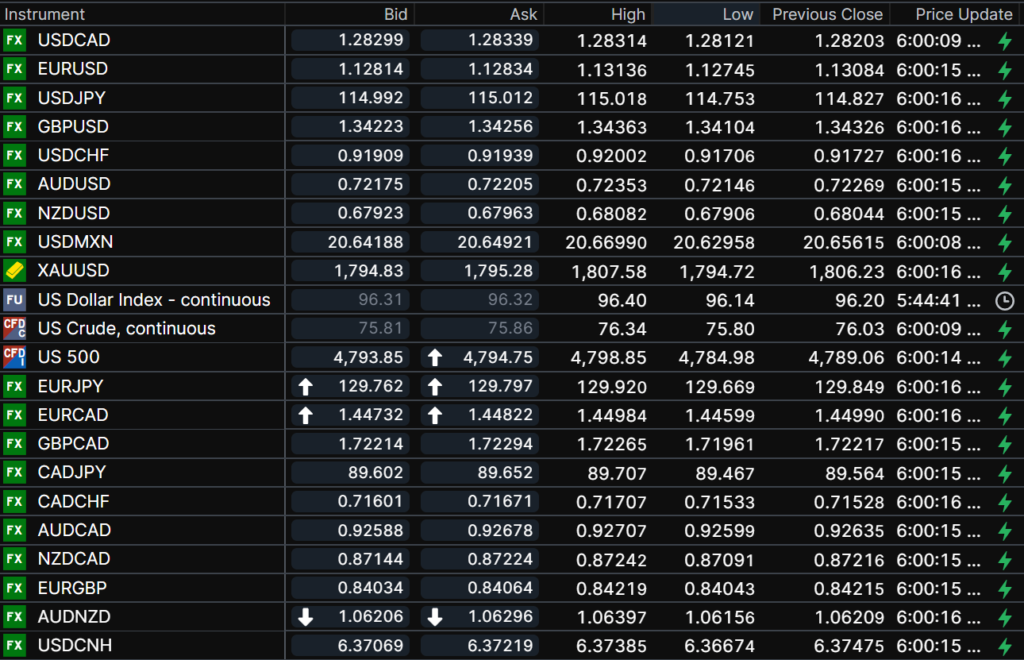

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

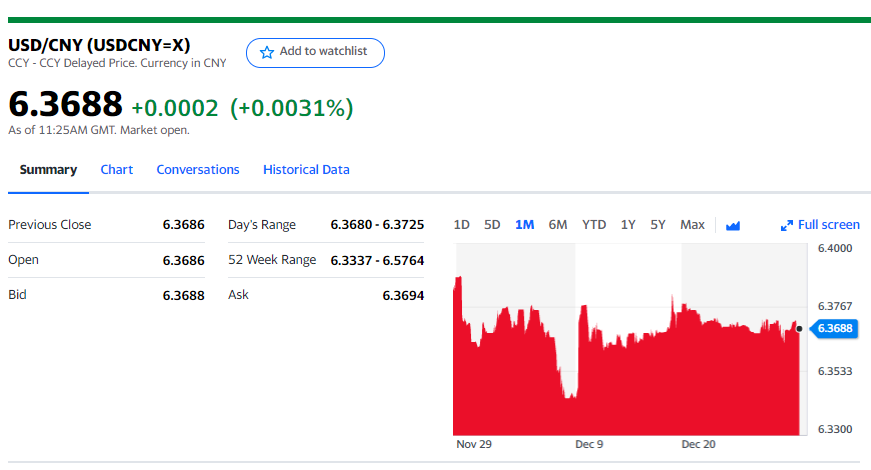

China Snapshot

Today’s Bank of China Fix 6.3735

Shanghai Shenzhen CSI 300 fell 1.46% to 4,883.48

Chart: USDCNY 1 month

Source: Yahoo Finance