- Russian peacekeepers move into Eastern Ukraine

- Economic data takes back seat to geopolitics

- US dollar opens mixed, still rangebound

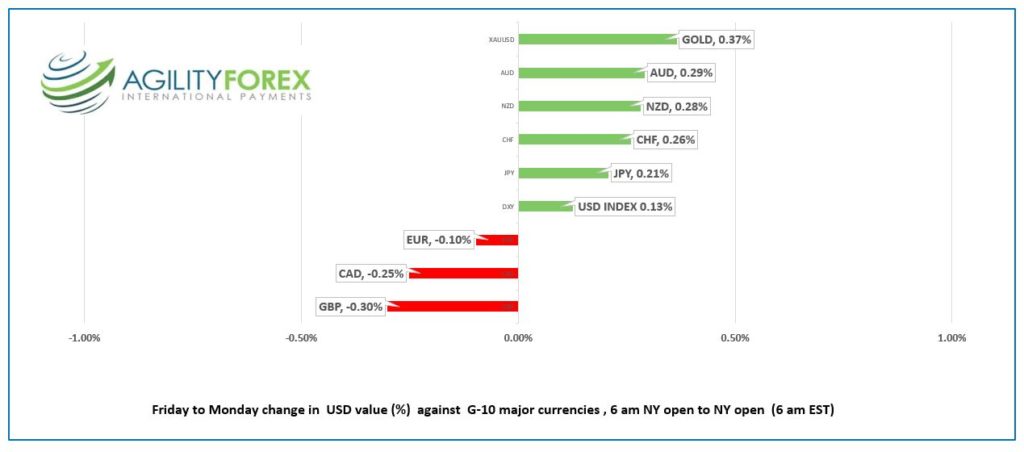

FX at a Glance Friday Feb 18-to Tuesday Feb 22

Source: IFXA Ltd/RP

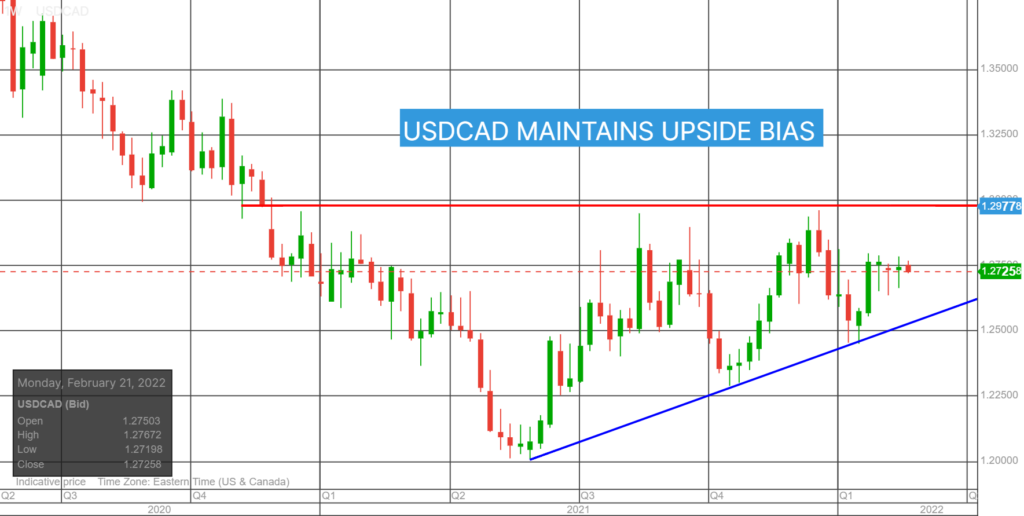

USDCAD Snapshot: Open 1.2730-34, Fri. close-Tue. open range-1.2721-1.2767, Fri. close 1.2751

USDCAD swirled in geopolitical, WTI vortex inside a relatively tight band. Rising oil prices and Canada’s distance form Ukraine helped offset risks from Russia’s peace-keeping plans in Eastern Ukraine.

WTI oil prices hit a gusher, soaring from $89.09/barrel Friday to $95.96/b in Europe today, before easing to $94.97/b in early NY trading. The gains were driven by the Russia /US and NATO tensions. The Iran nuclear talks are progressing with a deal possible before the end of the week and will remain in force until Trump becomes President again.

USDCAD direction will be dictated headlines influencing broad US dollar sentiment. The surge in WTI prices will slow USDCAD gains on escalating US and Russia tensions

There are not any Canadian economic reports today or the rest of the week.

Technical view: The intraday technicals continue to be directionless inside a 1.2670-1.2770 range. There is a mildly bearish bias following the move below 1.2740 overnight, which targets a break of 1.2720 extending losses to 1.2770. The uptrend line from June 2021 is intact above the 1.2500-1.2520 area aiming for significant resistance in the 1.2980-1.310 area.

For today, USDCAD support is at 1.2720 and 1.2670. Resistance is at 1.2770 and 1.2810. Today’s Range 1.2670-1.2770

Chart USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

It’s been a headline-driven 48 hours. Bonds, stocks commodities, and FX traders reacted to news of Russian plans for the Ukraine and even China’s latest crackdown on tech stocks was overshadowed.

The weekend was filled with rumours and reports about Russia’s plans for the Ukraine. President Biden’s warnings were explicit. He said Russia would invade Ukraine, and depending upon your perspective, that’s what happened.

Russia President Putin recognized two Ukrainian separatist regions as independent republics. Afterwards, he dispatched peacekeeping troops into the regions to keep the peace among the Russian proxy troops that were already there.

The initial “risk-off” reaction across markets has already faded. S&P 500 futures dropped to the 4,257.00 area on Monday, after closing Friday at 4,348.87. They have since rallied to 4,440.00 in NY trading today. Gold prices slumped from $1,913.19 to $1897.48 in NY.

Fed-speak is largely ignored. Governor Michelle Bowman suggested she was open to a 50 bp rate hike at the March meeting, “depending upon the data” and Chicago Fed President Charles Evan believes rates need to rise to 2.5%.

EURUSD traded erratically in a 1.1284-1.1390 since Friday and prices are sitting at 1.1340 in early trading. The single currency is underpinned by robust Eurozone and German economic data showing the Eurozone economy is rapidly recovering. Monday’s PMI reports were mixed with Manufacturing data a tad below forecasts while Services and composite data beat the estimates.

The German Ifo Survey Business Climate Index rose to 98.9 from 96.0 in January, despite the Ukraine crisis.

EURUSD gains may be limited due to its proximity to the Ukraine and depending if Russia curtails energy exports in response to EU sanctions.

Chart: EURUSD 4 hour, 3 months

Source: Saxo Bank

GBPUSD rallied from 1.3587 to 1.3637 Monday after better than expected UK PMI data, then retreated steadily to 1.3547 in NY today. Bank of England Deputy Governor Dave Ramsden’s comments suggesting “further modest tightening in monetary policy is likely to be appropriate in the coming months” may be weighing on prices as it implies a slower pace of rate hikes. However, the EU, US response to Russia’s actions will determine GBPUSD direction today.

Chart: GBPUSD 4 hour, three month

Source: Saxo Bank

USDJPY dropped to 114.51 overnight due to safe-haven demand for yen and sliding 10-year US Treasury yield which touched 1.854% yesterday, before climbing to 1.94% in NY today, tracking gains in S&P 500 futures.

AUDUSD and NZ+DUSD are underpinned in part because both countries are far from the Ukraine. In addition, NZDUSD is supported ahead of tomorrow’s RBNZ meeting where a 0.25% rate hike is expected (and priced in).

US Consumer Confidence and S&P Case Shiller Housing Price data will be overshadowed by Russia headlines.

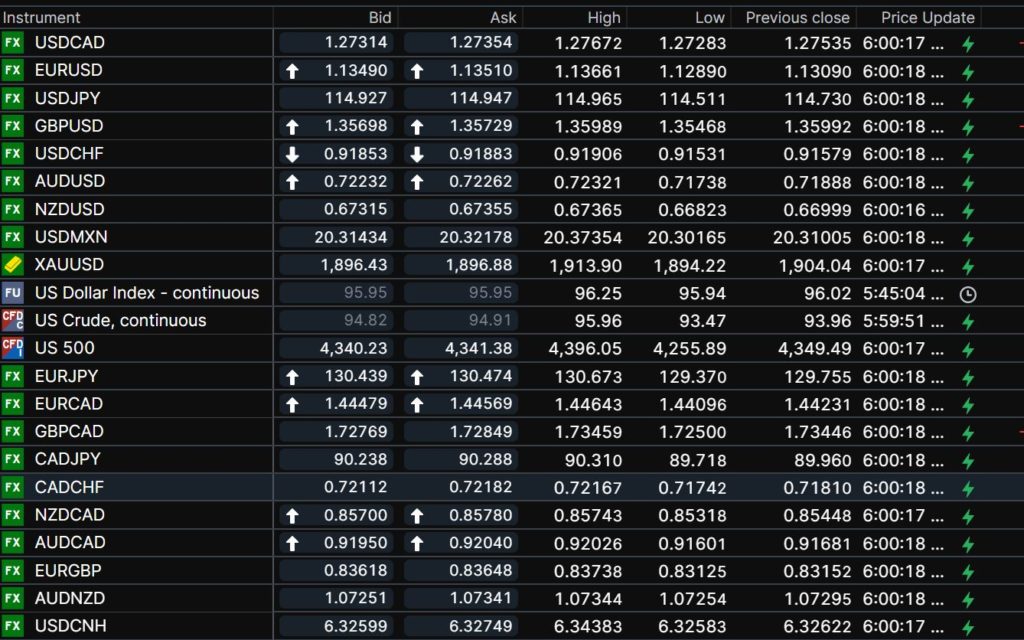

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

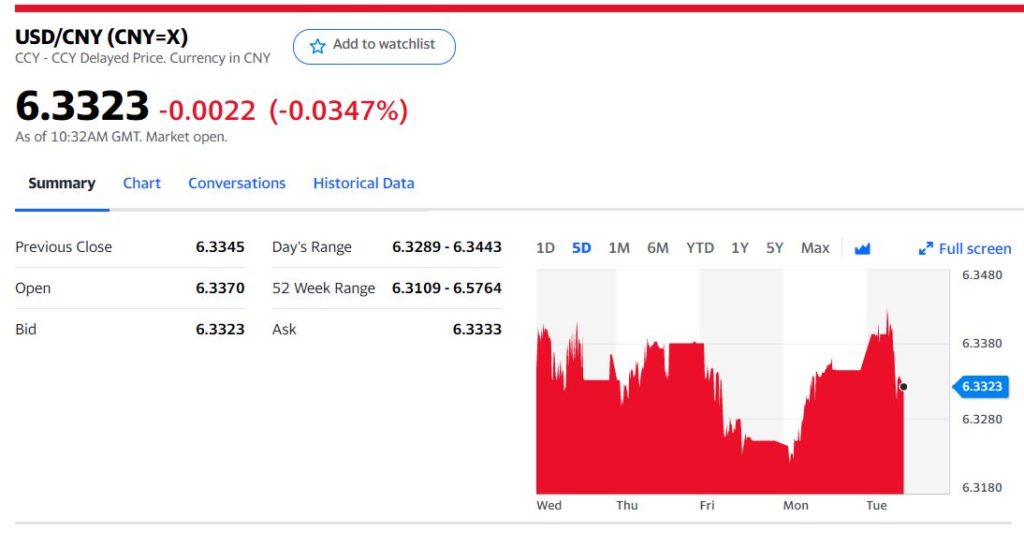

China Snapshot

Today’s Bank of China Fix 6.3487, Monday 6.3401, Friday 6.3343

Shanghai Shenzhen CSI 300 fell 1.66% to 4,574.15, from Friday close of 4651.24

China stocks roiled by negative sentiment from Russia and Ukraine, along with further Tech Stock crackdown fears. Chinese regulators reportedly told banks to report their exposures to Ant and Tencent.

Chart: China 5 day

Source: Saxo Bank