Source: Pixabay

- Chinese retreats further from Covid-zero

- Bank of Canada guess: 50/50 split between 25 and 50 bp bump

- US dollar consolidating gains in nervous market

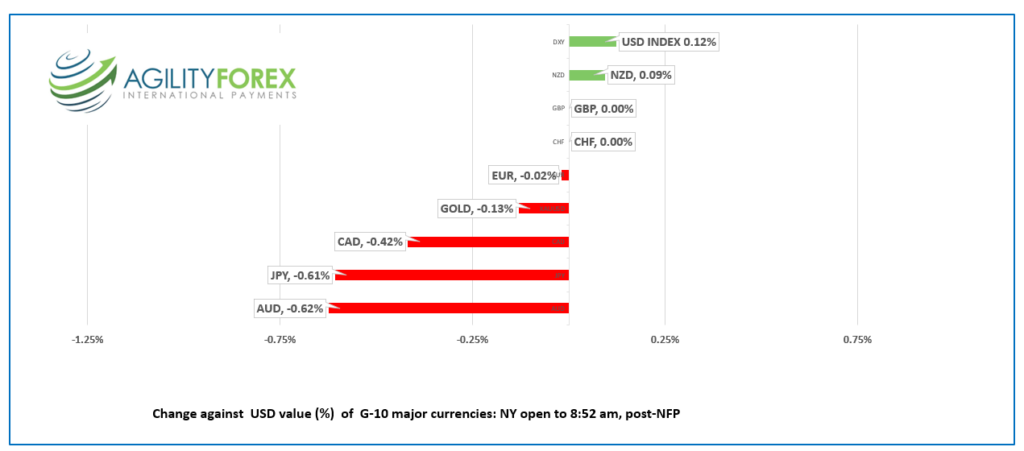

FX at a glance:

Source: IFXA Ltd/RP

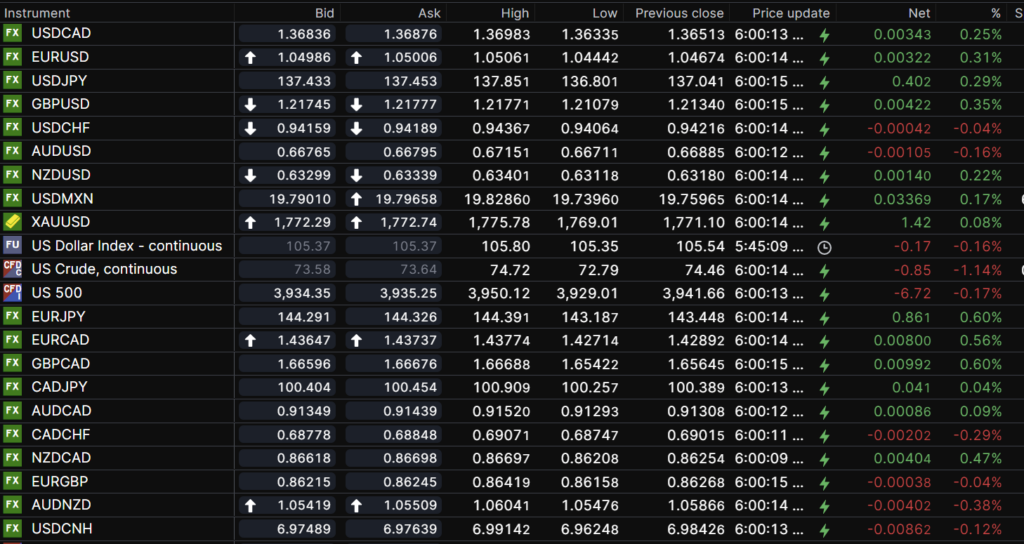

USDCAD Snapshot: open 1.3684-88, overnight range 1.3634-1.3698, close 1.3651

USDCAD added to yesterday’s gains overnight on the back of softer commodity prices, particularly crude.

The drop in commodity prices is due to escalating recession fears stoked by comments from the CEOs at JP Morgan and Goldman Sachs. JPM’s Dimon warned that rising interest rates and inflation will wipe out the cash cushion consumers built up during pandemic which could cause a recession. Goldman’s Solomon thinks US recession risks are about 2 out of 3.

Those comments and thin pre-FOMC markets helped drive stock and commodity prices lower.

WTI dropped to $72.79/barrel in early NY trading before inching back to $73.55/b. Prices have dropped 11.8% (peak to trough) since Monday as US and European recession fears overshadow news that China accelerated its retreat from pandemic restrictions.

The Bank of Canada gets its moment in the spotlight. USDCAD may see a bit of volatility because markets are undecided between a 25 or 50 bps hike.

The BoC’s policy rate sits at 3.75% which is 25 bp below the US fed funds rate of 4.0%. The FOMC is expected to hike rates by 50 bps next week, although some analysts fear they could go 75 bps.

So, if the BoC only raises rates by 25 bps, while WTI prices remain depressed, USDCAD will target the 2022 peak of 1.3965.

USDCAD would retreat toward 1.3500 following a 50 bp bump, unless the BoC statement suggests that the rate hike cycle is close to ending. That will leave USDCAD rangebound, with a bullish bias.

We will know by 10: am ET.

USDCAD Technical outlook

The intraday USDCAD are bullish while trading above 1.3630, looking for a break above 1.3710 to extend gains to 1.3810. A topside break targets 1.4000. A move below 1.3630 suggests a retest of the 1.3550 area.

The November USDCAD uptrend is intact while prices are above 1.3410.

For today, USDCAD support is at 1.3630 and 1.3570. Resistance is at 1.3710 and 1.3760

Today’s range 1.3650-1.3750

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Chinese authorities announced further easing of its draconian Covid-zero policies overnight but reaction to the news was underwhelming. Markets have been anticipating such an outcome since large-scale anti-covid protests swept across China.

Traders have turned their attention to wobbly stock markets and numerous analyst predictions for a recession in 2023, in the absence of top-tier US data and “radio-silence from Fed officials.

Asia equity indexes followed Wall Street’s lead and sold off, but news China was further easing covid restrictions tempered the slide. Australia’s ASX 200 fell 0.85% while Japan’s Nikkei fell 0.72%. European bourses are also on the defensive with the German Dax down 0.34%. S&P 500 futures are down 0.42%

The US 10-year Treasury yield is a tad higher at 3.546%.

EURUSD crawled higher, rising from 1.0444 to 1.0506 in early NY supported by better-than-expected Eurozone data. Q3 GDP rose 2.3%, y/y, and 0.3% q/q compared to forecast for a 2.1% y/y gain and a 0.2% q/q increase. Eurozone employment rose 1.8% y/y (forecast 1.7%). EURUSD technicals are bearish after the failure to extend gains above 1.0500 suggests a retreat toward 1.0200.

GBPUSD rallied from 1.2107 in Asia to 1.2185 in early NY, then dropped to 1.2155. UK House price data was weak but not a surprise. Traders are biding their time until next week’s FOMC meeting. The intraday GBPUSD technicals are bearish below 1.2205.

USDJPY inched higher overnight, rising from 136.80 to 13765 in NY. Prices are underpinned by broad US dollar demand due to increased fears of a US recession. USDJPY continues to have limited downside due to dovish BoJ monetary policy.

AUDUSD traded negatively in a 0.6670-0.6715 range, weighed down by weaker commodity prices and soft Chinese trade data. Robust Q3 GDP (actual 5.9% vs previous 3.6% y/y) news was overshadowed by US recession fears.

There are no US top tier economic reports today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

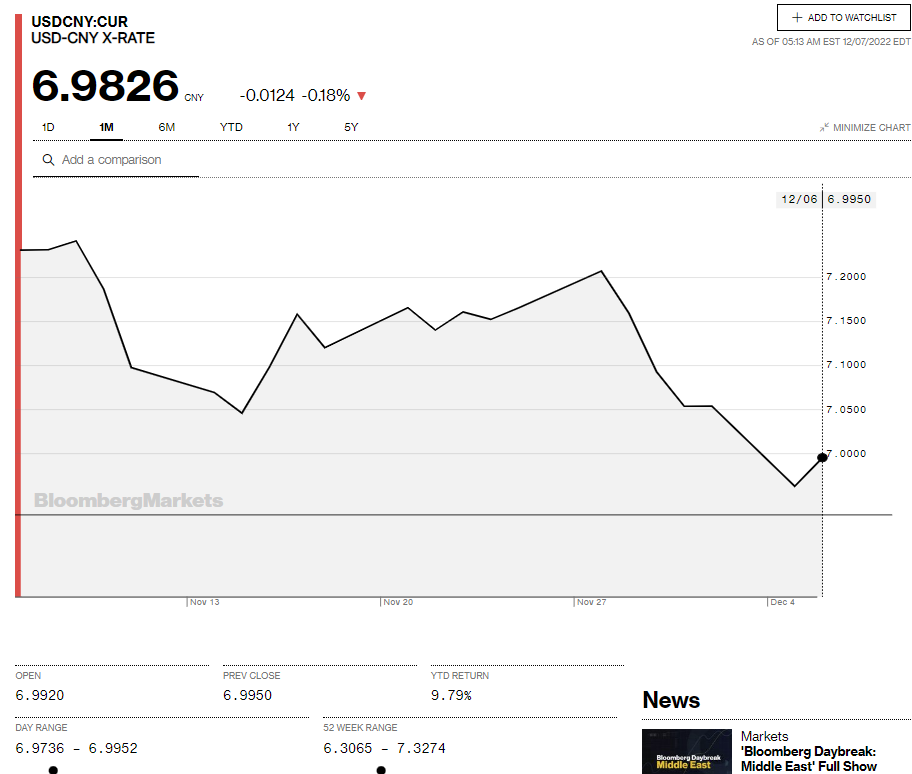

China Snapshot

Today’s Bank of China Fix: 6.9975, previous 6.9746

Shanghai Shenzhen CSI 300 fell 0.25% to 3958.44

November Trade surplus $69.84 billion (forecast $78.1 b, Oct. $81.15b)

November exports -8.7% y/y (Oct. -0.3% y/y)

November Imports -10.6% y/y (Oct. -0.7%y/y)

Shrinking trade surplus blamed on supply disruptions in China and weak demand from Europe and the US.

China is stepping up its exit from Covid-zero. The State Council plans to scrap requirements for virus testing and QR code scanning when entering premises, ease internal travel testing rules and ban limit the ability of local authorities to shut down entire city blocks.

Chart: USDCNY 1 month

Source: Bloomberg