Photo: Road and Track

- Trader’s fear getting burned by hotter than expected US CPI data

- WTI oil prices slide further, WTI flirting with $70.00/b again

- US dollar opens mixed compared to Friday- CAD underperforms

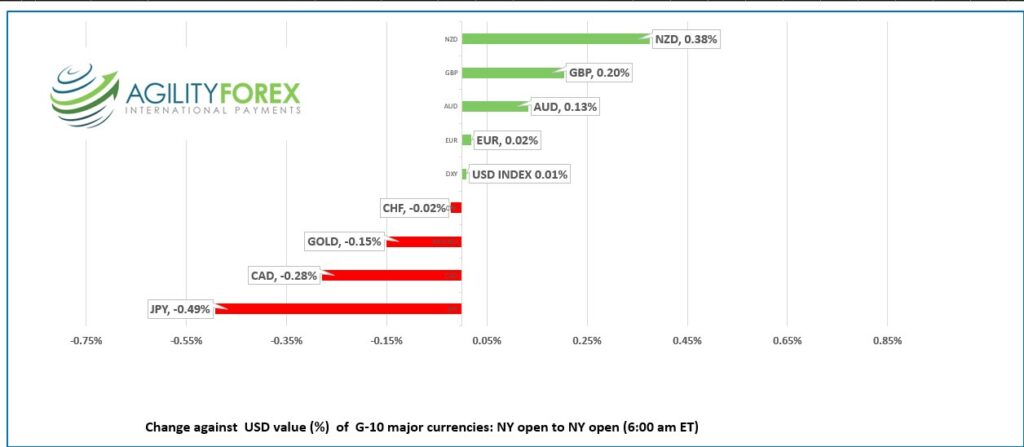

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3659-63, overnight range 1.3634-1.3673, close 1.3646

USDCAD had its moment in the sun last week after the Bank of Canada monetary policy meeting. The 50-bp rate hike took the overnight rate to 4.25% and the statement dropped the inference that more rate hikes would be needed.

BoC Governor will explain the decision in further detail today in Vancouver at 9:25 PT (12:25 pm ET). His remarks are unlikely to differ from Deputy Governor Kozicki’s comments last Thursday.

USDCAD traders have shifted their attention from domestic data and central bank policy to south of the border. Tuesday’s US inflation report and Wednesday’s FOMC meeting are key.

USDCAD is suffering from a bout of oil price blues. WTI dropped from $72.73/b to $70.18 on Friday then rallied to close at $71.55/b. Prices rose further in Asia overnight reaching $72.29/b before dropping to $70.29/b in Europe. Traders are concerned about weakening global which makes little sense as winter is just beginning.

There are no Canadian economic reports today.

USDCAD technical outlook.

The USDCAD intraday technicals are bullish in an uptrend channel between 1.3620 and 1.3700. A move below 1.3620 will extend losses to 1.3580, then 1.3540. A break above 1.3700 targets 1.3750 then 1.3810.

Longer term, the uptrend line from August is intact while prices are above 1.3350.

For today, USDCAD support is at 1.3630 and 1.3590. Resistance is at 1.3690 and 1.3730

Today’s range 1.3610-1.3690

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global markets started the week under a yellow flag. All eyes are on Tuesday’s US CPI report where Core CPI is expected to dip to 6.1% from 6.3% in October. Friday’s hotter-than-expected US PPI ex-food and energy data (actual 0.4% m/m forecast 0.3%) raised concerns for a similar outcome for CPI.

US Treasury Secretary Janet Yellen was on CBS 60 minutes Sunday and told viewers “I believe inflation will be lower,” while expressing her hope for a healthy labour market. Her words a little to zero impact as she no longer an unbiased observer but a shill for the Biden administration.

Asian equity markets closed with losses. Australia’s ASX 200 fell 0.45% while “fear of the Fed” knocked Hong Kong’s Hang Seng index down 2.20%. European bourses are quiet but and trading close to flat. S&P 500 futures have gained 0.39%

EURUSD ticked higher, rising from 1.0507 to 1.0572 in early NY partly because positions closed on Friday were reopened today. Price action will likely be choppy ahead of CPI, and the upcoming FOMC and ECB meetings.

GBPUSD got an infusion of better-than-expected data which drove prices from 1.2208 to 1.2295. October GDP surprised analysts by rising 0.5% m/m rather than falling 0.1%. Manufacturing Production rose 0.7% m/m (forecast -0.1%) was flat. It was a good news-bad news data day. Aug-Oct quarterly GDP fell 0.3% prompting the Chancellor of the Exchequer Jeremy Hunt to warn of a “tough road ahead.” The BoE is expected to hike rates 0.50% on Thursday.

USDJPY inched higher in a 136.57-137.12 range supported by the US 10-year yield rising from 3.452% Friday to 3.521% in NY. Japanese PPI rose 0.5% m/m in November (forecast 0.5%).

AUDUSD traded in a 0.6759-0.6799 range while NZDUSD traded in a 0.6381-0.6420 band. NZDUSD is outperforming against its Aussie cousin as the RBNZ’s interest rate outlook is more hawkish than the RBA’s.

The US data calendar is empty.

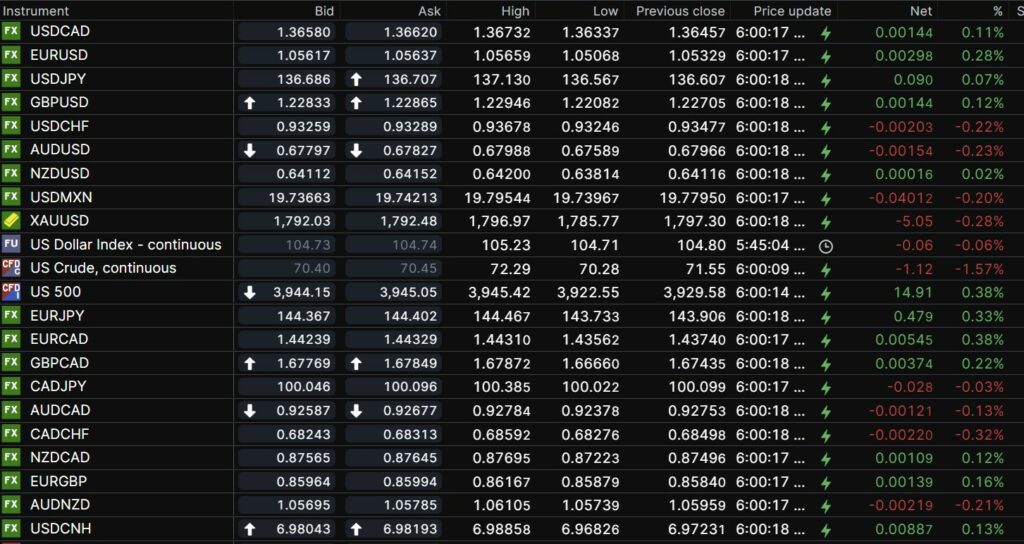

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

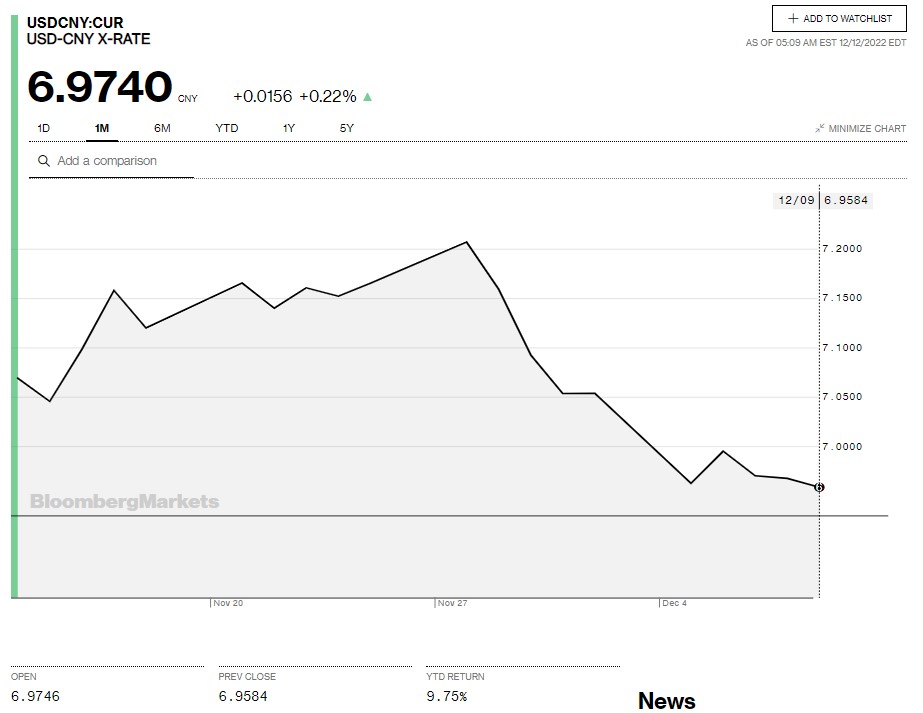

China Snapshot

Today’s Bank of China Fix: 6.9565, previous 6.9588

Shanghai Shenzhen CSI 300 fell 1.12%% to 3953.44

Chart: USDCNY 1 month

Source: Bloomberg