Photo: Wikipedia

- BoJ tweaks YCC, JPY soars, stocks plunge

- Higher Treasury yields underpin US dollar

- US dollar opens mixed after volatile overnight session

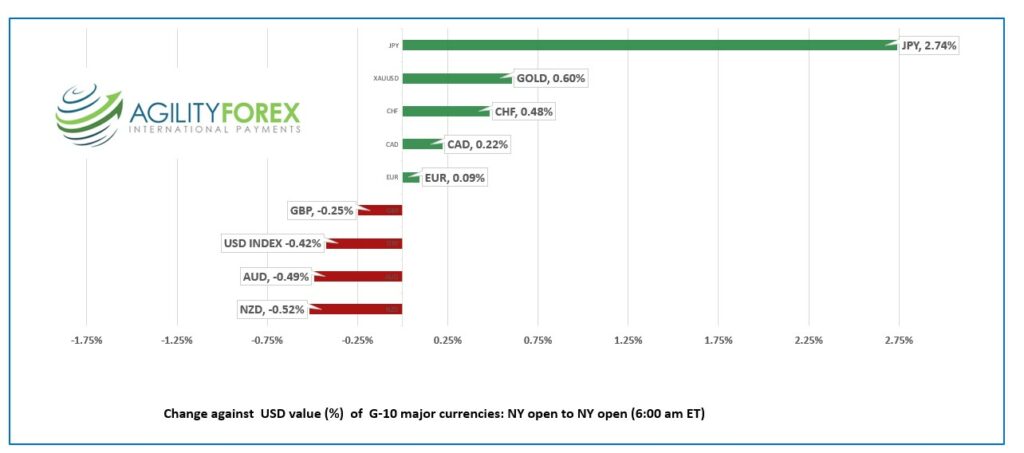

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3616-20, overnight range 1.3612-1.3702, close 1.3651

USDCAD had a wild ride overnight, courtesy of the Bank of Japan but the currency pair still managed to open in NY with a loss.

The USDCAD volatility was due to the BoJ modestly tightening policy which fueled a torrent of cross-yen activity including CADJPY sales.

USDCAD was also undermined by rising WTI oil prices which climbed from an overnight low of $74.52/barrel to $76.26/b, before dropping to open nearly unchanged today. Traders are torn between buying crude ahead of an expected rebound in demand in 2023 or selling crude because of US recession risks and the latest surge in Covid cases in China.

Statistics Canada reported Retail Sales rose 1.4% in October, a tick lower than the 1.5% expected which was still the largest increase in five months.

USDCAD technical outlook.

The intraday technicals are bullish above 1.3580 which guards the November uptrend line at 1.3540. If prices stay above 1.3540, a retest of 1.3700 is likely. A break below 1.3540 would target 1.3400.

Longer term, the USDCAD technicals are bullish above the uptrend line from November 16, at 1.3520, looking for a break above 1.3700 to extend gains to 1.3850 then 1.4000 on a daily chart. A break below 1.3520 targets 1.3400.

For today, USDCAD support is at 1.3580 and 1.3540. Resistance is at 1.3660 and 1.3710

Today’s range 1.3570-1.3660

Chart: USDCAD weekly since January 2022

Source: Saxo Bank

G-10 FX recap and outlook

Japan is famous for its sneak attack on Pearl Harbour which occurred in December, 81 years ago which President Franklin D Roosevelt caid would be “a day that would live on in infamy.”

The Bank of Japan made a similar move overnight, except without the bombs.

The BoJ surprised markets when they raised the band on the yield curve control policy from +/- 0.25% to +/-0.50%. The move was especially galling because for months and months BoJ officials insisted there was no need to change monetary policy because the Japanese economy was different.

The move roiled global bond, equity and FX markets which were already suffering from poor liquidity due to seasonal holidays and year end.

The US 10-year Treasury yield spiked to 3.71% from 3.583% before inching down to 3.668% in early NY.

Asian stock markets suffered a double whammy. The weak handover from Wall Street and the BoJ action combined to pummel the major stock indexes. Japan’s Nikkei 225 index fell 2.46% while Australia’s ASX 200 lost 1.54%.

European bourses dropped on the back of the BoJ actions but are well on their way to recouping the losses. The German Dax is down 0.32% compared to 1.08% at its lowest level overnight. S&P 500 futures dropped steeply in Asia but have clawed back most of the losses in early NY trading.

Gold is a big winner. XAUUSD rose $19.00 to $1806.84, while WTI oil is opening close to unchanged from its NY close.

EURUSD traded erratically in a 1.0580-1.0652 range in the wake of the BoJ news. Price action was exacerbated by sales of EURJPY which dropped from 145.82 to 140.17. German producer prices fell 3.9% in November (forecast -2.6% m/m). The EURUSD technicals are bullish above 1.0480 and looking for another test of resistance in the 1.0700 area.

GBPUSD soared and sank in a 1.2087-1.2223 band following the BoJ and are sitting above the mid—point of that range in NY. GBPUSD remains defensive as traders believe the Bank of England is more dovish than the ECB and the Fed. The intraday technicals are bearish below 1.2250.

USDJPY was crushed, plunging from 137.47 to 132.00. The BoJ actions opened the door to a flood of speculation that Japan is about to end its years of ultra-easy monetary policy even though they left the overnight rate unchanged at 0.1%. Speculation of the size and timing of the expected BoJ tightening will dominate the narrative in early 2023 and impact FX markets due to the use of yen as a funding currency.

AUDUSD rallied to 0.6743 then dropped to 0.6631 with AUDJPY selling exacerbating the price action. The release of the minutes from the RBA meeting on December 6 were not a factor. The RBA considered pausing rate hikes but hiked them 25 bps instead.

US Housing Starts were 1.427 million (forecast 1.415 million, Oct. 1.434 million).

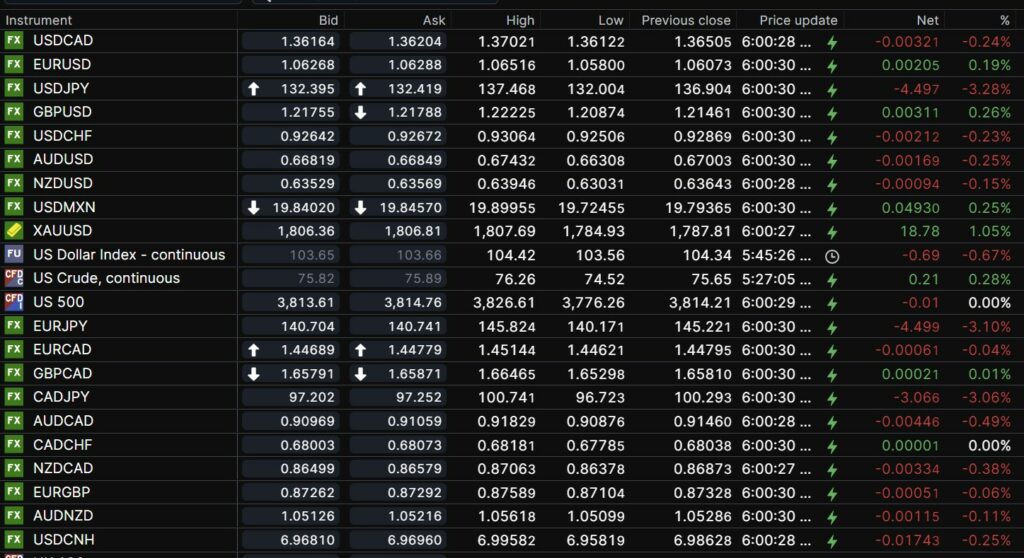

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

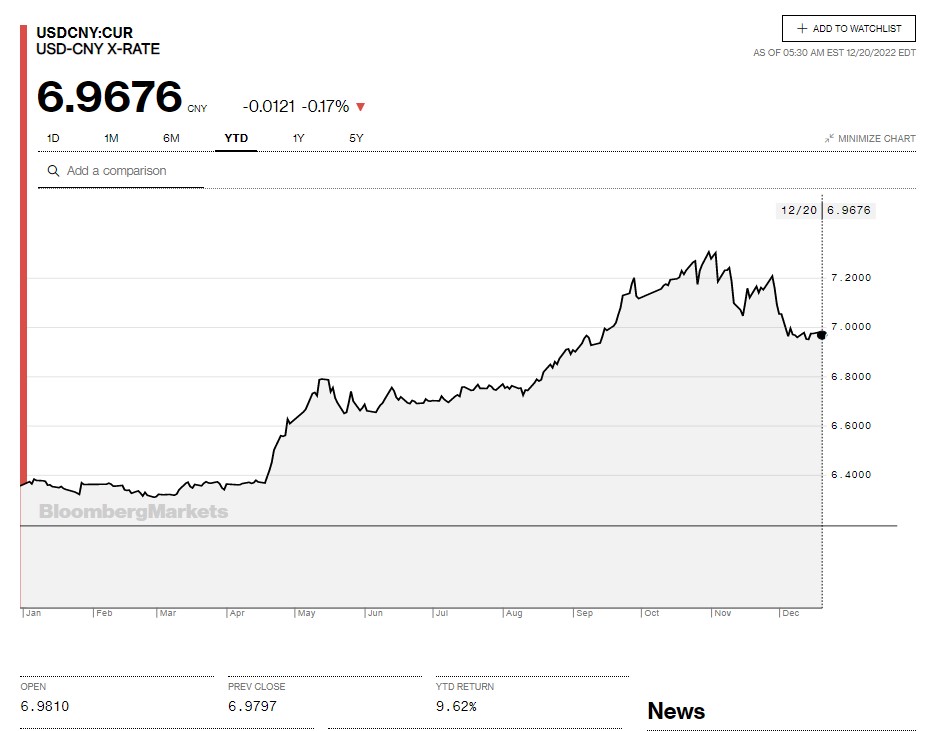

China Snapshot

Today’s Bank of China Fix: 6.9861, previous 6.9746

Shanghai Shenzhen CSI 300 fell 1.65% to 3829.02

The PboC left the 1- and 5-year Loan Prime Rate (LPR) unchanged at 3.65% and 4.30% respectively.

Markets spooked by rising Covid deaths in the face of authorities easing covid containment measures further.

Chart: USDCNY year-to-date

Source: Bloomberg