Photo: hdclipart.com

April 13, 2023

- Bank of Canada stays the course, as expected.

- FOMC minutes suggest one more hike.

- US dollar trading defensively and adds to losses overnight.

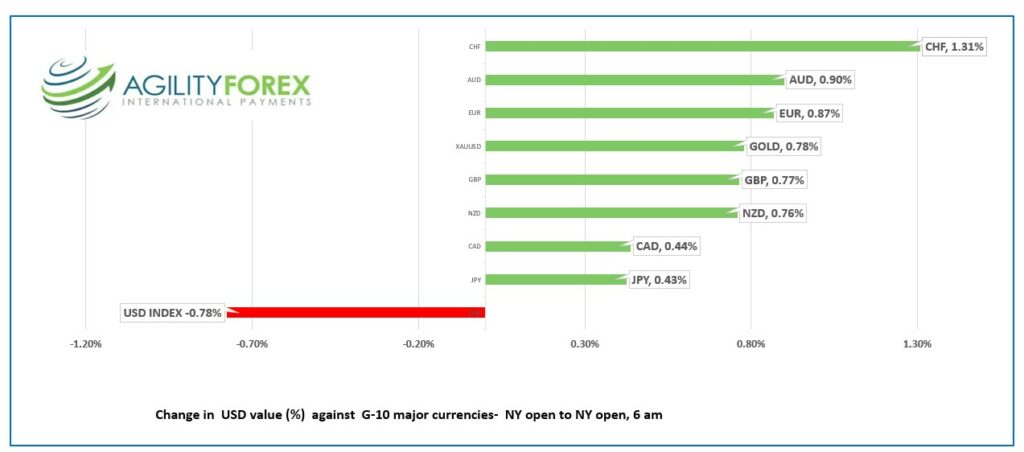

FX at a glance

Source: IFXA Ltd/RP

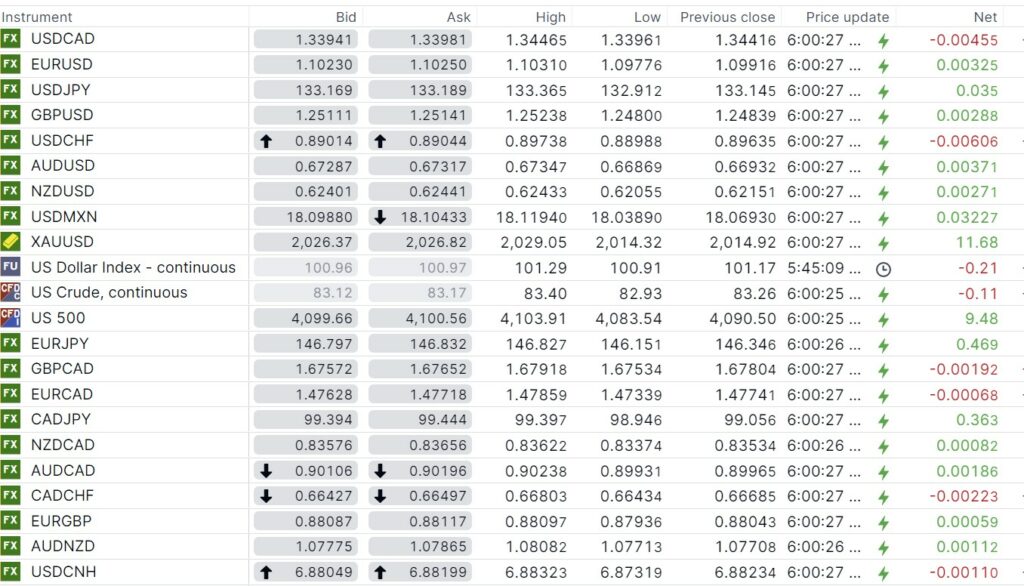

USDCAD Snapshot: open 1.3394-98, overnight range 1.3389-1.3447, close 1.3442

The Bank of Canada did not surprise anyone. They left interest rates and monetary policy unchanged but hedged themselves by warning rates could rise if the economy gets over-heated. The news had little to no impact on USDCAD trading.

It was the US inflation data that knocked USDCAD lower. Traders are now pricing that the first Fed rate cut will occur in July and the greenback was sold across the board.

WTI oil prices rallied from $81.31 yesterday to $83.40/b overnight and are looking to extend gains to $85.00. Oil traders expect lower US interest rates, increased Chinese demand, and the latest Opec production cuts to help boost prices toward $100.00/b.

USDCAD Technical Outlook

The intraday technicals are bearish below 1.3450, supported by the move through 1.3400-05 support area. A decisive break below the 200-day moving average at 1.3396 would extend losses to 1.3230.

The daily chart suggests USDCAD is becoming oversold as the RSI and Bollinger Band indicators are close to extreme levels.

For today, USDCAD support is at 1.3350 and 1.3320. Resistance is at 1.3420 and 1.3450.

Today’s range 1.3340-1.3420.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

US weekly jobless claims rose 11,000 to 239,000, which was 2,000 more than forecast. The Producer Price Index fell 0.5% m/m in March and dropped to 2.7% y/y from February’s 4.9% reading. The results lifted S&P futures and led to some slippage in the US dollar on hopes that the Fed has only one more rate hike in the tank.

Wednesday’s US March inflation report was far from conclusive. The headline number was lower than expected (actual 5.0% y/y vs forecast 5.2%, and February 6.0%) but the more important Core-CPI at 5.6%, met expectations but was higher than the 5.5% y/y seen in February. Traders focused on the lower headline number and concluded that ongoing banking and credit concerns will ensure lower rates ahead.

The FOMC minutes indicated another 25 bp rate hike was in the cards before the Fed pauses, then starts to cut rates in July.

Asian equity markets closed with Japan’s Nikkei 225 index rising 0.26% and Australia’s ASX 200 falling 0.27%. European bourses opened mixed and are trading around flat except for the French CAC 40 index which is up 0.84%. S&P 500 futures are slightly higher while oil and gold prices are down modestly. The US 110-year Treasury yield is steady at 3.435%.

EURUSD is trying to get comfortable above 1.1000, after rising from 1.0978 to 1.1031 overnight. EURUSD is underpinned by hawkish comments from Bank of France Governor and ECB policymaker Francois Villeroy yesterday. He warned of the risk that Eurozone inflation becomes entrenched above 2.0%, claiming inflation has become “more widespread and persistent.” EURUSD will test 1.1200 if prices can stay above 1.0970.

GBPUSD is at the top of its 1.2480-1.2524 range due to broad US dollar weakness on an improving inflation outlook. Traders ignored the report from the Office for National Statistics (ONS) that economic growth stagnated (February GDP 0% m/m) due to the impact of public sector strikes.

USDJPY traded in a 133.91-133.36 band. BoJ Governor Kazuo Ueda continued with his predecessor’s dovish theme, saying that monetary easing will continue until the price target is stable. Officials accidently sent an evacuation order to the island of Hokkaido due to an errant North Korean ICBM missile.

AUDUSD rallied from 0.6686 to 0.6734following a robust March employment report. Australia added 53,000 new jobs in March, on top of the 63,600 gain in February. The unemployment rate remained unchanged at 3.5%. The results support another RBA 25 bp rate hike.

NZDUSD rose from 0.6206 to 0.6244 on the back of broad US dollar weakness following the US CPI data.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

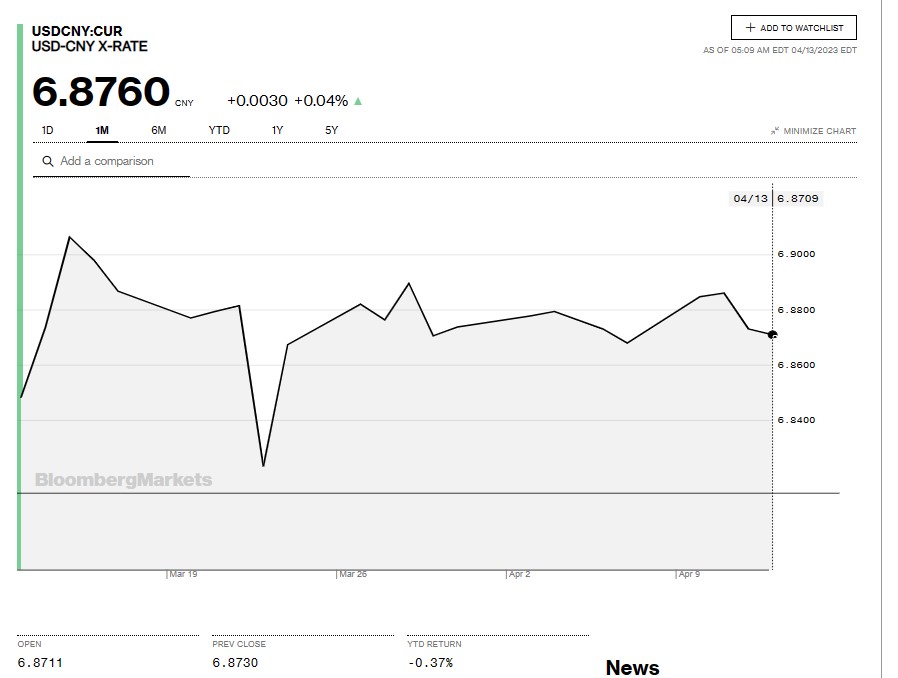

China Snapshot

Bank of China Fix: 6.8658, Previous: 6.8854.

Shanghai Shenzhen CSI 300 fell 0.69% to 4068.98.

March Trade Balance $88.19 b (February $116.8 b)

Exports 14.8% y/y (Feb -6.8%

Imports -1.4% y/y (Feb -10.2%)

Barclay’s economists suggest the sharp rise in exports combined with other strong economic reports reduces the odds that the PboC cuts rates in the near future.

Chart: USDCNY 1 month

Source: Bloomberg