April 10, 2024

- US CPI jumps to 3.5% y/y (February 3.2%)

- BoC rate decision and MPR due today

- US dollar opens little changed then soars post-CPI.

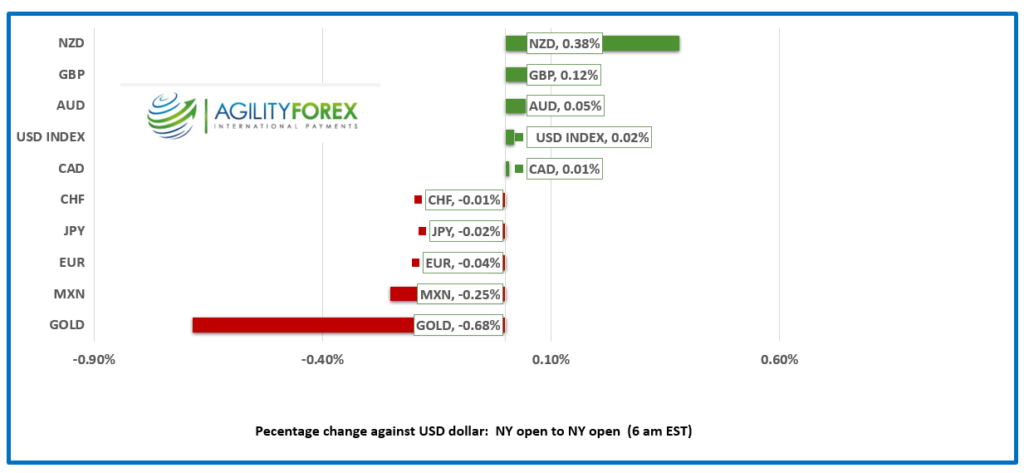

FX at a Glance-Open

FX at A glance-Open to Post CPI 5:40 am PDT

Source: IFXA/RP

USDCAD Snapshot: open 1.3567, overnight range 1.3558-1.3652, close 1.3574

USDCAD drifted aimlessly again overnight then spiked from a pre-CPI low of 1.3565 to 1.3645 in the aftermath of the hotter than expected inflation result.

The US data eliminates any chance of the Bank of Canada cutting interest rates at today’s meeting despite domestic inflation falling into the BoC’s targeted range, slow economic growth, and rising unemployment. The US inflation print also dashes hopes that the Fed would cut rates in June.

Furthermore, the BoC would be loath to provide monetary stimulus to an economy which is being pumped full of fiscal stimulus, thanks to a series of multi-billion dollar spending announcements ahead of next weeks Canadian budget.

WTI oil prices drifted lower, falling from 85.72 to 85.14 due to rising US crude inventories and suggestions that Middle East tensions are easing.

USDCAD Technicals

The intraday USDCAD technicals are bullish with the break above 1.3580 setting the stage for a move above the 1.3650-60 area to extend gains to 1.3750

Fibonacci retracement analysis on a daily chart shows that today’s break above the 61.8% level sets the stage for a rally to 1.3750, the 78.6% retracement level of the November-December range.

For today, USDCAD support is at 1.3590 and 1.3560. Resistance is at 1.3660 and 1.3690. Today’s range is 1.35.90-1.3680.

Chart: USDCAD daily

Source: DailyFX

Bumpy ride hits crater

Mr. Powell said warned about a bumpy inflation ride. He said, “We were saying that it’s going to be a bumpy ride. Now, here are some bumps, and the question is, are they more than bumps? And we just can’t know that.” Well, today you can.

US CPI was a hotter than hotter than hot 3.5% y/y while the core number ticked up to 0.4% m/m compared to expectations for a 0.3% rise. The news was not greeted warmly. The US dollar soared across the board. The US 10-year Treasury yield spiked to 4.507% from 4.342%, and S&P 500 futures plunged 1.24%.

Minutes and Fed-Speak

Fed Governor (and voter) Michelle Bowman speaks just before the minutes from the March 20 minute are released. Her remarks, the minutes, and today’s CPI report will frame the interest rate debate.

EURUSD: EURUSD was quiet in a 1.0848-1.0865 range overnight, but prices dropped to 1.0773 after the US CPI data. The risk that the ECB starts cutting rates far sooner than the Fed is driving prices lower.

GBPUSD: GBPUSD’s dropped from 1.2708 to a post-CPI low of 1.2595 due to fears that UK and US interest rate differentials will widen in favour of the US.

USDJPY: USDJPY soared to 152.51 following the US data. Recent dovish comments by BoJ Governor Kazuo Ueda and the prospect of US interest rates remaining elevated for most of 2024 is fueling USDJPY gains. The threat of BoJ intervention is not much of a deterrent.

AUDUSD and NZDUSD: AUDUSD dropped to 0.6545 from an overnight peak of 0.6632 due to broad-based US dollar strength,

NZDUSD rallied from 0.6037 to 0.6079, overnight than erased the entire move, falling to 0.6013 after the US inflation data. The RBNZ left the Overnight Cash Rate (OCR) unchanged at 5.5% and stuck with a neutral bias although for many, that was seen as being somewhat hawkish. ASB analysts do not expect the RBNZ to cut rates until November at the earliest.

USDMXN: USDMXN rallied from 16.2608 to 16.4215 after Mexican inflation was a tad softer than expected (actual 0.29% m/m vs forecast 0.36%). The move was reversed in the wake of the US CPI report and USDMXN climbed to 16.4571 before inching lower.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0959 vs exp. 7.2300 (prev. 7.0956).

Shanghai Shenzhen CSI 300 fell 0.81% to 3504.71.

Fitch downgrades China credit outlook to negative from stable, reaffirms China’s A+ rating.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com