July 24, 2024

- Trading is just noise ahead of Friday PCE data.

- Preliminary Eurozone PMI data largely ignored.

- US dollar opens with a bid, but rally unconvincing.

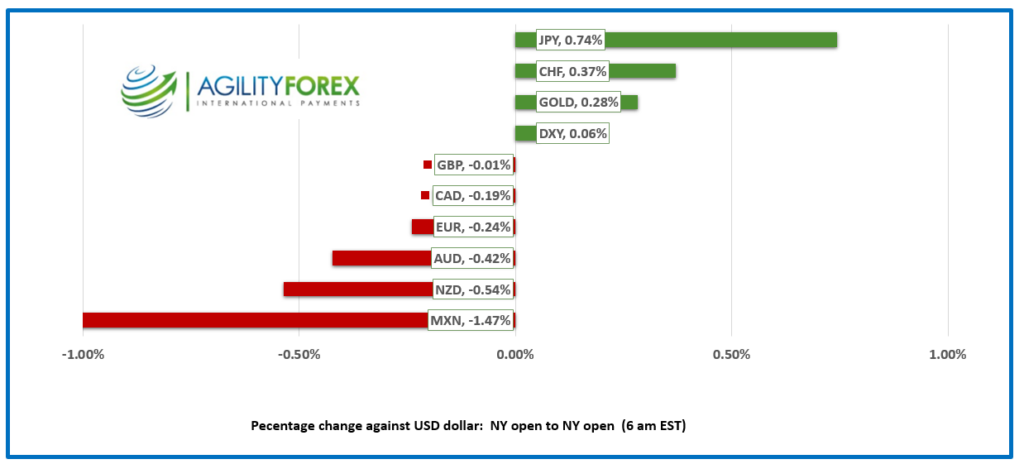

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3791, overnight range 1.3781-1.3800, previous close 1.3785

USDCAD inched higher due to general US dollar strength with expectations for the Bank of Canada to cut rates by 25 bps today not helping.

The BoC monetary policy meeting and quarterly Monetary Policy (MPR) report are the highlight for USDCADS traders. Analysts are suggesting the BoC will follow today’s rate cut with two more by year end and they will be looking to Governor Tiff Macklem and the MPR for supporting evidence.

USDCAD Technicals

The intraday USDCAD technical are bullish. The uptrend channel that began on July 11 is steep with the channel top at 1.3810 on the top and the floor at 1.3720 on a 4 hour chart. A move below 1.3750 targets the floor.

The longer term technicals are unchanged chart and suggested continued range trading in a 1.3600-1.3900 band.

For today, USDCAD support is at 1.3750 and 1.3710. Resistance is at 1.3810 and 1.3850. Today’s Range 1.3750-1.3840.

Chart: USDCAD 4 hour

Source: DailyFX

“A Dog Chasing its Tail”

Global markets are going in circles, not unlike the canine activity suggested in the headline. It’s summertime, which lately means Western Canada is ablaze, heat domes, and torrential rainstorms in Eastern Canada. And this year, the US presidential election drama. Historically, the Democrats take about a year to select their candidate for President. It consists of a series of state primaries and caucuses. Delegates are awarded to candidates based on their performance in these contests. The candidate with the majority of delegates is then officially nominated at the Democratic National Convention. Kamala Harris bypassed this process, and a handful of puppet masters anointed her as the “chosen one.”

Equity Traders on Edge

The tech stock retreat continues to reverberate through global markets after traders were unimpressed with Tesla’s results or Alphabet’s outlook. Asian equity indexes closed poorly, led by a 1.42% drop in Japan’s Topix. Australia’s ASX 200 was unchanged. European bourses are in negative territory, led by a 0.92% drop in the French CAC-40 index. S&P 500 futures are down 0.73%. The poor equity performance is giving the US dollar a bit of a risk aversion boost.

EURUSD

EURUSD extended Tuesday’s losses and fell to 1.0825 from 1.0855 before ticking higher into the NY open. The price action is noisy due to US election theatrics, soft Flash Eurozone PMI data, and the lead-up to the key US PCE Core Price index report on Friday, followed by the August 1 FOMC meeting. No one expects the Fed to cut rates then, but the probability of a 25 bps drop to 5.25-5.50% at the September 19 meeting is 91.7%.

GBPUSD

GBPUSD traded in a 1.2876-1.2913 range, with the low seen in Asia. Better-than-expected flash S&P Global UK PMI data sparked a bit of a rally, partly because analysts there said, “policymakers will likely take a cautious approach to loosening policy amid signs of inflationary pressures pivoting away from services towards manufacturing, where Red Sea shipping delays and higher freight prices are adding to costs again.”

USDJPY

USDJPY got slammed again, falling from 156.00 to 154.28 before a profit-taking bounce to 154.89 in NY. The catalysts were many and included today’s marginal decline in Jibun Manufacturing Flash PMI to 49.7 from 50.4 in June. In addition, the BoJ is expected to raise rates by 0.10 bps next week, and with the Fed in rate-cutting mood, traders continue to unwind carry-trade positions.

AUDUSD and NZDUSD

AUDUSD traded negatively in a 0.6583-0.6618 range due to weak commodity prices and AUDJPY selling pressures. The preliminary July PMI data was on the soft side. S&P Global/Judo Bank Flash Australia Composite PMI Output Index: 50.2 (June: 50.7), Services PMI Business Activity Index: 50.8 (June: 51.2), Manufacturing PMI: 47.4 (June: 47.2), a 2-month high. NZDUSD suffered a similar fate as its Aussie cousin and dropped to 0.5914 from 0.5961.

USDMXN

USDMXN climbed from 18.1474 to 18.2835 as modest risk aversion fueled broad-based US dollar gains, before retreating to 18.1895 in early NY trading. Prices are supported by an expected increase in July mid-month inflation readings today, although the increase is unlikely to prevent Banxico from cutting interest rates by 25 bps to 10.75% at its August 8 meeting.

Bitcoin (BTCUSD)

BTCUSD suffered from a slightly negative risk sentiment and traded in a 65,547-67,406 range. The “Trump-effect” is at play, with traders hoping Trump spotlights cryptocurrency when he speaks at a Nashville rally.

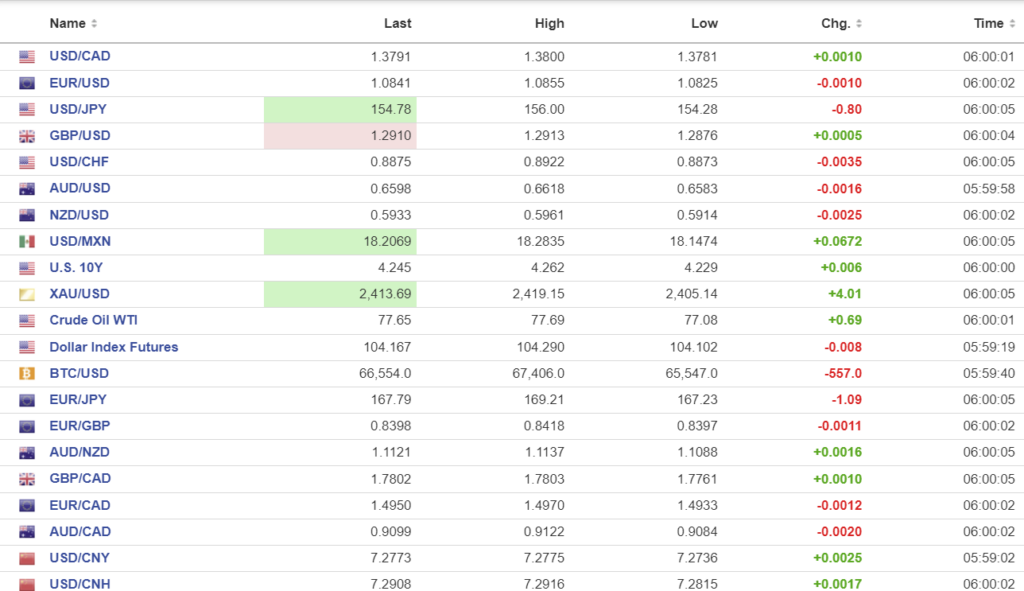

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1358 exp. 7.2795 (prev. 7.1334).

Shanghai Shenzhen CSI 300 fell 0.63% to 3418.17.

Analysts are suggesting that the prospect of Trump returning to the White House is weighing on Chinese stocks due to expectations he will increase trade pressures and tariffs on Chinese goods. There is speculation that Trump would revoke China’s Most Favoured Nation status.

Chart: USDCNY and USDCNH

Source: Investing.com