June 6, 2025

USDCAD: open 1.3678, overnight range 1.3661-1.3687, close 1.3676

USDCAD continues to trade defensively but traded in a very narrow range overnight after making a dent in the major 1.3650 support area yesterday. The selling pressure is entirely due to widespread US dollar selling pressures vs the majors. USDCAD drifted up to 1.3701 ahead of the employment reports then dropped back to 1.3686 in the immediate aftermath.

Bank of Canada Deputy Governor Sharon Kozicki spoke in Toronto yesterday and left the door open for more rate cuts. She said that with non-traditional data confirming a cooling economic pulse, the Bank is likely to remain on hold in the near term, but the groundwork is being laid for a rate cut later this year if conditions worsen.

WTI oil prices rose from 62.82 to 63.46 due to the improved risk tone following the Trump/Xi Jinping call.

Canada’s employment report showed a 8,800 rise in new jobs for May while the unemployment rate rose to 7.0% from 6.9%.

USDCAD Technicals

The intraday USDCAD technicals are unchanged from yesterday; they are bearish while trading below 1.3710 and looking for a break below 1.3650 to target the 1.3550 zone. The intraday RSIs suggest USDCAD is deeply oversold and vulnerable to a bounce toward the 1.3720-40 resistance zone.

The medium term technicals are bearish below 1the 200 day moving average at 1.4026 and it is guarded by resistance in the 1.3740 and 1.3660 area. A decisive close below 1.3600 suggests further losses to 1.3450.

For today, USDCAD support is at 1.3650 and 1.3600. Resistance is at 1.3710 and 1.3740

Today’s Range: 1.3630-1.3730

Chart: USDCAD 4 hour

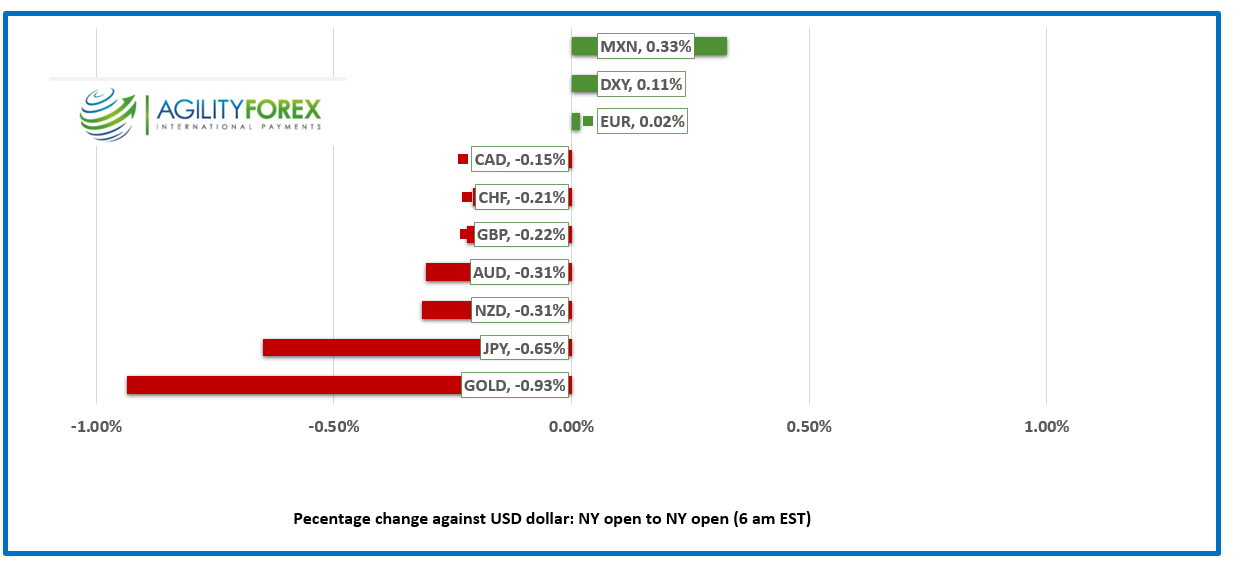

FX at a Glance

He Said, He Said

Social media feeds were blowing up after President Trump and First Friend Musk exchanged a series of inflammatory and accusatory tweets (truths) that pretty much signalled the end of the bromance. The feud appeared to have started with Musk’s reaction to the steep rise in deficit spending championed by Trump’s Big Beautiful Bill. Trump said Elon only got upset when EV subsidies were removed. Elon replied tweeting. “Without me, Trump would have lost the election” It’s a disgusting abomination that would add trillions to the deficit.” Musk stoked the fire a bit later when he tweeted “@elonmusk Time to drop the really big bomb: @realDonaldTrump is in the Epstein files. That is the real reason they have not been made public. Have a nice day, DJT!”

Republican politicians were spooked, fearing the disappearance of $290 million of campaign funding.

The feud knocked 14.26% off the Tesla (TSLA: NASDAQ) market cap.

Who Called Who

It is not clear who blinked (bet Trump), but the U.S. President and Chinese President had a ninety-minute phone call. Trump said he plans a visit to China and Xi Jinping has been invited to the White House. Trump also dropped the ban on Chinese students coming to America, while Xi Jinping agreed to export rare earth minerals as agreed on May 12. Neither Trump nor Jinping admitted to initiating the call.

Payrolls Friday.

This week’s employment data paints a picture of a slowing job market and today’s non-farm payrolls data confirmed that view. The NFP data showed the U.S. gained 139,000 new jobs in May compared to the revised down result of 147,000 in April. The unemployment rate stayed unchanged at 4.2% today, suggesting the Fed will not be motivated to cut rates before September.

Global Equities Under the Weather

Asian equity indexes closed mixed. Japan’s Topix rose 0.42% while Australia’s ASX 200 fell 0.27%. The major European bourses are flat to negative with the German DAX down 0.24% but S&P 500 futures have risen 0.78%. The 10-year Treasury yield jumped to 4.47% from 4.384% and gold (XAUUSD) is 3357.90 as of 5:40 am PT.

EURUSD

NY Open: 1.1421 Overnight Range: 1.1411-1.1458

EURUSD rallied to 1.1495 in the wake of the ECB decision yesterday, then retraced the entire move and opened in NY virtually unchanged from Thursday. The ECB cut rates by 25 bps as expected, but the press conference revealed that policymakers were in no hurry to repeat the action in July. There was the expected caveat about the uncertainty around the impact of tariffs, which could force a change in the outlook. A slew of economic data from Germany, France, and the Eurozone did not have much impact, with traders ignoring the 1.5% rise in Q1 GDP q/q, which easily topped the forecast of a 1.2% gain. The focus is on today’s U.S. NFP report, and just to keep things interesting, the $2.4 billion of 1.1400 option strikes maturing at 10 a.m. ET.

GBPUSD

NY Open: 1.3535, Overnight Range: 1.3529-1.3585

GBPUSD dipped in Asia and Europe but bounced from its low in early NY trading. Traders are awaiting the U.S. employment report. News that UK house prices fell more than expected in May weighed on the currency pair.

USDJPY

NY Open: 144.05, Overnight Range: 143.45-144.19

USDJPY climbed steadily higher with prices underpinned by a sharply weaker household spending report for April. Household spending fell 0.1% y/y rather than the expected 1.4% increase, which suggests Japanese consumers were pessimistic. Prices were also boosted by further unwinding of yen safe-haven trades after the Trump/Jinping call.

AUDUSD

NY Open: 0.6490, Overnight Range: 0.6486-0.6518

AUDUSD remained inside yesterday’s range but is trading with a negative bias due to broad U.S. dollar strength, which got a boost after Trump and Xi Jinping chatted.

NZDUSD

NY Open: 0.6028, Overnight Range: 0.6022-0.6051

NZDUSD price action mirrored that of AUDUSD and for the same reasons. Traders are awaiting today’s U.S. non-farm payrolls report for further direction.

USDMXN

NY Open: 19.1476, Overnight Range: 19.1375-19.1669

USDMXN extended losses yesterday then consolidated them overnight on the back of a major thaw in the U.S./China trade war. The USDMXN downtrend channel from the middle of April is intact while prices are below 19.3700 and looking to test 19.0000.

China

PBoC fix: 7.1845 vs exp. 7.1935 (Prev. 7.1865)

Shanghai Shenzhen 300 fell 0.09% to 3873.98

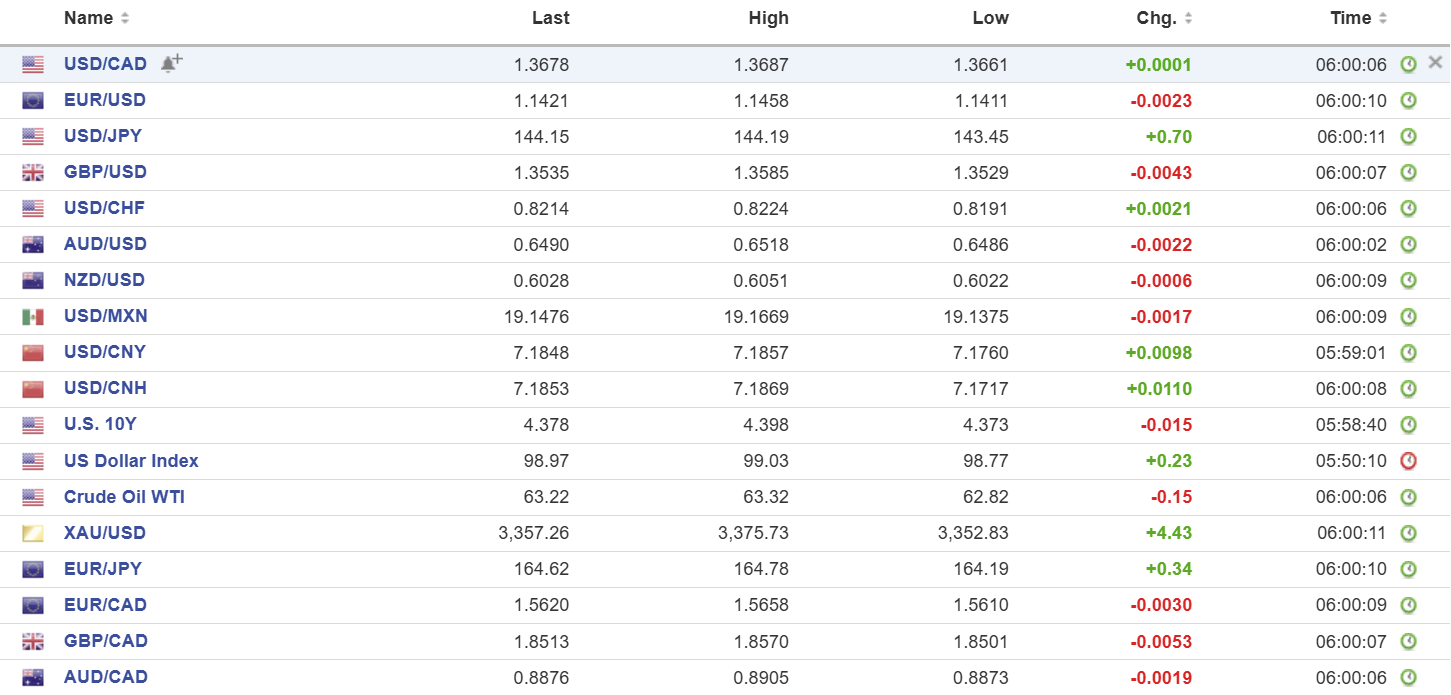

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.

–