July 3, 2025

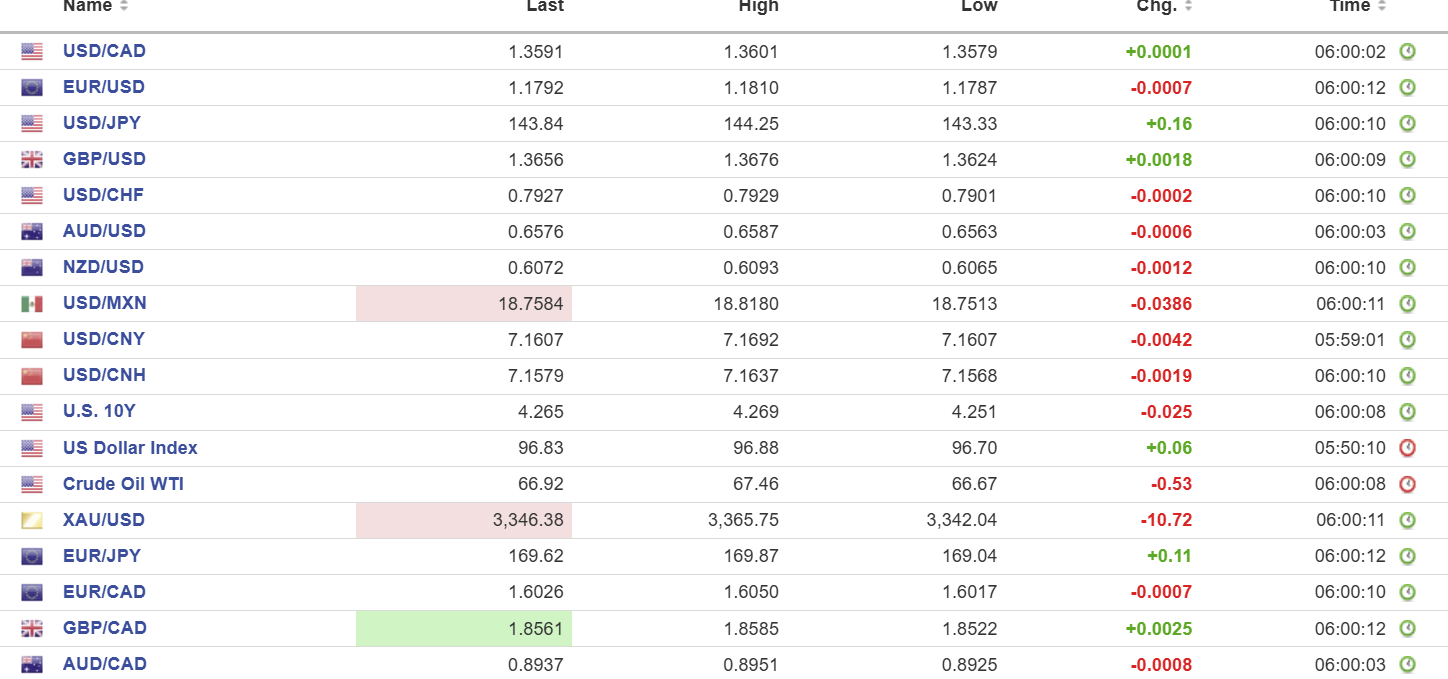

USDCAD open 1.3591, overnight range 1.3579-1.3601, close 1.3593

USDCAD continues to retreat due to broad-based US dollar selling pressure after analyts and traders now believe the Fed will cut US rates three times in 2025, taking the benchmark rate to 3.75 in December. However, traders will be re-thinking that view following today’s US employment numbers.

The non-farm payrolls whisper number of 96,000 proved to be a losing guess. NFP rose by 147,000, which topped last month’s number, and it was also higher than the consensus forecast of 110,000. Weekly jobless claims also rose less than expected (actual 233,000 vs 237,000 last week). More importantly, to Fed Chair Powell’s view is that the unemployment rate declined to 4.1% (forecast 4.3%, previously 4.2%).

USDCAD popped to 1.3624 from 1.3588 on the news but it is already retreating.

A key driver of USDCAD weakness is the sharply narrowing CAD/US interest rate spreads. The 10-year CAD/US spread has narrowed from -1188.3 bps a month ago to -89.7 today. The 2-year yield has compressed to -110.6 from -134.2 in the same period.

Oil prices are trading in a 66.67-67.46 range. Oil prices spiked to 67.58 yesterday after Iran halted IAEA cooperation and positive US-Vietnam trade deal news. The move didn’t last thanks to a 3.8-million-barrel build in US crude stockpiles and concern about OPEC increasing output by 411,000 bpd at their next meeting.

Canada’s International trade deficit narrowed to $5.9 billion, as expected. (May -$7.14 billion).

USDCAD Technical Outlook:

The intraday technicals are bearish while trading below 1.3640 and looking for a break of 1.3540 to extend losses to 1.3510. However, momentum indicators suggest prices are at over-sold levels, which could limit downside, for now.

The longer-term outlook is decidedly bearish with the March downtrend line at 1.3750 and guiding prices lower.

For today, USDCAD support is 1.3540 and 1.3510. Resistance is 1.3620 and 1.3650. Today’s Range 1.3520-1.3620

Markets in Brief

The Trump Show is the only ticket in town. His “Big Beautiful Bill” has reportedly secured enough votes in the House of Representatives to pass, ensuring middle class Americans will benefit from tax cuts while poorer Americans lose access to health care—at least those that he hasn’t deported.

Trump suffered another nasty bout of verbal diarrhea overnight. His TruthSocial account was rife with effusive praise for loyalists and vitriol for anyone who didn’t share his opinion. Once again, he set his sights on Fed Chair Jerome Powell, tweeting “Too Late” should resign immediately!!!” then posting a link to a Bloomberg story: “Fed Chair Should Be Investigated by Congress, FHFA Head Says” https://www.bloomberg.com/news/articles/2025-07-02/fed-s-powell-should-be-investigated-by-congress-fhfa-head-says

Data Dump Day

Friday, US Markets are closed for Independence Day. Other key reports include ISM Services PMI (forecast 50.5 vs 50 in May)

Taking Stock

Asian equity indexes closed close to flat except the Hong Kong Hang Seng, which lost 0.63%.

European bourses are mixed to flat, with the UK FTSE 100 index the outlier, rising 0.49%. S&P 500 futures rose, post-NFP and are up 0.31%. while gold (XAUUSD)fell from 3350.81 to 3316.68 after the NFP data. The US 10-year Treasury yield popped from 4.256% to 4.382%.

EURUSD

EURUSD continued to rally, rising from 1.1787 to 1.1810, supported by better-than-expected Eurozone Services PMI (actual 50.5, previous 50) and Composite PMI (actual 50.6, previous 50.2). Also, German and French PMI readings topped expectations but remain in contraction territory. EURUSD technicals are bullish with the uptrend line from March intact while prices are above 1.1550. According to the Financial Times, this rally is causing some concern among policymakers at the ECB, with some wondering if rates should be cut further and faster to help offset the gains.

GBPUSD

GBPUSD dropped sharply yesterday, falling from 1.3754 in Asia to 1.3564 on UK political drama, which was exacerbated by the very weak US ADP Employment Change report. Reportedly, traders got it into their heads that UK Chancellor Rachel Reeves (who ING describes as fiscally conservative) would get fired. Prices recovered after Prime Minister Starmer (somewhat belatedly) gave her his full backing. The rally picked up steam overnight, with GBPUSD climbing from 1.3624 to 1.3676 supported by a sharp rise in UK June Services PMI (actual 52.8, May 50.9).

USDJPY

USDJPY traded in a 143.33-144.25 range with prices on the defensive ahead of the looming US data dump and expectations for a faster pace of Fed rate cuts. USDJPY was also pressured after BoJ board member Hajime Takata said the BoJ should resume hiking rates.

AUDUSD

AUDUSD remains firm in a 0.6563-0.6587 range. Prices are underpinned by expectations of a soft US Non-Farm Payrolls report which, if it occurs, will boost Fed rate cut hopes and sink the greenback. US budget drama and ongoing tariff theater will also impact trading.

NZDUSD

NZDUSD continues to consolidate last week’s gains in a 0.6065-0.6563 range. Prices slipped from the top of the range after the China Caixin Services PMI rose less than expected. General US dollar weakness and RBNZ hints that its easing cycle was near an end supported prices. US political drama around its budget bill alongside a slew of economic reports including NFP has contained price action overnight.

USDMXN

USDMXN drifted higher in a 18.7561-18.8180 range due to broad US dollar strength ahead of today’s US massive data dump, that includes Non-Farm Payrolls. Mexico’s Foreign Minister announced that a delegation would travel to Washington, D.C. for high-level talks on security, migration, and trade.

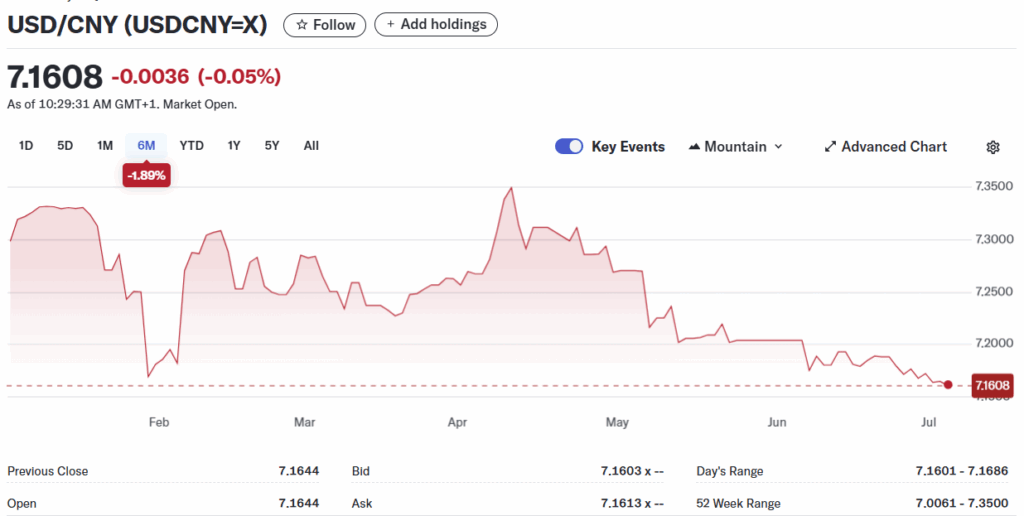

USDCNY

PBoC fix: 7.1523 vs exp. 7.1618 (Prev. 7.1546).

Shanghai Shenzhen 300 rose 0.62% to 3968.07

Caixin June Services PMI 50.6 (forecast 51, previous 51.1). Composite PPI 51.3 (previous 49.6). The services PMI expansion was the slowest expansion since September.

Wang Zhe, Senior Economist at Caixin Insight Group, wrote, “Recently, major macroeconomic indicators have shown divergence, with consumption in certain sectors increasing beyond expectations, while the momentum of growth in investment and industrial production has weakened. We must recognize that the external environment remains severe and complex, with increasing uncertainties. The issue of insufficient effective demand at home has yet to be fundamentally resolved.”

Reuters reports that the US lifted some restrictions on exports to China for chip design software developers.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo