August 1, 2025

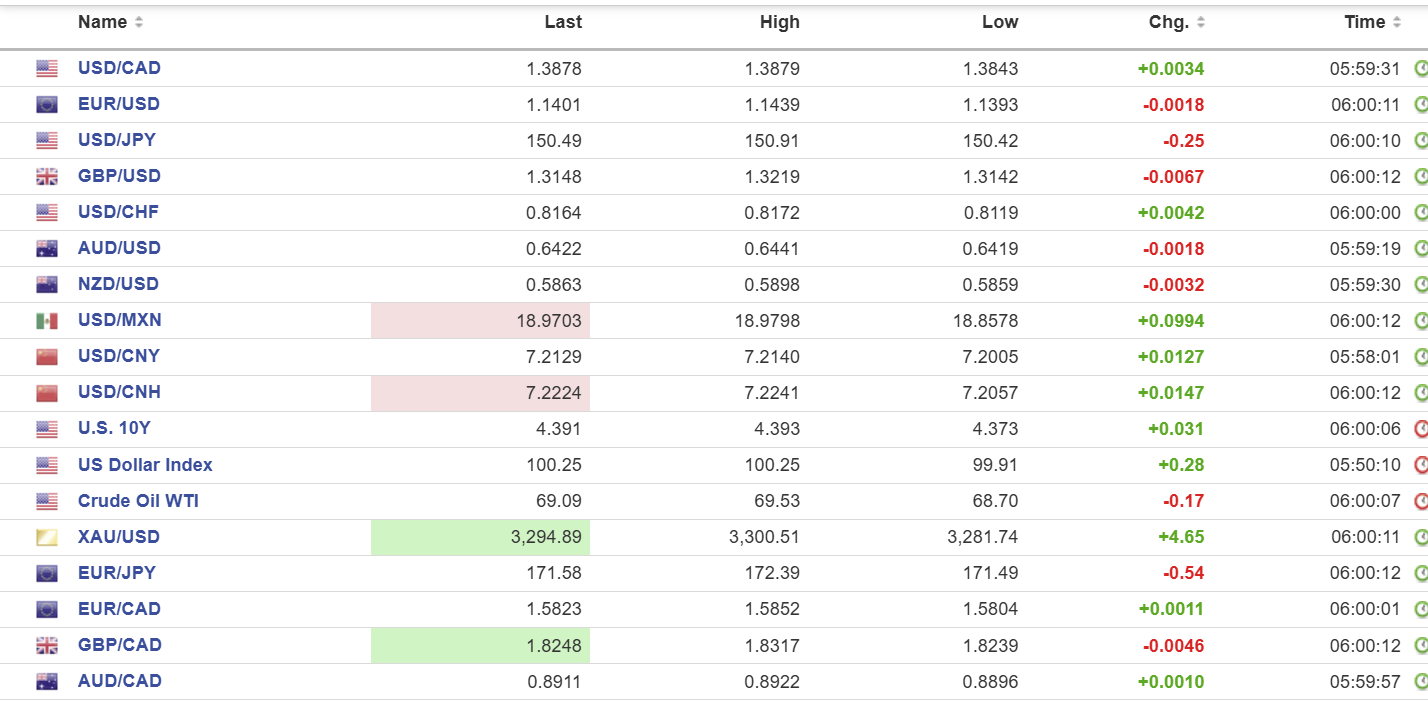

USDCAD open 1.3878, overnight range 1.3786-1.3876, close 1.3856

USDCAD plunged from 1.38 75 to 1.3775 after a weaker than expected US nonfarm payrolls report raised the odds for a Fed rate cut in September. Traders were caught long and wrong, and they bailed.

Trump just dumped on Canada. The uber-vain, nearly-octogenarian President—whose cognitive decline was on full display two weeks ago when he blamed Biden for appointing Fed Chair Jerome Powell—slapped a 35% tariff on all Canadian imports not covered by the USMCA effective today. Meanwhile, while the major source of illicit drugs to the US, Mexico, earned a 90-day reprieve.

His rationale? According to the laughably misnamed “White House Fact Sheet,” it’s “to address the flow of illicit drugs across our Northern Border.”

If Trump wants to play that game, Canada could just as easily address his fantasy problem with a fantasy solution. Prime Minister Carney could instruct Hydro-Québec and Ontario Hydro to pull the plug on electricity exports to the U.S.—after all, who knows what those crafty smugglers are hiding in the power lines? In addition, Alberta’s Keystone pipeline taps would be turned off to ensure no fentanyl is hitching a ride.

Trump’s tariff action was well-telegraphed and the USDCAD reaction has been muted—so far.

However, the outlook is rather grim. The Fed sees no need to lower rates while the BoC doesn’t have that option. Yesterday’s May GDP data showed that economic growth was negligible and likely to get worse. Canadian unemployment is already elevated, and tariff-related layoffs will exacerbate the situation.

Many analysts are claiming that raising the tariff to 35% is not a big deal because, per RBC Economics, the USMCA agreement covers almost 90% of Canadian exports into the US. Maybe so, but they are extremely vulnerable to a Trump late-night bathroom tweet. After all, Mr. MAGA (Memory Ain’t Great Anymore) could forget his latest tariff move and do it again with a much higher rate.

WTI traded sideways in a 68.70–69.53 range, with gains hampered by a stronger US dollar and risk aversion from the tariff onslaught.

USDCAD Technical Outlook:

The intraday technicals are bullish while prices are above 1.3860 (100 day moving average is 1.3858) and are looking for a test of the 1.4022, the 200-day moving average, but at the moment USDCAD looks a tad overbought with RSIs at extreme levels.

Longer term, the trend is higher but the 200-day moving average at 1.4022 may be formidable resistance initially. However, downside corrections should be contained at 1.3660.

For today, USDCAD support is 1.3770 and 1.3740. Resistance is 1.3910 and 1.3960. Today’s Range: 1.3770-1.3870

Spotlight on Data

Nonfarm Payrolls rose a less-than-expected 73,000 compared to estimates for 110,000 and 147,000 last month, while the unemployment rate ticked up to 4.2% from 4.1%, as expected.

The news knocked the greenback lower and sent 10-year Treasury yields tumbling from 4.40% to 4.29%.

Later in the day, the ISM Manufacturing PMI index is expected at 49.5 from 49, with the prices paid component rising to 70 from 69.7. Michigan Consumer Sentiment rounds out the data dump, and it is expected to improve to 62 from 61.8.

Fed Governor Waller’s Audition

The surprise drop in NFP boosted Governor Waller’s credibility after he dissented at Wednesday’s FOMC meeting. He justified his view in a speech today, saying that he believes current rates are too restrictive given weak GDP growth, stalling job gains, and inflation near target. He argued tariff-driven price increases are temporary and shouldn’t delay rate cuts if inflation expectations remain anchored.

Then, he warned that waiting risks falling behind the curve if the labor market suddenly deteriorates. Cut rates now, and it gets flexibility later. What he didn’t say in public was, “Hey Donnie, did I get Powell’s job?”

Taking Stock

Equity traders were unimpressed with Trump’s tariff actions. S&P 500 futures are down -0.93%. European bourses are bleeding. The French CAC-40 is down 2.36%, the German DAX has lost 2.11%, and the UK FTSE 100 has lost 0.58%. The US dollar index firmed to 100.12 pre-NFP, then dropped to 99.31 post-data. Gold (XAUUSD) spiked from 3300.10 pre-data to 3343.37 afterwards, as of 5:45 PDT.

EURUSD

EURUSD remained under pressure and traded in a 1.1393–1.1439 range, then soared to 1.1550 after the US data. Eurozone Manufacturing PMI and inflation data presented no surprises.

GBPUSD

GBPUSD added to this week’s decline and traded in a 1.3142–1.3219 band but popped to 1.3297 after NFP. However, gains are limited due to dovish expectations for next week’s BoE meeting and soft July PMI data.

USDJPY

USDJPY traded sideways in a 150.32–150.91 range before plunging to 148.66 in NY. That’s because traders boosted the odds for a Fed rate cut in September, which helps take the sting out of downgraded odds for BoJ rate hikes. The post-data slide in the US 10-year Treasury yield back to Wednesday’s level helped. Manufacturing PMI ticked up to 48.9 from 48.8 in June.

AUDUSD

AUDUSD was steady in a 0.6419–0.6441 range, with prices supported by AUDNZD demand, but then rallied further to 0.6484 in NY. Additional gains may be a struggle after soft Manufacturing PMI (actual 51.3 vs. 51.6 in June).

USDMXN

USDMXN rallied from 18.8578 to 18.9335 then plunged to 18.7775 on increased odds for a Fed rate cut in September.

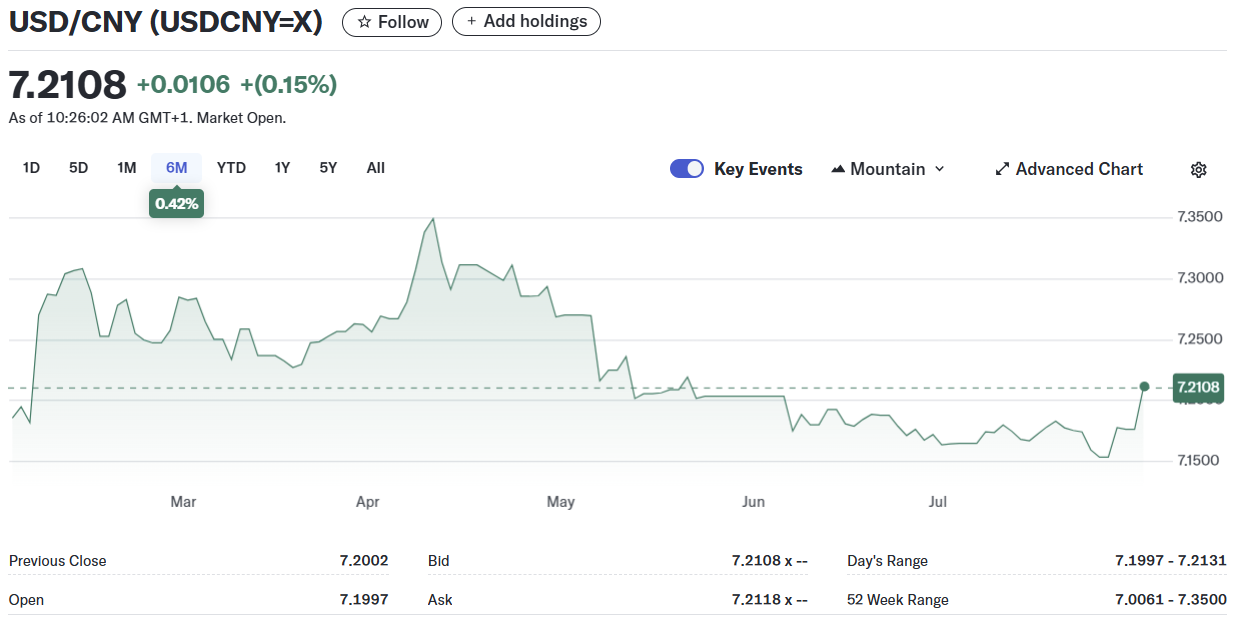

USDCNY

PBoC fix: 7.1496 vs exp. 7.2033 (Prev. 7.1494)

The Shanghai Shenzhen CSI 300 fell 0.51% to 4054.93

Caixin June Manufacturing PMI 48.2 (forecast 48.4, May 48.4)

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics