August 12, 2025

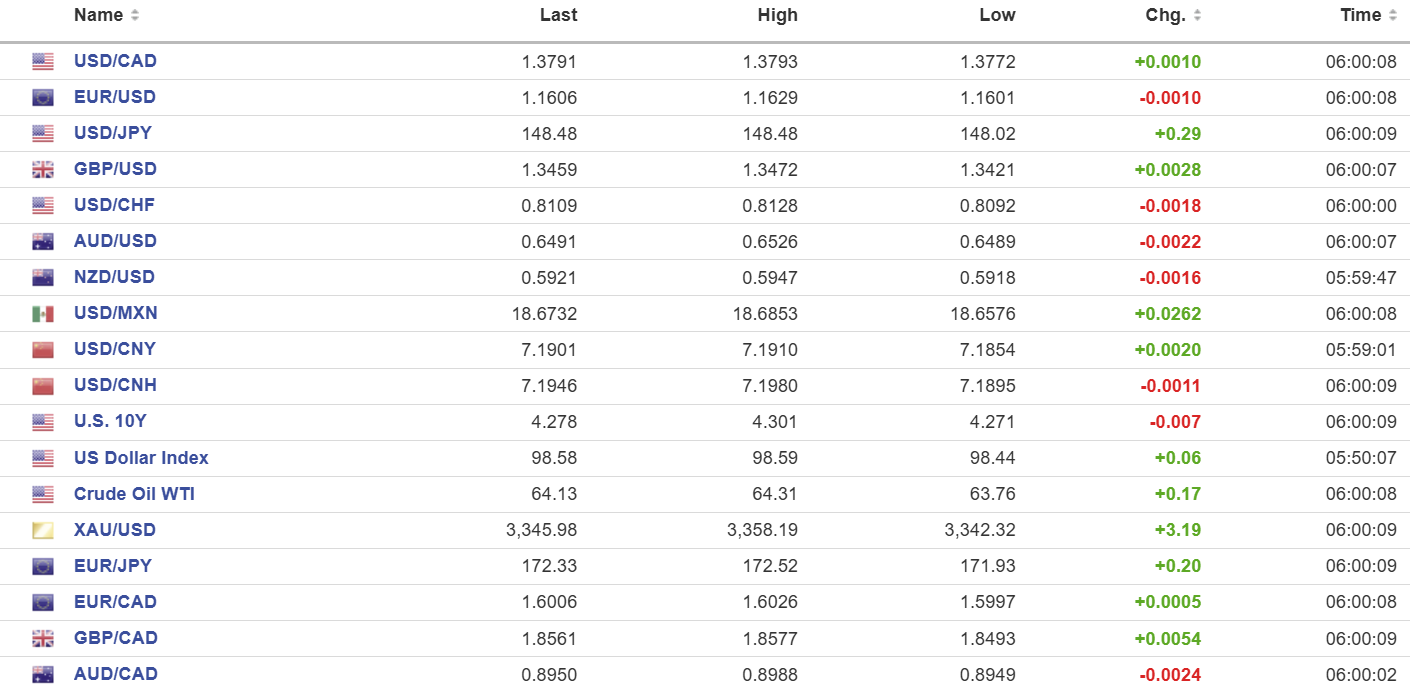

USDCAD open 1.3791, overnight range 1.3772-1.3806 close 1.3780

USDCAD traded quietly, albeit with a modest bid and rose to 1.3806 ahead of today’s US inflation numbers, which, when all is said and done, will not be a big deal. And they weren’t. US inflation was close to expectations and USDCAD retreated to 1.3778 following the news.

There are many more inflation-related reports released before the September 17 FOMC meeting.

USDCAD direction is at the mercy of broad US dollar moves, with the next top-tier domestic data (July CPI) not available until next Tuesday.

WTI oil is slightly higher, trading in a 63.76-64.34 range. Prices got a bit of a boost after Trump announced a 90-day extension on the China tariff pause. Trump is threatening new tariffs on China for buying Russian crude, and recent reports suggesting China is reducing imports of Saudi crude in favour of Russian oil may exacerbate the situation.

USDCAD may be choppy around the 10:00 am option expiry window as $1.1 billion of 1.3750 strikes roll off and $772 million of 1.3785 strikes mature.

USDCAD Technical Outlook:

The intraday technicals are little changed from yesterday—bullish while trading above 1.3740 and looking to break above resistance in the 1.3830 area to extend gains to 1.3880. A move below 1.3740 targets 1.3660.

Longer term, USDCAD technicals are bearish but downward momentum is stalling. A break above 1.3830 targets 1.3915 while a topside failure risks a return to 1.3600.

For today, USDCAD support is 1.3740 and 1.3710. Resistance is 1.3810 and 1.3830. Today’s Range: 1.3740-1.3820

Inflation in Focus

US CPI rose 0.2% m/m in July, as expected and a tick below the June’s 0.3% result. The year over year result was 2.7%, unchanged from June but below the 2.8% forecast. Core-CPI was a wrinkle. It rose 0.3% m/m as expected (June 0.2%) but the year over year result at 3.1% was higher than expected (3.0%) and June’s 2.9% increase.

Taking Stock

European bourses are trading higher post-CPI. The UK FTSE 100 index is up 0.18 %, the German DAX is flat and the French CAC-40 index has gained 0.56%. S&P 500 futures are up 60% as of 5:52 am PDT. The U.S. dollar index (DXY) dropped from 98.52, pre-data, to 98.20 in the aftermath. while gold rose to 3351.00 from 3345.98 at the NY open. The US 10-year Treasury yield is 4.27%.

EURUSD

EURUSD traded lower in a 1.1601-1.1629 range, weighed down by concern ahead of US inflation numbers and disappointing ZEW Survey data. The survey suggests respondents were less than enamoured with the EU–US trade deal and softer Eurozone growth expectations.

GBPUSD

GBPUSD traded in a 1.3421-1.3472 range, hitting the top after the headline employment figures, then dropping to 1.3458 as the details were digested. The UK added 105,000 jobs in the three months ending in June. Today’s data did nothing to resolve the rate cut/rate pause debate.

USDJPY

USDJPY inched higher in a 148.02-148.47 range and is at the top of the band in NY ahead of today’s US inflation numbers. Traders appear to have dismissed last week’s BoJ comments that rates will rise if growth and inflation rise, as they expect.

AUDUSD

AUDUSD is at the bottom of its 0.6490-0.6526 range in early NY. The RBA cut its benchmark rate to 3.60%, which was a universally expected move due to falling inflation. A September 30th cut is on the table due to staff forecasts that “underlying inflation will continue to moderate to around the midpoint of the 2–3 per cent range, with the cash rate assumed to follow a gradual easing path.” NAB Business Conditions Index dipped to 5 from 9 in July, while Business Confidence rose to 7 from 5.

USDMXN

USDMXN is consolidating yesterday’s gains in an 18.6575-18.6853 range ahead of this morning’s US inflation report. USDMXN remains defensive due to Trump delaying tariffs on non-USMCA imports to the US and due to the wide Mexico/US interest rate differentials.

USDCNY

PBoC fix: 7.1418 vs exp. 7.1901 (Prev. 7.1405)

The Shanghai Shenzhen CSI 300 rose 0.52% to 4143.82

Trump confirmed the rumours and gave China another 90 day extension (to November 9) to arrive at a deal with the US or face tariffs of 145%. However, Trump may levy additional tariffs to punish China for buying sanctioned Russian oil.

China urges firms not to use Nvidia H20 chips suggesting that they pose “security concerns.”

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics