September 23, 2025

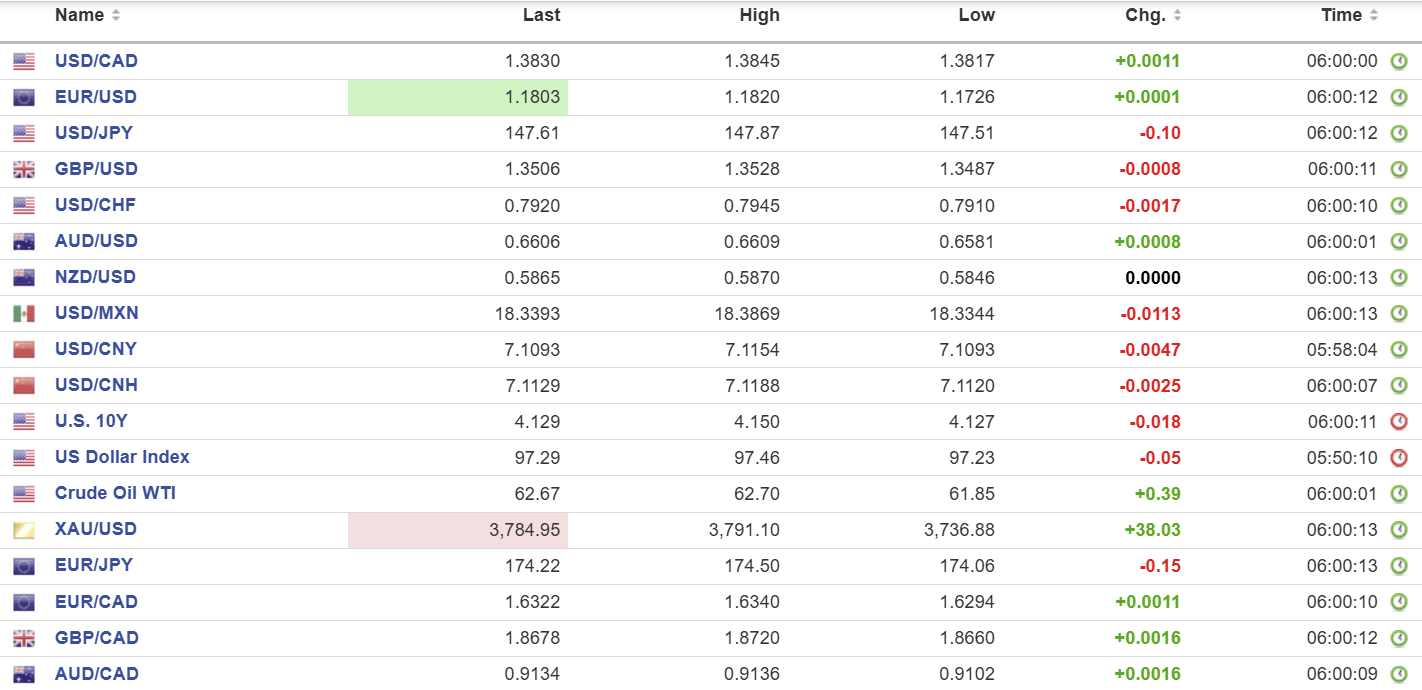

USDCAD open 1.3830, overnight range 1.3817-1.3845, close, 1.3819

USDCAD posted gains despite the US dollar slumping against the rest of the G-10 major currencies. That could be because on July 30, Trump threatened that it would be hard to make a trade deal if Canada backed statehood for Palestine. Mark Carney has, and US politicians are promising consequences.

The risk of renewed US trade hostility is a reality and that is reflected in the Loonies underperformance against the commodity currency bloc.

WTI oil is at the top of its 61.85-63.02 range with traders weighing risks of addition Russian crude sanctions against rising production and inventories.

The Canadian data releases consist of the housing price index) while US S&P Global PMI data is on tap

USDCAD Technical Outlook:

The intraday technicals are bullish while trading above 1.3810 and looking for a break above the 1.35850-60 resistance zone to extend gains to the 1.3900-10 area. The break above the 100-day moving average (currently 1.3763) targets the 200-day m.a at 1.4003.

The medium-term technicals suggest further range trading in a 1.3600-1.3900 band albeit with an upside bias.

For today, USDCAD support is 1.3810 and 1.3770. Resistance is 1.3860 and 1.3890. Today’s Range: 1.3790-1.3890

Trump Addresses the UN Today

President Trump is the featured speaker at the United Nations today at 9:50. Trump will regale the UN delegates with tales of his “magnificent achievements, and (according to press secretary Leavitt) talk about how “globalist institutions have significantly decayed the world order.” That follows on a Reuters report that the Trump administration is considering slapping sanctions on the entire International Criminal Court.

Trump’s speech completes the comedy portion of today’s program while Fed President Jerome Powell’s speech to the Greater Providence Chamber of Commerce is the drama. Unfortunately, it’s unlikely that his economic outlook will be any different than it was last week.

Taking Stock

Wall Street closed higher led by Nasdaq gains after Nvidia and Open AI announced a $100 billion deal to build data centers. It is a cash (Nvidia’s) for Open AI equity deal. The news helped Australia’s ASX 200 close 0.40% higher. Japan’s Topix was closed for a holiday. The Hong Kong Hang Seng closed down 0.70% ahead of a major typhoon making landfall.

As of 7:10 am EDT, European equities are in positive territory led by a 0.66% rise in the French CAC with the German Dax rising 0.20%, and the UK FTSE 100 and S&P 500 futures are flat. The US dollar index (DXY) is 97.33 while Gold (XAUUSD) posted a new record high at 3791.10. The US 10-year Treasury yield sits at 4.131%.

EURUSD

EURUSD rallied from 1.1726 in Asia to 1.1820 in Europe before drifting down to 1.1801 in early NY trading. Eurozone PMI data was mostly positive although Germany’s manufacturing PMI dipped back into contraction territory, falling to 48.5 from 50 in August. The ECB chief economist said the eurozone was on a growth path but still a long way from seeing any momentum.

GBPUSD

GBPUSD is consolidating yesterday’s gains in a 1.3487-1.3528 range after hitting the session low in the wake of disappointing PMI data. Flash Composite PMI fell to 51.0 in September, from 53.5 in August. Chris Williamson, Chief Business Economist at S&P wrote “September’s flash UK PMI survey brought a litany of worrying news including weakening growth, slumping overseas trade, worsening business confidence and further steep job losses.” Talk of higher UK taxes is not helping sentiment.

USDJPY

USDJPY was uninspired in a 147.51-147.87 range partly because it is a public holiday in Japan. The currency pair continues to be supported by political uncertainty ahead of the Japanese Liberal Democratic Party (LDP) leadership election on October 4. Rising US 10-year Treasury yields acted as a drag on gains.

AUDUSD

AUDUSD traded in a 0.6581-0.6608 range with the session low seen following soft PMI readings. September Manufacturing PMI was 51.6 vs 53 in August, while Services PMI came in at 52 compared to 55.8. Prices rebounded in Europe on the back of broad US dollar weakness vs the majors.

USDMXN

USDMXN traded in a 18.3349-18.3869 range albeit with a slightly negative bias ahead of domestic July retail sales data (forecast 1.6% y/y vs June 2.5%). USDMXN continues to trade with a negative bias supported by news on Friday that the IMF upgraded its Mexican GDP outlook to 1.0% in 2025, up from -0.3% in April. The GDP forecast for 2026 was raised to 1.5% from 1.4%. The IMF noted that a favourable US-Mexico trade deal would further boost its growth prospects.

USDCNY

PBoC fix: 7.1057 vs exp. 7.1066 (Prev. 7.1106)

Shanghai Shenzhen CSI 300 fell 0.06% to 4519.78.

PBoC leaves rates its 1-year and 5-year Loan Prime Rate (LPR) unchanged as expected.

China buys 10 cargoes of Argentina soybeans after Argentina dropped grain export taxes, which is 10 cargoes that US farmers do not get to sell to China.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics