September 26, 2025

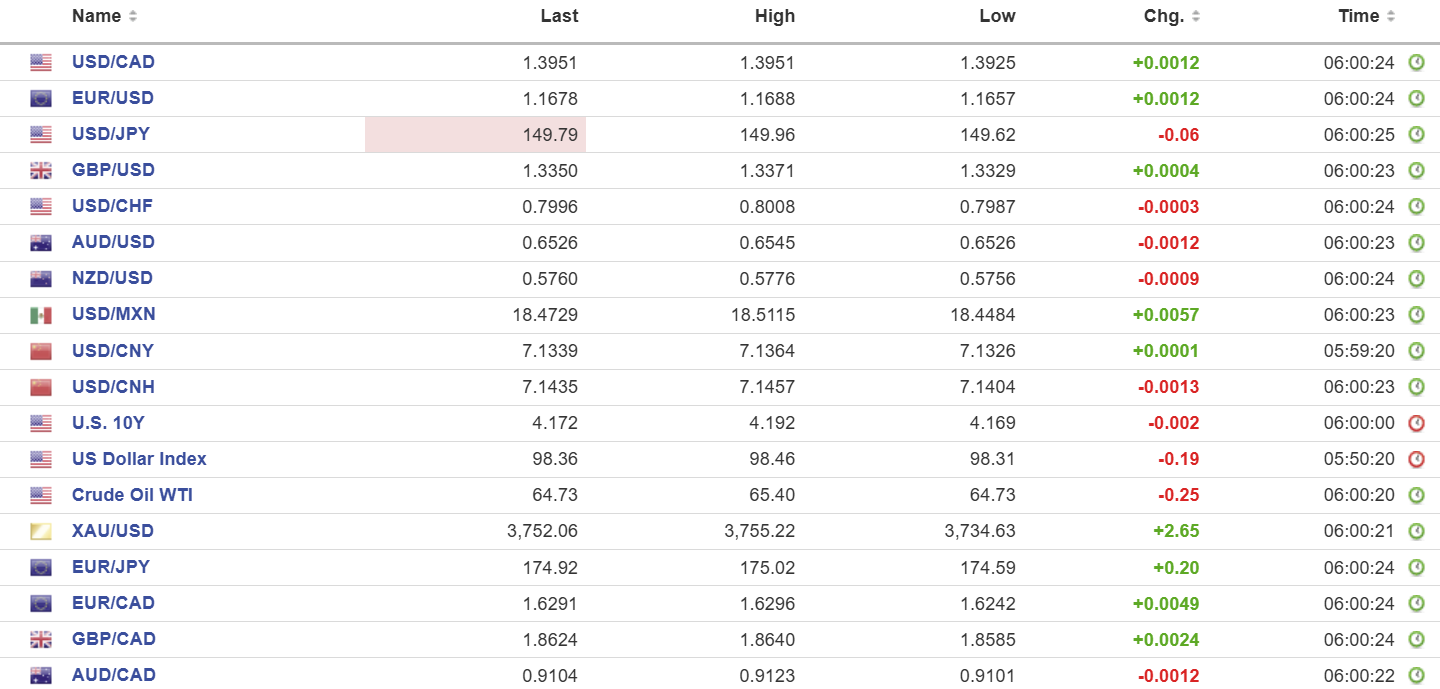

USDCAD open 1.3951, overnight range 1.3925-1.3959, close, 1.3942

USDCAD is gnawing through significant recent levels with the latest gains spurred on by yesterday’s US data. Weekly jobless claims, durable goods orders and weekly jobless claims reports suggested that the Fed could be less aggressive in trimming rates.

Trump’s latest tariff salvo on pharmaceuticals, heavy trucks and furniture spooked traders overnight, even though US courts have ruled levying tariffs exceeds his authority.

Today’s July GDP data was a tad better than expected, rising 0.2% m/m in July (forecast 0.1%) and August growth is expected to be unchanged. The report suggests the current recovery lacks depth and durability. July’s GDP bounce looks good on paper (+0.2%), but the momentum is narrowly concentrated in energy, pipelines, and autos.

And to keep things interesting, $1.0 billion of USDCAD 1.3955-65 option strikes expire at 10:00am

USDCAD Technical Outlook:

The intraday technicals are bullish while trading above 1.3895 and are looking for a sustained break above 1.3951 (the 61.8% retracement of the 2024/2025, 1.3308-1.4630 range) to target the 200-day moving average at 1.3998. However, the momentum indicators are screaming “overbought” and a reversal to 1 the 1.3880-1.3900 area is likely.

The medium-term technicals are bullish while prices are above 1.3760 (100 day moving average) and pointing to a test of 1.4000. A decisive topside break puts 1.4110 in play.

For today, USDCAD support is 1.3910 and 1.3870. Resistance is 1.3970 and 1.4020. Today’s Range: 1.3910-1.4010

Black Hawk Down

European leaders put Russia on notice—violate our airspace again and we will shoot down your planes. The question that those leaders should be asking is, “will the first Russian plane shot out of the sky be flown by the Russian equivalent of Archduke Ferdinand?” Apparently, Russia’s military didn’t get the message as several unidentified drones were seen flying over Danish airports.

Another Trumpster Fire

The fact that only a month ago the U.S. Court of Appeals for the Federal Circuit ruled that the majority of tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were illegal did not deter Trump from unleashing another barrage of tariffs yesterday. Effective October 1, he slapped 100% duties on branded drugs, 50% on heavy trucks, and another 30–50% on everything from bathroom vanities to kitchen cabinets and furniture.

As usual, the details are vague, and the Administration has not said if countries that have recently signed trade deals will face the new levies.

If TikTok had to be sold to U.S. investors because its Chinese ownership was considered a national security threat, will the Europeans and other nations ban TikTok because U.S. ownership is just as big an issue?

The Fed is Driving the Bus

The latest tariff announcements are merely unsettling for markets, but today’s U.S. PCE inflation data proved to be a non-event. Core-PCE data rose 2.9% y/y in August as expected, which is unchanged from July. The takeaway is that although inflation didn’t rise, it isn’t falling either. Michigan Consumer Sentiment is due later today.

The US dollar did not react to the news.

Taking Stock

Asian equity indexes closed flat to negative. Japan’s Topix posted a record high then finished the session up 0.5% while Australia’s ASX 200 gained 0.17%. Hong Kong’s Hang Seng index fell 1.35% mainly because of the latest Trump tariffs.

As of 5:45 am PDT, European equity traders have dismissed the noise coming from Washington. The German DAX is up 0.65%, the French CAC-40 index has gained 0.77%, and the UK FTSE 100 index is up 0.53%. S&P 500 futures have risen 0.45%. The U.S. dollar index (DXY) is 98.37, Gold (XAUUSD) is 3752.74 and the U.S. 10-year Treasury yield sits at 4.165%.

EURUSD

EURUSD is consolidating in a 1.1657–1.1688 range after yesterday’s losses following robust U.S. growth and employment data. EURUSD may rebound on soft U.S. PCE data but increased tensions with Russia may limit gains.

GBPUSD

GBPUSD is trading in a 1.3329–1.3371 band, and yesterday’s U.S. data was just another negative for sterling. GBPUSD is under pressure from UK debt and budget woes, weak PMI data earlier in the week, and mixed Bank of England guidance.

USDJPY

USDJPY rallied yesterday and consolidated the gains in a 149.62–149.96 range. The rally is fueled by U.S./Japan interest rate differentials as the 10-year U.S. Treasury yield climbed from 4.099% on Wednesday to 4.192% today. Tokyo Core-CPI rose 2.5% y/y compared to 3.0% previously.

AUDUSD

AUDUSD is at the bottom of its 0.6521–0.6545 range on profit-taking and the latest tariff news sparking fresh U.S. dollar demand.

USDMXN

USDMXN chopped in an 18.4484–18.5115 range and is trading at 18.5010 in early NY. The gains occurred on the back of yesterday’s U.S. data which downgraded hopes for aggressive rate cuts. Banxico didn’t help. It cut its benchmark rate to 7.50% from 7.75% as expected, citing weak economic growth and moderating inflation to justify the move.

USDCNY

PBoC fix: 7.1152 vs exp. 7.1439 (Prev. 7.1118)

Shanghai Shenzhen CSI 300 fell 0.95% to 4550.05.

China may be facing 20 new anti-dumping probes from Europe.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics