November 25, 2025

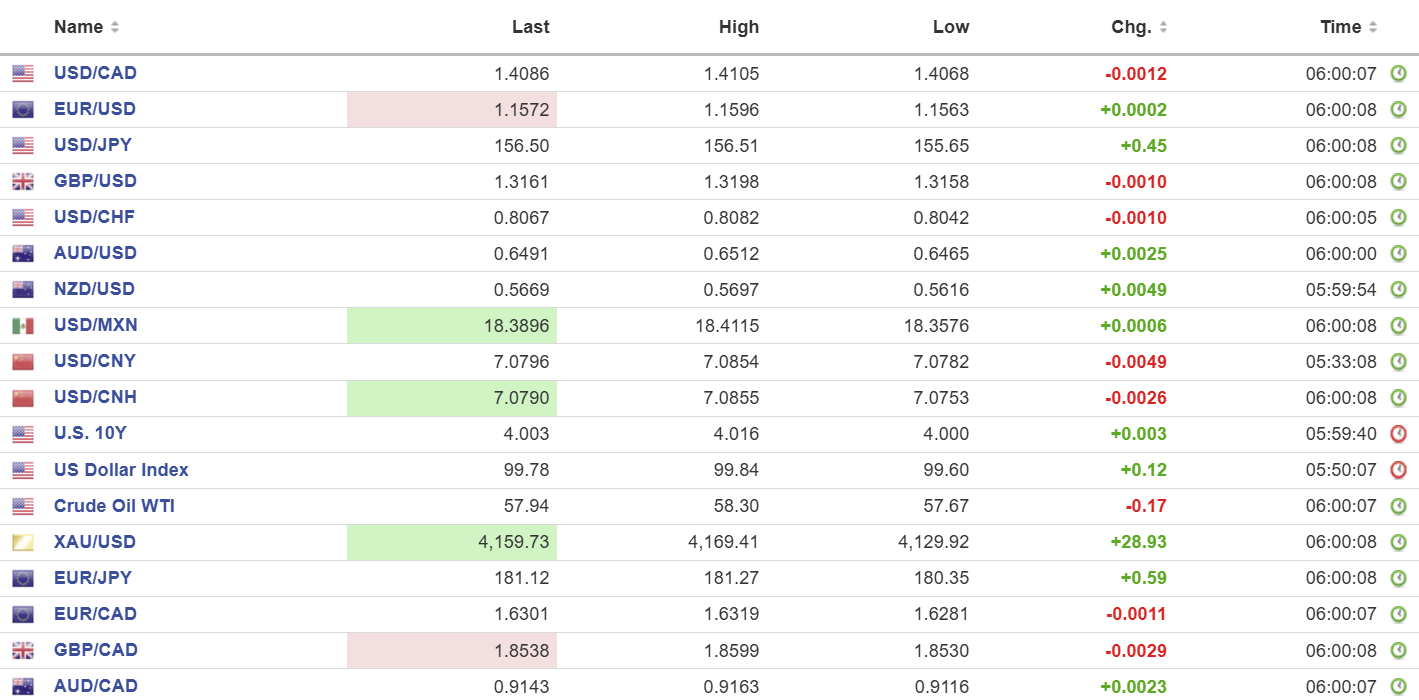

USDCAD open: 1.4086, overnight range 1.4068-1.4105, close 1.4101

USDCAD retreated on the back of broad-=based US dollar selling pressure but the downside appears limited. The Canadian economy is weak, although the BoC believes inflationary pressures are contained. Economic growth is expected to be very slow in 2026 due to what the BoC describes as “structural damage” to the economy from tariffs.

Canada gave Stellantis around $105 million to retool two Ontario plants and Stellantis took the money and fled to the US. The government ordered Stellantis executives to explain themselves to a parliamentary committee yesterday. Stellantis blew them off. That doesn’t bode well for the Canadian auto sector, especially if Ford, GM and others decide to appease Trump.

WTI oil prices traded in a 57.67-58.30 band weighed down by Opec production increases. Traders are also concerned about Russian crude returning (legally) to the market in an environment that is already oversupplied.

Todays US data: September Durable Goods Orders(actual 0.5%, August 2.9%), Initial Jobless claims 216,000, 4-week average 223,700. The results were ignored.

USDCAD Technical Outlook

The intraday USDCAD technicals are modestly bearish while trading below 1.4005 but support in the 1.4060 area was tested and it held. A move above 1.4010 shifts the focus to 1.4160, while a break below 1.4060 targets 1.4020.

The medium-term technicals are bullish. USDCAD is locked in a 1.3960-1.4160 range with an underlying uptrend line that comes into play at 1.4000.

For today, USDCAD support is at 1.4060 and 1.4020. Resistance is at 1.4110 and 1.4150.

Today’s Range: 1.4060-1.4140

Home for the Holidays

In America, the traffic is heavier than usual, train stations are busier, and airports are more crowded as the travel to celebrate Thanksgiving. CBS News reports that about 82 million Americans are traveling and 90% will be on the road. Sammy Hagar complained he couldn’t drive 55. This week he would be hoping to hit 25.

And if all those people are traveling, they aren’t trading. FX liquidity is poor and that leads to exaggerated price action which will be on full display with the release of today’s US data. Furthermore, the quality of the economic reports is sketchy and the results should be taken with a large degree of scepticism.

Taking Stock

Asian equity markets rallied on improved risk sentiment. Japan’s Topix rose 1.96%, Australia’s ASX 200 gained 0.81%, and Hong Kong’s Hang Seng rose 0.13%.

As of 7:00 am, the FTSE 100 index has gained 0.25%, the French CAC-40 is up 0.44%, and the German DAX has gained 0.30%. S&P 500 futures are up 0.34%, the US Dollar Index (DXY) is 99.76, the US 10-year Treasury yield is 3.998%, and gold (XAUUSD) is $4170.55.

EURUSD

EURUSD traded in a 1.1563-1.1596 range supported by US dollar weakness after yesterday’s soft US data. Prices are also seeing some benefit from talk that Ukraine may be forced to accept Putin’s Ukraine peace plan which was put forward by the Americans. Reuters reported that the US peace plan was drawn up using a Russian document given to the Trump administration in October.

GBPUSD

GBPUSD consolidated yesterday’s gains in a 1.3158-1.3198 range then sank and soared in a 1.3125-1.3225 range as Chancellor Rachel Reeves delivered her highly anticipated budget. The UK Office of Budget Responsibility (OBR) published (then yanked-) their latest economic and fiscal outlook, apologizing for releasing it too early. Unfortunately for the OBR, the data is out; (from Reuters)

- UK OBR ECONOMIC AND FISCAL OUTLOOK: BUDGET TAX RISES RAISE 26.1 BLN STG BY 2029-30

- UK OBR: CENTRAL GOVERNMENT NET CASH REQUIREMENT EX NETWORK RAIL 149.2 BLN STG 2025-26

- UK OBR: CUTS MEDIUM-TERM PRODUCTIVITY GROWTH FORECAST TO 1.0 PCT FROM 1.3 PCT

- UK OBR: FREEZING PERSONAL TAX THRESHOLDS RAISES 8.0 BLN STG IN 2029-30

- UK OBR: NICS ON SALARY-SACRIFICE PENSIONS RAISES 4.7 BLN STG IN 2029-30

USDJPY

USDJPY is at the top of its 155.65-156.51 range with selling pressure from speculation about a December rate hike losing out to the latest fiscal stimulus package. Reuters reported that the BoJ Governor has tweaked communications recently which suggests rates are going higher in December. Japanese Prime Minister Takaichi claimed that her stimulus package was not reckless spending but strengthened the economy.

AUDUSD

AUDUSD rallied from 0.6465 to 0.6512 due to broad US dollar weakness and higher-than-expected inflation numbers. October CPI rose 3.8% y/y (forecast 3.6%) while Core CPI rose 3.3% from 3.2%. The results were the fourth consecutive rise for inflation and dampened hopes for one further RBA rate cut next year. Some analysts even mused that the next move could be a rate hike.

NZDUSD

NZDUSD soared from 0.5616 to 0.5697 following the Reserve Bank of New Zealand (RBNZ) rate decision. Policymakers did the expected and cut the benchmark rate by 25 bps to 2.5% and indicated that further easing was unlikely.

USDMXN

USDMXN is consolidating yesterday’s losses in an 18.3576-18.4115 range after soft US data boosted odds that the Fed would cut US rates by 25 bps on December 10. The statement was cautious, noting that the risks were balanced.

China

PBoC Fix: 7.0796 vs exp. 7.0825 (Prev. 7.0826)

Shanghai Shenzhen CSI 300 rose 0.61% to 4517.63.

The yuan was fixed at its highest level in over a year and it may go higher if the Fed cuts rates in December.

Taiwan announces $40 billion defence budget.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics