March 6, 2026

USDCAD open: 1.3661, overnight range 1.3628-1.3679, close 1.3675

The first week of March 2026 is heading into the dust bins of history. It has been a rather eventful period beginning with Trump’s attack on Iran and an effective closure of the Strait of Hormuz, knocking off around 20 million barrels per day of crude supply. The conflict is threatening to suck surrounding nations into the battle. Trump is calling for the Kurds, a stateless group residing around the borders of Iran, Iraq, Syria and Turkey, to join the fight against Iran. Not to be outdone, Israel is attacking Lebanon in addition to Iran.

WTI soared 6.65% overnight, rising from 78.26 to 87.64 where it sits in NY today. The latest spike occurred after the WSJ reported Kuwait cut its oil production because it was running out of storage. The severe disruption of crude shipments from UAE, Saudi Arabia, etc. raised fears of an oil shortage and WTI has soared by 32.21% this week.

For a large swathe of the globe, the Middle East war is viewed through an economic lens: “How will it impact my portfolio? Can I make money from the turmoil?”

The Canadian dollar had a rather choppy week, rising and falling in a 1.3616–1.3754 range but opened in NY today where it opened on Monday.

Today’s US data includes NFP and Retail Sales.

USDCAD Technical Outlook

The intraday USDCAD technicals are neutral inside a 1.3620-1.3730 range with USDCAD currently trading in the middle of the band. A break above 1.3730 targets 1.3770 whiel a downside break puts 1.3580 in play.

The medium-term technicals are bearish with a descending triangle guiding prices lower while they are below the 1.3770-80 area and targeting a test and break of support in the 1.3480 zone. A break above 1.3780 negates the down trend and targets 1.4000.

For today, USDCAD support is at 1.3630 and 1.3580. Resistance is at 1.3690 and 1.3720.

Today’s Range: 1.3630-1.3720.

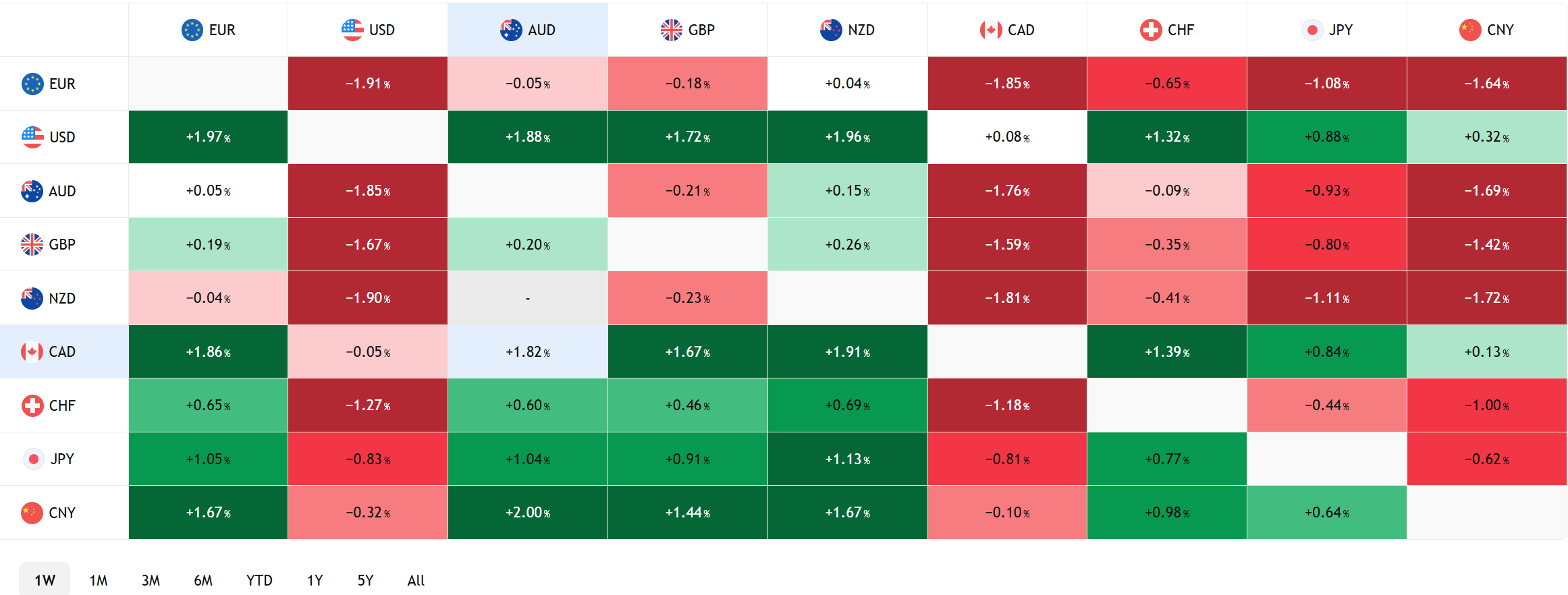

FX Heat Map (6:00 am) one week

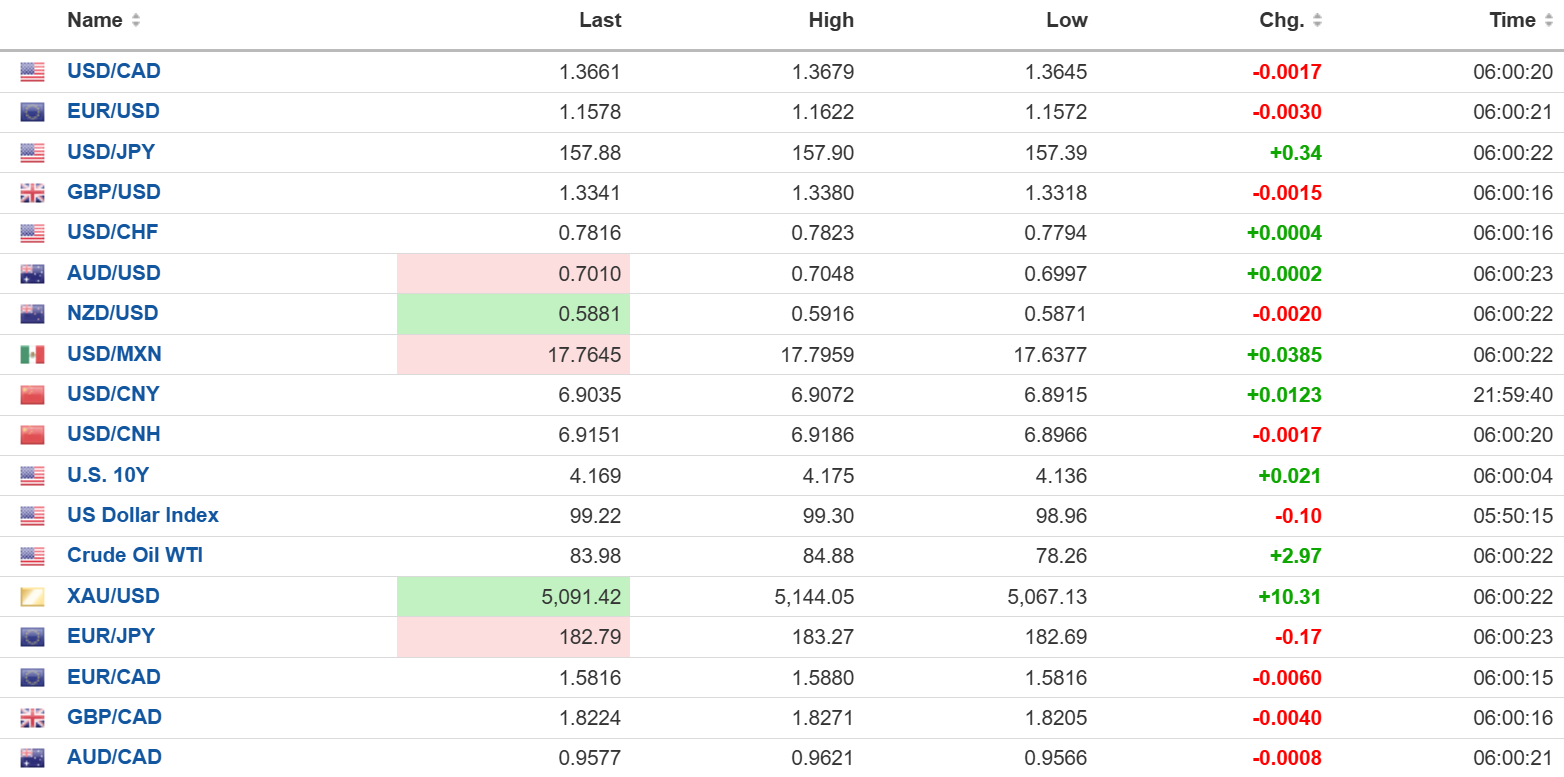

FX open high low 6:00 am

NFP Surprises to the Downside

The US jobs market was beaten with the ugly stick and todays nonfarm payrolls numbers just tossed a monkey wrench into the FOMC decision. Weak jobs suggest the need for a rate cut while soaring oil prices are inflationary and they may worsen an already sticky inflation outlook.

NFP plunged 92,000 in February, and the January numbers were revised down to 126,000 from 130,000 and the unemployment rate rose from 4.3% to 4.4%. The data may have been impacted by weather. Regardless how the numbers get spun, the report is weak.

Retail Sales Control Group (excludes receipts from auto dealers, building-materials retailers, gas stations, office supply stores, mobile home dealers and tobacco stores) rose 0.3% compared to 0% in December.

Overnight Round-up

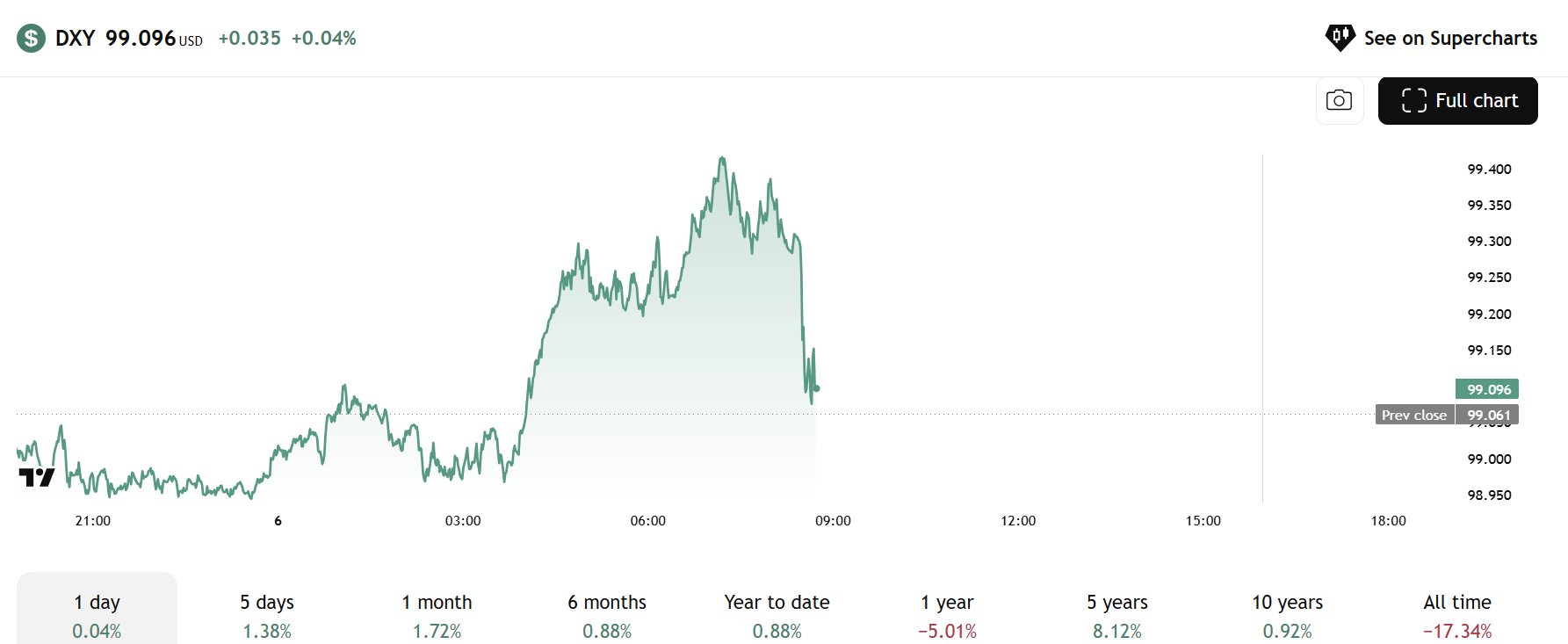

The US dollar index is up 0.20% at 99.23 after trading in a 98.96-99.32 range overnight. The DXY has gained 1.57% this week.

Richmond Fed President Thomas Barkin justified the case to leave interest rates unchanged. He said about last year’s easing, “the sense that the risks of the labour market were up while the risks to inflation were down. The data that’s come in over the last couple months suggests it has moved in the other direction. With the PCE numbers that we’re expecting next week, you’ve got a couple months of relatively high inflation. That certainly puts pause to any conclusion that we’re done fighting this.”

Taking Stock

Asian equity markets closed higher but lost ground on the week. Japan’s Topix rose 0.39% to finish the week down 4.17%. Hong Kong’s Hang Seng climbed 1.72% but is down 2.61% this week. Australia’s ASX 200 was the exception. It lost 1.00% overnight and is down 3.53% for the week.

As of 5:30 am PT, European bourses are under water. The German DAX is down 0.76% and 6.37% for the week. The French CAC 40 has lost 0.87% today and 7.36% this week. The UK FTSE 100 has dropped 0.71% today and 4.67% this week and S&P 500 futures are down 0.97%. The 10-year Treasury yield are 4.148% and gold (XAUUSD) is 5,109.75

EURUSD

EURUSD chopped around in a 1.1566–1.1622 range and is at the bottom of the band in early NY, losing 0.32% overnight and 1.90% this week. Eurozone Q4 GDP disappointed, rising 0.2% compared to the forecast for a 0.3% gain, while Q4 GDP y/y rose 1.2% compared to the previous reading of 1.4%.

GBPUSD

GBPUSD dipsy-doodled in a 1.3318–1.3380 band and is near the session low in NY. It was a choppy trading week for sterling as it bounced in a 1.3253–1.3403 range with price action being dictated by US dollar sentiment.

USDJPY

USDJPY traded quietly in a 157.39–157.99 range with prices underpinned by higher US Treasury yields and oil prices.

AUDUSD

AUDUSD churned in a 0.6990–0.7048 range and is at its session low ahead of today’s US nonfarm payrolls data.

USDMXN

USDMXN is bid, rising from 17.6377 to 17.8439 ahead of todays US jobs report. The ongoing war in Iran and fears that it could suck other Gulf nations into its vortex are fueling US dollar safe-have demand and the peso is suffering from that.

China

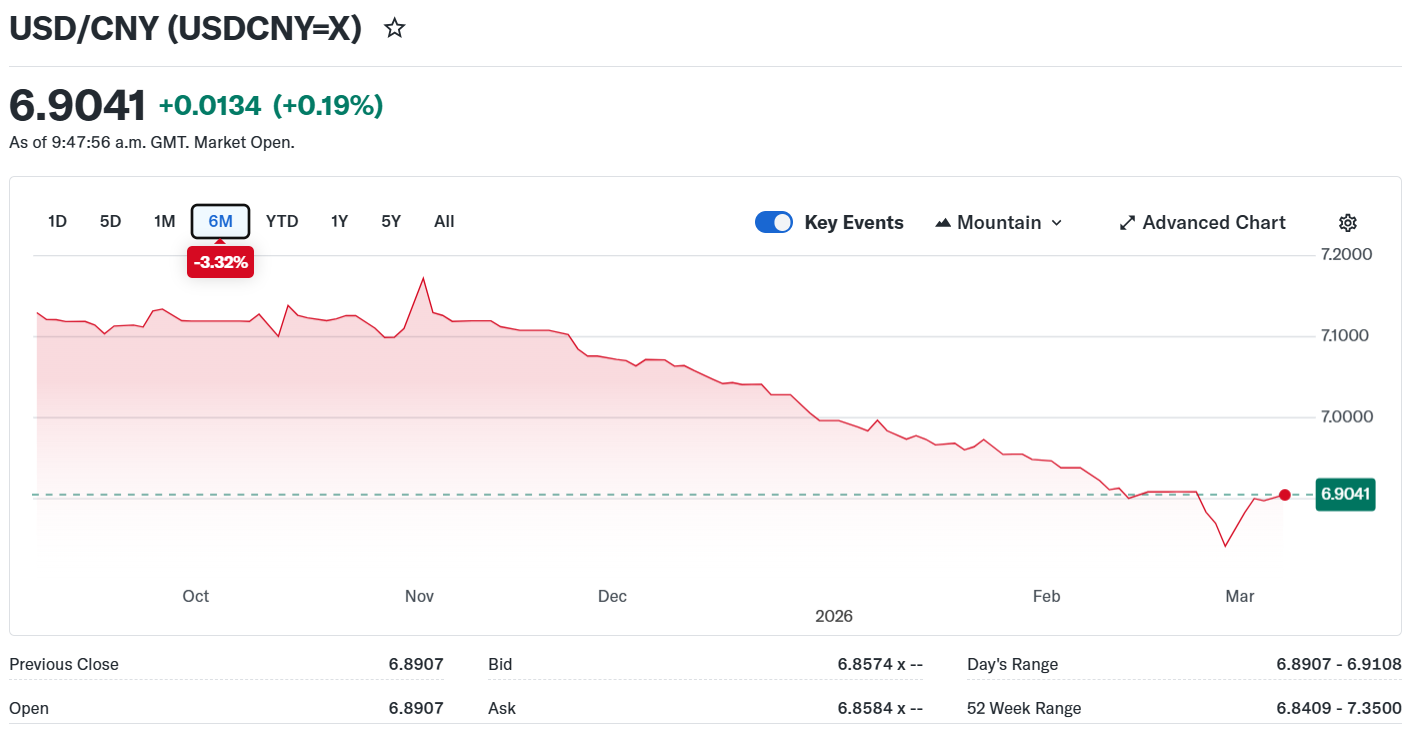

USDCNY Fix: 6.9025 vs exp. 6.8998 (Prev. 6.9007

Shanghai Shenzhen CSI 300 rose 0.27% to 4,660.44

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview