Source: Wikimedia commons

By Michael O’Neill

The Federal Open Market Committee’s dot-plot projections for US interest rates maybe wrong. That shouldn’t be a surprise. The FOMC has been wrong, often.

Do you remember when Fed Chair Jerome Powell started proclaiming inflation as transitory in March 2021? He finally ditched the term in November 2021 after prices soared and a cacophony of academic and private sector economists said rates were too low.

Even so, at the December 15, 2021, the FOMC did not act like they thought inflation was a big a deal. They projected PCE inflation would rise to just 2.6% in 2022, then drop to 2.3% in 2023. Another bad guess.

When they realized their inflation view was erroneous, on March 17, 2022, they only hiked rates by a 25 bps. They got braver the following month with a 50 bps hike, but it took a CPI print of 8.6% y/y in May, to force the Fed’s hand, which led to 350 bps more in rate increases by December 14.

Now the FOMC are rate hawks. Fed funds are at 4.25-4.50%, their highest level in 15 years, with more hikes penciled in for 2023. The dot-plot interest rate projections suggested a terminal (or peak rate) of 5.1% and no rate cuts in 2023.

Bond traders think the Fed has got it wrong.

The US 10-year Treasury yield dropped from 4.21% November 7, to 3.39% on January 18, after weak Producer Price Index data and a mild inflation report. CPI fell 0.6% to 6.5%y/y leading many economists to scale back their inflation forecasts.

The lower yields are also supported by the January 6 nonfarm payrolls report which showed US job growth slowing and wages ticking lower. The service sector, which had been a barometer for the resilient economy dropped from 56.5 in November to 49.6 in December.

There is a lot riding on the inflation outlook. But what if it is wrong.

Former Fed Vice Chair (1994-1996) Alan Binder thinks it is.

Mr Binder suggests that the pandemic, the war in Ukraine, and supply-chain disruptions created an inflation anomaly He has a point.

At the beginning of January he wrote an op-ed for the Wall Street Journal where he noted that inflation in the second half of 2022, was not only vastly lower than the first half, but it is very close to the Fed’s 2.0% target.

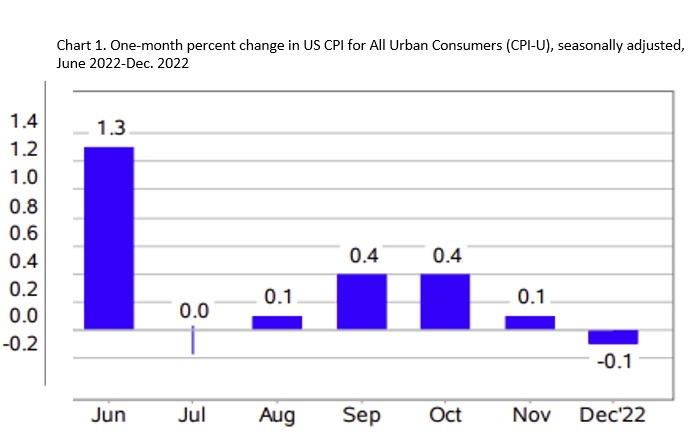

He’s right. If you add the month over month percent change from June to December 2022, CPI is 2.2% for the period.

Source: Bureau of Labor Statistics

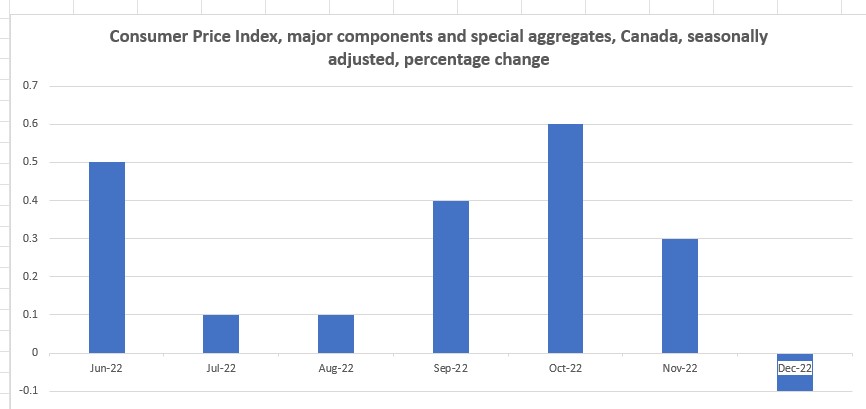

The Bank of Canada is in the same boat. Canada’s inflation rate since June 2022 is a mere 1.9%, which is bang in the middle of the BoC’s 1-3% inflation target.

Source: Statistics Canada/IFXA

However, the devil is in the details.

Mr Blinder pointed out that it is too soon to declare victory. He noted that US Core inflation, which excludes food and energy has run higher.

It’s the same in Canada where the BoC’s core-CPI metrics (Trim and Median) are 5.3% and 5.0% respectively.

The lower Canadian inflation numbers for December were because of a 13.1% drop in gasoline prices. West Texas Intermediate (WTI) bottomed out at $70.20/barrel on December 12. Prices have risen 18% since then, which doesn’t bode well for a lower core -inflation reading for January.

The BoC monetary policy statement on December 7 said, “The longer that consumers and businesses expect inflation to be above the target, the greater the risk that elevated inflation becomes entrenched.”

The BoC’s Q4 Business Outlook Survey shows inflation is a major concern for businesses and consumers. The survey showed 84% of businesses expect CPI will average above 3% over the next two years. Consumers are even more sceptical. They think inflation will be 7.2% for 1 year and 5.1% for two years.

It appears that the fears of inflation being entrenched have been realized.

USDCAD is not reacting to Canadian data. Traders quickly erased the post-employment report sell-off and the reaction to the lower-than-expected Canadian CPI report was so fleeting, that if you blinked, you would miss it.

A 25 bp BoC rate hike next week, will likely have a similar impact as it is the consensus view.

However, if the BoC decides to pause, it will cause an adverse reaction.

Leaving rates unchanged is a real possibility after Senior Deputy Governor Sharon Kozicki suggested that the impact of previous rate hikes and its effects are working their way through the economy. “In other words, we are moving from how much to raise interest rates to whether to raise interest rates.”

Such an outcome would send USDCAD to 1.3800 as traders tell the BoC, “What we’ve got here is failure to communicate.”