By Michael O’Neill

It had to happen. And it did. On February 5, the Dow Jones Industrial Average (DJIA) suffered the largest intraday drop in history, falling nearly 1,600 points and on the heels of a 665 point drop the previous Friday. It was a collapse of Olympic proportions. Nasty, for sure. Unexpected; not at all.

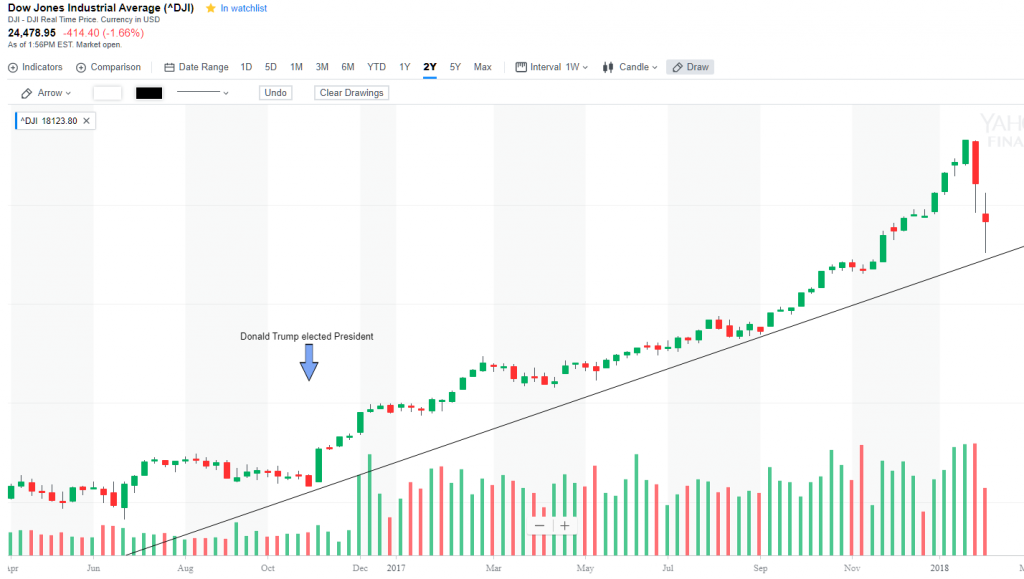

The DJIA soared 45.8% from President Trump’s election on November 7, 2016, to January 26, 2018, without a meaningful correction. In January, daily gains accelerated like a nitrous-fueled funny car. It took a mere 13 days, from January 4 to January 18, to go from 25,000 to blasting above 26,000.

Even at that lofty level, pundits were predicting further gains. Rising global growth forecasts, US tax cuts, low unemployment and the belief US interest rate hikes would be gradual had visions of 30,000 dancing in their heads.

Alas, it was not to be. The February 2, US employment data reported a sharp jump in average hourly earnings in January, to 2.9% from 2.5% in December. Low readings of this metric were cited by Former Fed Chair Janet Yellen and her colleagues for preventing interest rates from rising. They weren’t low anymore, and that sent Treasury yields soaring. Rapidly rising interest rates are anathema to equities.

The high flying DJIA was shot down in flames, erasing all the gains since the beginning of December.

Chart: DIJA 1 year

Source: YahooFinance

Prices are struggling to rebound from Monday’s carnage, and the blood-letting hasn’t stopped. Equity traders, fund managers, etc. have ridden the “Trump rally” for a little over 14 months. They will be eager to protect those gains by selling into rallies, suggesting fresh gains may be hard to sustain. It is not a stretch to suggest that we have seen the high for the next few months.

The Olympic torch that was lit in Olympia Greece on October 24 will soon put fire to the cauldron in Pyeongchang, South Korea, heralding the start of the 2018 Winter Olympics.

Us Treasury Secretary Steven Mnuchin didn’t have a torch when he lit a fire of another kind, two weeks ago, in Davos, Switzerland. That’s where he proclaimed “a weaker dollar is good for the US.”

Immediately afterwards, headlines screamed, “US abandons strong dollar policy.” EURUSD roared higher, rising from 1.2300 to 1.2535. Sterling climbed from 1.3920 to 1.4340. USDCAD wasn’t bothered very much and only rose from 1.2280 to 1.2385. President Trump and later, Mr Mnuchin denied that the US had changed its currency policy and the US dollar began reversing gains.

Those soothing words may have appeased FX traders, but they did not have the same effect on European Central Bank council member Ewald Nowotny. Mr Nowotny in an interview with an Austrian magazine on February 1, was asked if President Trump’s tweets were a danger or uncertainty factor for international markets. He responded by saying “the US Treasury purposely pushes down the dollar and wants to keep it low.”

FX markets responded by buying US dollars which were already in demand due to rising US Treasury yields and risk aversion concerns.

US dollar gains this week need some perspective. The dollar has gotten stronger, but the current levels are well above where it was at the start of the year. The only exceptions are the Australian and Canadian dollars which are down modestly. The risk of further US dollar strength cannot be ruled out, especially if global equity indices continue to be unstable.

The equity market wobble wiped out all the gains for the UK’s FTSE 100 for 2018, but it didn’t seem to faze Bank of England Governor Mark Carney. At his press conference on February 8, after the BoE left rates unchanged, the governor said “it is certainly healthier when markets have two-way risk. You can have a trend, but a trend with two-way risk.”

The Bank of England left the door wide open to a May rate increase because of high inflation and stronger global growth than previously forecast.

The global equity market correction is a bit of a blessing for the Bank of Canada. The BoC justified the January 17 increase in the overnight rate to 1.5%, saying “inflation is close to target and the economy is operating roughly at capacity.” They admitted concern about the future of the North American Free Trade Agreement clouded their outlook.

The market focus shifted to the US dollar. It was falling steadily and lifted the Loonie in the process. On February 2, USDCAD appeared poised to shatter support at 1.2250 and sink to 1.1920. If it had happened, the move would have limited the BoC’s ability to raise rates to combat inflation.

They were saved by the US employment report and the rise in hourly wages. USDCAD soared, rising from 1.2250 to 1.2613 by February 8. One man’s blessing is another man’s curse, and in this case, free-falling equity markets led to a lot of cursing

Global equity markets have yet to stabilize, and that means the Olympic Cauldron isn’t the only thing getting torched.