Forecasting is a “crap-shoot” at the best of times, and no one knows that better than the Bank of Canada. They keep rolling the forecast dice and coming up “snake eyes.” Their GDP forecasts are proof. They trimmed their 2019 GDP prediction from 2.1% to 2.0% in October and then lowered it again, to 1.7%, in January.

The third time is a charm, right? Not if you are either the Toronto Maple Leafs playing a game seven against Boston Bruins or Bank of Canada economists. Both groups rolled “snake eyes.”

The Bank of Canada cut its 2019 GDP forecast again. The April Monetary Policy Report slashed growth estimates to 1.2% from 1.7%. It is becoming a quarterly ritual, making their forecasting ability look somewhat suspect. The BoC lists 319 economists spanning 32 pages of their website which is a lot of brain power. If they can’t get it right, Corporate Canada’s ability to make informed, investment decisions and long-term plans, are seriously degraded.

A cynic might believe that the BoC’s latest cut to its GDP growth forecast is so deep because it is an effort to avoid being wrong in July and having to downgrade growth further. The cynics might be right.

The BoC did what was almost universally expected and left interest rates unchanged, at the April 24 policy meeting. However, the statement was considered more dovish than expected. They dropped the reference to “the timing of future rate increases” and the “neutral rate,” and proclaimed a need for an “accommodative” policy.

The MPR statement went further. In January the first three paragraphs of the “Canadian Economy” section bragged how the Canadian economy was operating close to capacity and had been for over a year. They pointed out that job growth was strong but still downgraded their growth outlook. They blamed the changes on developments in the oil markets, predicting a “temporary” slowdown in Q1. Temporary needs to be defined.

The April MPR explained the lower growth outlook by noting highlighted trade tensions and “elevated uncertainty.” Really? They just became concerns, in April? Those two factors were issues last September when President Trump slapped tariffs on Chinese imports into the US. “Elevated uncertainty” isn’t even quantifiable; it is merely a throw-away phrase meaning “I don’t know.”

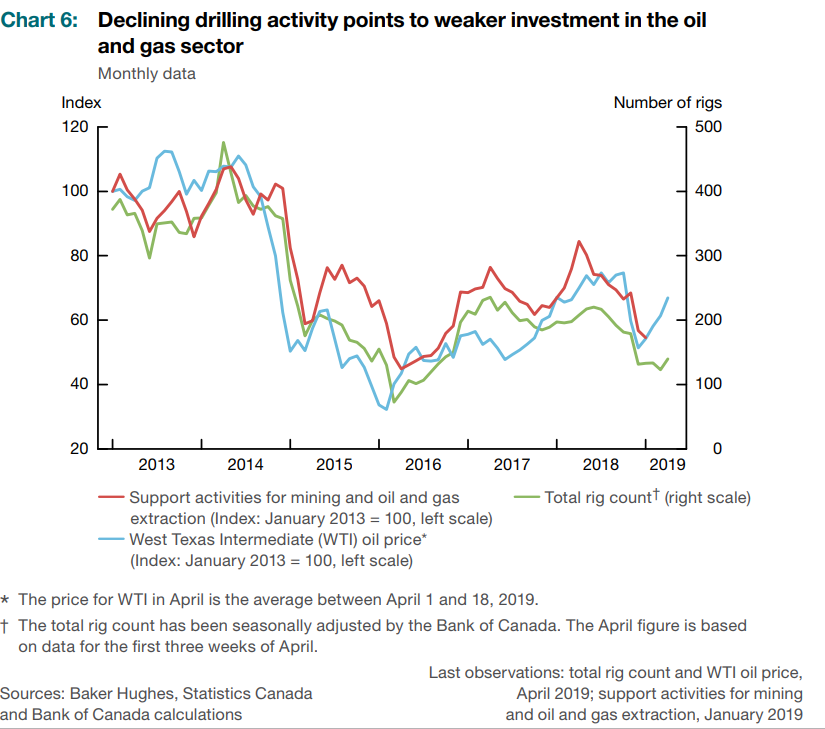

Governor Poloz noted four Canadian specific considerations for the dovish outlook; oil, trade, housing, and fiscal. He said Canada’s oil sector remains under considerable stress as “limited access to markets remains a significant source of drag and uncertainty” due to western producers causing a downward revision in investment intentions. He justifies the view by noting that the sector is still adjusting to global oil prices in the $50.00-$60.00/barrel range rather than the much higher prices of five years ago

Source: Bank of Canada MPR

Mr Poloz’s oil price comments are accurate depending on your time frame. Sure, oil prices were much higher five years ago, but they were a whole lot lower for the 20 years between 1988 and 2008 when the average price for that period was $34.06/barrel.

Alberta may be suffering a shortage of pipeline capacity, but rail delivery is picking up the slack. CP and CN rail companies reported a surge in profits from oil tanker loads. Oil is still getting to markets but perhaps not as efficiently as it could. Furthermore, the Western Canada Select discount to West Texas Intermediate has shrunk to $11.35/barrel from as high as $39.00/b last November. Canadian producers are receiving CAD 74.25/barrel for their oil after accounting for the discount and using an exchange rate of 1.3500. Not too shabby.

Mr Poloz cited uncertainty about future trade as another reason for the current slowdown. He is worried about the delay in the ratification of CUSMA (Canada US Mexico Agreement on trade). The BoC anticipated the trade deal would boost investment, but it hasn’t happened. He said the decline in exports might be related and incorporated the weak numbers into their forecasts, even though they could be tainted by severe weather. It almost sounds like the BoC are finding “facts” to fit their argument.

Housing prices are another concern. They are monitoring developments in the housing market very closely in order to understand how the effects of local tax changes, changes in mortgage guidelines and past rises in interest rates would play out. Arguably, the BoC statement suggesting an accommodative monetary policy “continues to be warranted” is a deliberate measure to alleviate mortgage default concerns.

The Governor didn’t seem pleased about the Province of Ontario’s efforts to curtail years of massive deficit spending noting that the smaller budget would knock 0.2% off of the BoC’s 2020 GDP growth outlook.

The Bank of Canada may be unsure of the domestic economic growth outlook, but USDCAD traders have a pretty good idea about the currency direction, and that direction is higher.

The April 24 interest rate statement and Monetary Policy report knocked the Canadian dollar for a loop and set the stage for additional losses. USDCAD traders turned bullish with the break above significant resistance at 1.3460 which had capped upside moves since January. They have set their sights on 1.3660 and then expect further gains to 1.4080 (CAD 72.00 cents)

The Bank of Canada may have rolled snake eyes with its forecasts, but it is the companies who hedged exposures by selling USDCAD at the beginning of the month who “crapped out.”