By Michael O’Neill

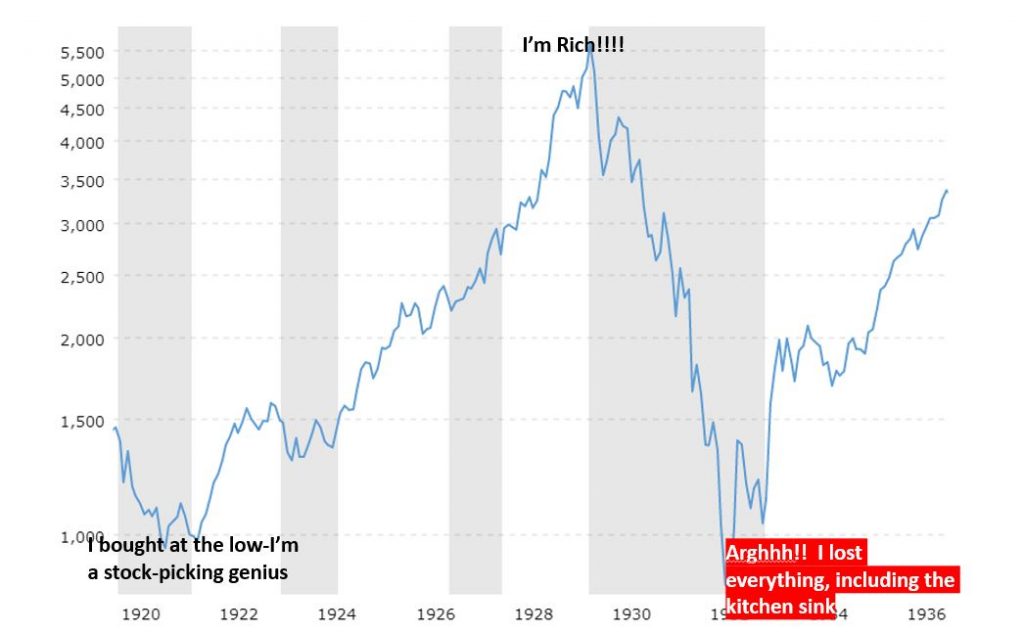

It’s the start of a brave new decade. This century’s teen years has rolled over to what some hope to be the 21’st century’s version of the “roaring twenties.” They should be careful of what they wish for, especially if they are looking for stock market gains. The Dow Jones Industrial Average lost 31.3% in 1920. A similar performance in 2020 would knock the index down from 28,745 to 19,748. Even worse, a decade’s worth of gains between 1920 and 1930 were totally wiped out by mid-1932.

Chart: DJIA Performance 1920-1936

Source: Macrotrends

Many people believe a repeat of that performance is unlikely. Perhaps caution is warranted. They may be underestimating potential chaos from leaders like thin-skinned Trump, imperialistic Xi Jinping, well-armed Vladimir Putin, financially naive Justin Trudeau, and looney-tunes Kim Jong-un.

The 2020’s are barely two weeks old, and the top song should be a Barry McGuire/ Plastic Ono Band medley. Barry is singing “the Middle Eastern world is exploding, violence flaring, missiles loadin,” while John and Yoko harmonize “give peace a chance.”

The song was inspired by the high-stakes geopolitical poker game between Iran and the US. The Americans anted with a drone strike that killed Iran Revolution Guard General Qasem Soleimani. Iran raised with a missile barrage on US-occupied bases in Iraq but didn’t kill anyone. Whip-saw price action roiled Japanese yen, Swiss franc, oil, and gold markets as headlines scrolled across screens. The furor died down as quickly as it started when both sides appeared to walk away from the table. Wall Street responded by taking stock markets to record highs on January 9.

There is an undercurrent of positive risk sentiment. It stems from the global low-interest rate environment and a major thaw in the previously frozen US/China trade negotiations. The Fed indicated that interest rates would be on hold for 2020, at their December meeting and Vice Chair Richard Clarida echoed that sentiment this week. Thursday, he said that monetary policy is in a “good place,” which is the same description that Fed Chair Jerome Powell has been using, since October.

China’s chief trade negotiator Vice Premier Liu He will arrive in Washington next Thursday, to sign the Phase 1 trade deal. President Trump said that he might wait until after the 2020 elections to complete Phase 2, on January 9. He said, “I think I might want to wait to finish ’til after the election, because by doing that, I think we can actually make a little bit better deal, maybe a lot better deal.” Will he delay Eurozone and French trade talks? I don’t think so.

Equity traders are heartily cheering the news of the Phase 1 deal. Bank of Canada Governor Stephen Poloz is less enthusiastic. He is sceptically shaking his pom-poms, noting that “plenty of uncertainty remains around the implications of the US-China agreement for Canadian exports and around whether any more of the new tariffs can be rolled back.” He acknowledged some improvement on the business investment prospects with the pending ratification of the Canada US Mexico Agreement.

The Bank of Canada left interest rates unchanged, December 4. Since then, a string of soft data offset firm inflation readings of 2.0% which suggests domestic rates will remain unchanged at 1.75% until the summer.

USDCAD has dropped steadily after failing to break above resistance at 1.3330 in mid-November and then dropping below 1.3100 on Boxing Day and hitting 1.2960 January 2. Some analysts believed that the break below 1.3000 was significant and suggested it was the start of a new downtrend. Others blame the price action on seasonal factors.

The “fog of war” and the “haze of year-end” are a similar phenomena. They both mask the truth. Invading a sovereign country to locate weapons of mass destruction is an example of the fog of war. The haze of year-end is when someone ascribes USDCAD price movements to anything other than supply/demand imbalances in extremely illiquid, December holiday markets.

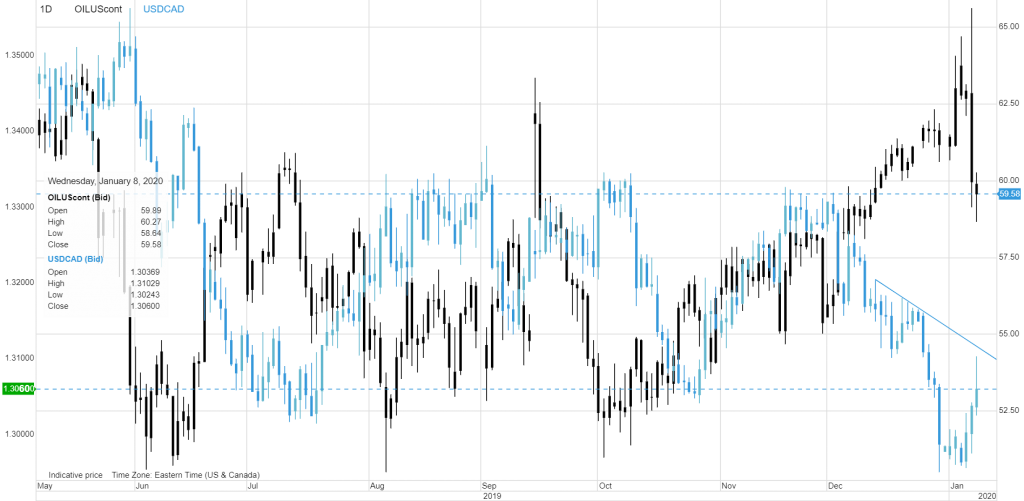

Oil traders were side-swiped by the brief US/Iran hostilities which sent West Texas Intermediate (WTI) skyrocketing to $65.70/barrel on January 7 and then down to $58.69 on January 9. The sharp retreat from the peak is telling. It says traders are more concerned about the risk of rising crude supply in a slowing global environment than they are with the risk of supply disruptions if Iran were to close the Strait of Hormuz. American’s are less concerned than most as the US is not only self-sufficient in crude production, it is an exporter.

The Canadian dollar reacted to the steep up and down oil price action. However, the correlation isn’t as robust as in the past. Alberta’s Western Canada Select Crude trades at a $22.51/b discount to WTI and producers are still struggling with pipeline constraints. Also, Canadian oil is the “Ebola” of the energy industry. A National Geographic article last April claimed the oilsands were the world’s most destructive oil operation, citing tailings leakage contaminating water supplies and the creation of acid rain. Saudi Arabia, which bred, al-Qaeda, is the preferred crude source despite the massive carbon footprint from over 12,000 oil tankers plying the oceans each year. The disdain for Canadian oil is another drag on Canadian dollar gains when oil prices rise.

Chart: OilUS continuous and USDCAD daily

Canadian economic growth lags that of the US. Canadian and US overnight rates are identical at 1.75%. Simplistically, in weaker growth/same rate environment, it is better to buy greenbacks rather than Canadian dollars. Adding the new US/China trade agreement to the equation combined with a deteriorating Canada/China relationship, makes the US dollar even more attractive. Finally, USDCAD has been grinding higher since 2012 and will continue to do so while prices are above the 1.2920-50 zone.

It is a brave new decade and Canadians may need to be brave to face the challenges ahead.