Photo: Pixabay/IFXA

By Michael O’Neill

Central Bankers around the world have similar mandates and similar problems. They use inflation targeting to dictate monetary policy actions. They are charged with maintaining price stability by keeping inflation low and stable.

It was a sound strategy when inflation was high, but in a low inflation environment, not so much. In July, European Union inflation was -0.4%, the United Kingdom posted a 0.4% result, US inflation was 0.6%, and Canada inflation was 0% m/m.

Judging by those numbers, the bankers have nailed their mandates. If they worked in the private sector, they would be cueing with hands out awaiting a huge performance bonus cheque.

Instead, their hands are getting slapped. That’s because the inflation numbers are too low.

G-10 central banks are mandated to maintain inflation around the 2% level. Economic theory posits that if inflation is below 2.0%, it means the economy is slowing, and job losses may increase. Low inflation also restricts a central bank’s ability to manage a crisis and is exacerbated in this negative-to near-zero interest rate environment.

The problem isn’t new. Central bankers have struggled to cope with soft data for years, without much success.

Perhaps it’s time to throw the baby out with the bath water.

“Time to start again” Picture Pixabay/IFXA

That’s what Fed Chair Jerome Powell may be doing. On August 27 at the Jackson Hole Symposium, he is expected to unveil a brand-new inflation strategy. His speech, titled, “Navigating the Decade Ahead: Implications for Monetary Policy,” maybe the blueprint for his G-10 peers.

He is expected to announce that the Fed is adopting an “average inflation rate” measure and ditching the existing 2.0% inflation target. The strategy allows the Fed to focus on growth and full employment. It also means inflation could rise well above 2.0% while keeping interest rates ultra-low, or even into negative territory.

Mr Powell’s speech may spur similar action by other central banks. The G-7 has a history of cooperation in coordinated FX intervention, so coordinated inflation manipulation is not out of the question.

It may have already started.

The European Central Bank (ECB) is undergoing a monetary strategy review which is to be completed at the end of the year.

One of the reasons for the review is to address how to manage a low inflation environment, which is different from the challenges inherent with high inflation.

The Bank of Canada seems to be on board. They are in the process of a five-year monetary policy review, and Inflation issues are at the top of the list. The BoC is conducting a survey called “Lets Talk Inflation.” Deputy Governors are making the rounds discussing how inflation is perceived and how the Bank can achieve their 2.0% inflation target.

The Bank of Canada has cited “temporary factors” as reasons for why Canada’s inflation numbers were below target for many years. Today they may be realizing that although some factors may have changed, the impact is far from temporary.

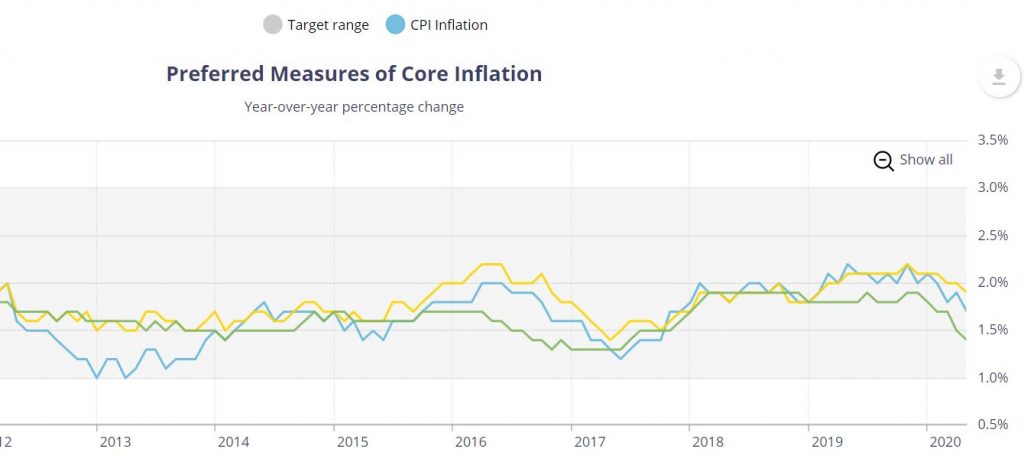

Source: Bank of Canada

In a speech to the Canadian Association for Business Economics, August 25, BoC Deputy Governor Lawrence Schembri claimed that the BoC “has the flexibility to see through temporary movements in inflation because of high “Public Confidence” in the Bank’s ability to manage monetary policy to achieve the inflation target.”

He goes to great pains to debunk the gap between consumer perception and reality. He noted that many consumers believe the Consumer Price Index (CPI) consumption basket is not representative of them.

He didn’t say “fake news” but did say the perception was erroneous. The BoC built a consumption basket and inflation rate and modeled it for different groupings of households, based on income, education, age, and renters versus owners. The results were very close to the official CPI rate.

On August 26, Senior Deputy Governor Carolyn Wilkins admitted that as part of the monetary policy review, the BoC was studying the use of average inflation targeting, price level targeting, and employment/inflation dual mandate and nominal GDP growth and level targeting.

The inflation survey, the speech about inflation, and then Ms Wilkins remarks about average inflation targeting and a dual inflation/employment mandate, certainly hint that the BoC will follow Mr Powell’s lead.

Central banks getting together to manipulate currency rates is nothing new, but a mass shift to average rate inflation targeting would be the first instance of Coordinated Inflation Manipulation.