By Michael O’Neill

The latest Federal Open Market Committee (FOMC) monetary policy decision may sound like an invitation to a freshman frat-house party, but instead of students, it’s interest rates that are set to rise and remain elevated for longer than previously expected.

The Fed lived up to its advanced billing and delivered a “hawkish pause.” This means they left interest rates unchanged while cautioning that rates may still climb before the year’s end. The statement also gets a hawkish label because it described economic activity as expanding at a solid pace compared to July when the economy was only expanding at a moderate pace.

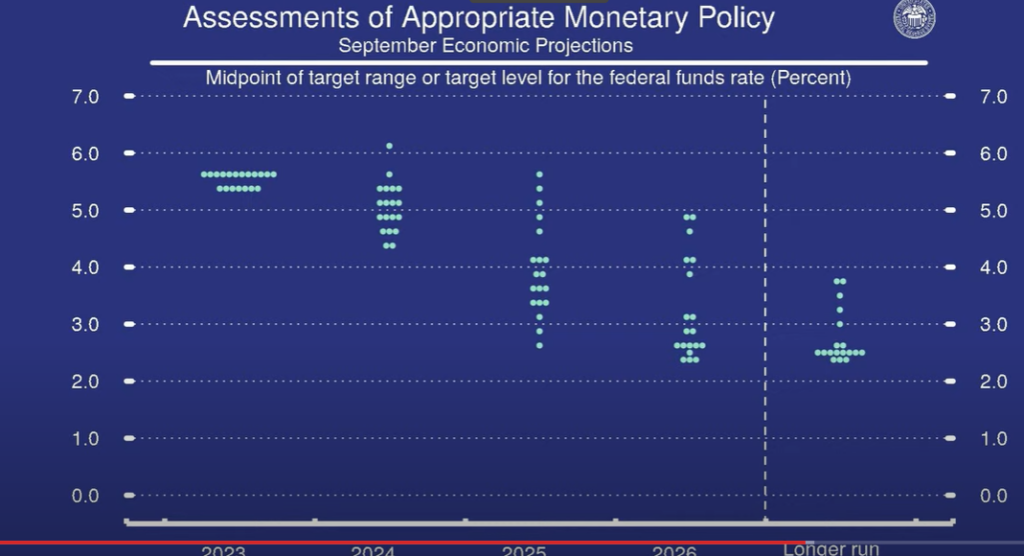

The Summary of Economic Projections supports the “hawkish” view. The July dots suggest that policymakers thought they were done hiking rates while September’s dots suggest that another 25 bp hike is likely before year end. Mr Powell said as much in response to a question in his press conference.

Source: FOMC

Policymakers are forecasting a lower unemployment rate (3.8% vs 4.1 in June), higher inflation (PCE 3.3% vs 3.2% in June) and stronger economic growth (2.1% vs 1.0% in June).

Mr Powell reiterated the above themes in his press conference opening statement. He emphasized that the current monetary policy stance is seen as restrictive and warned that the Fed is prepared to raise rates further if necessary. He included his usual caveat that “decisions will be based on incoming data and their implications for the economic outlook”.

“Who knew? The Fed and Led Zeppelin seem to have something in common – they both agree that ‘The Song Remains the Same.’

Meanwhile, the Bank of Canada has mastered a different Led Zeppelin tune– “Dazed and Confused.”

The BoC raised rates in lockstep with the Fed from March 2022 to January 2023. Then they left rates unchanged in March, despite acknowledging that inflation was “still too high”, “the labour market remains very tight” and that the decline in inflation was due to falling oil prices. The move was justified because “the latest data remains in line with the Bank’s expectations for CPI to drop to around 3.0% in the middle of the year.

By June, the rate hike pause playbook had been tossed out the window. Inflation was not falling as fast as expected, the economy was stronger than expected and goods and services were price inflation rose, despite lower energy costs. The BoC hike rates by 25 bps in June and again in July. The July statement noted a concern about sticky inflation while the Monetary Policy report upgraded GDP growth and pushed out there forecast for inflation to reach target to the middle of 2025.

In summary, inflation continues to be problematic and policymakers are confused. Prices are not coming down fast enough which should have led to another rate hike in September. It didn’t. The BoC left rates unchanged but warned they are “prepared to increase the policy interest rate further if needed.”

They might need to. Canadian inflation jumped to 4.0% y/y in August, compared to 3.3% in July, which is pretty solid evidence that the BoC’s expectations for inflation at 3.0% in the summer, were a few sandwiches shy of a picnic.

The BoC’s preferred inflation measures rose as well and averaged 4.0% Interestingly, the BoC used to feature three indicators: CPI Trim, CPI Median and CPI Common. No longer. CPI Common has been given the old heave-ho, which is a lot like a lousy carpenter blaming his or her tools.

Nevertheless, the inflation reading suggests that Canadian rates are going higher in October even though Deputy Governor Sharon Kozicki was dismissive of the results saying “ups and downs are not unusual which is why we look at core-CPI. Hello! Statistics Canada Core CPI rose to 3.3% as did the Bank’s measure.

The prospect of higher Canadian interest rates knocked USDCAD lower and the dropped chewed through strong support at 1.3440 and 1.3400. The technical picture turned bearish but only fleetingly. Attention has shifted to the Fed’s hawkish hold with a break above 1.3540 suggesting a short term low (1.3380) is in place. If so, USDCAD should consolidate in a 1.3400-1.3700 range until the October 20 BoC meeting.

The Fed’s hawkish stance and the BoC’s cautious approach remind us that the road ahead may be “higher for longer,” making it essential for market participants to stay vigilant and adaptable.