By Michael O’Neill

Happy Halloween. There are plenty of pint-sized, ghosts, and ghouls threatening tricks to coerce treats from homeowners this week. Even central bankers are into the act.

Bank of Canada Governor Stephen Poloz, costumed as a business one-percenter, handed out rocks, with veiled promises of treats in the future. Fed Chair Jerome Powell was more generous. He doled out the equivalent of full-size chocolate bars, but the candy was past its best-before-date.

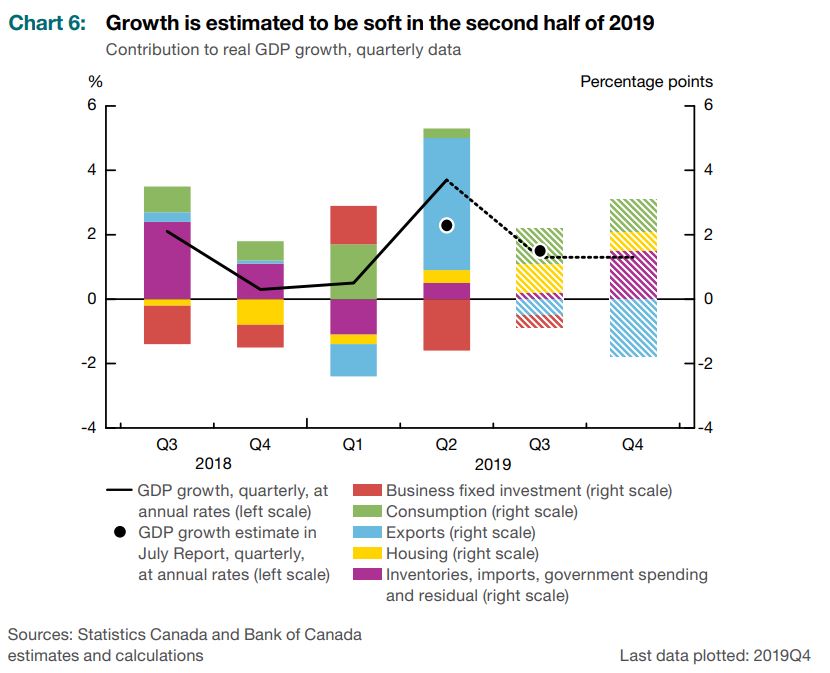

The Bank of Canada was first out of the policy gate. They left rates unchanged at 1.75% for the eighth meeting in a row, despite projecting that in the second half of the year, domestic growth will slow to a rate below its potential. They said the slow growth was due to “the uncertainty associated with trade conflicts, continuing adjustment in the energy sector, and the unwinding of temporary factors that boosted growth in the second quarter.”

FX markets were not surprised by the unchanged interest rate policy, but they were taken aback by the degree of dovishness inherent in the Monetary Policy Report (MPR). The BoC is concerned about weakness in foreign demand, escalating global trade conflicts, weak business investment, geopolitical tensions, and a soft energy sector. Traders paid special attention to the statement’s observation that the “Canadian dollar has strengthened against other currencies.” The Reserve Bank of Australia is known to intervene in its currency following similar comments although that is unlikely in the BoC’s case. As per the MPR, the biggest worry is trade tensions and the related uncertainty which are adding directly to the drag on investment and exports. The Bank estimates “that, together, the direct and indirect impacts would remove about 2 percent from the level of Canadian GDP by the end of 2021 in the absence of any policy actions.”

It isn’t all doom and gloom. The Bank predicts economic growth will gradually improve to potential, in 2020 and 2021. The increase will be driven by consumer spending, which is supported by low mortgage rates while oil capacity improves. Nevertheless, the BoC has a definite easing bias. Mr Poloz admitted as much during his press conference saying the Governing council discussed an “insurance” cut at the October 30 meeting.

The Canadian dollar took the news on the beak. USDCAD was just above its July 22 low of 1.3040, trading at 1.3080 when the BoC statement was released. The BoC’s dovish bias sparked a steep rally, exacerbated by a preponderance of bullish Canadian dollar positioning. USDCAD touched 1.3205 before drifting down to 1.3155 following the Federal Open Market Committee news.

The FOMC delivered the treats. The market universally predicted that US rates would fall by 0.25% at the October 30 meeting and they were correct. Analyst’s also thought the Fed would signal a pause in rate cuts. The Fed did that too.

The odds for a December rate cut faded to less than 20%, in part because of a minor tweak to the FOMC statement. The September 18 statement said the Committee would “contemplate the future path of the target range.” The October 30 statement drops “contemplate” and replaces it with monitor. Some analysts suggest the change is a hint that further rate reductions won’t be forthcoming. Mr Powell hinted the same thing during his press conference. He answered a question about what it would take for the Fed to raise rates, saying rates would go up if inflation goes up, but they “don’t see that happening.”

Wall Street stocks indices closed at record highs, Treasury yields dipped, and the US dollar sank.

Halloween spooked Brexit. The UK was supposed to leave the European Union (EU) on October 31, and if not, Prime Minister Boris Johnson promised to be “dead in a ditch.” Neither event happened although more than a few MP’s were seen with trenching tools. The EU extended the Brexit deadline to January 31, 2020, at the request of the British government and British MP’s granted Mr Johnson’s request for an election, slated for December 12. The lowered risk of a “no-deal Brexit,” and the events leading up to the election announcement lifted GBPUSD from 1.2200 on October 9 to 1.3005 on October 21. Prices have consolidated in a 1.2800-1.3000 range ever since.

The US dollar is closing out the month of October on a negative note. It lost ground against the major G-10 currencies except for the Japanese yen as safe-haven trades were unwound due to the improved tone to the US/China trade talks. The Fed and BoC rate decisions and the delay in Brexit also fueled US dollar selling.

Commodity bloc currencies rose on news that the US and China were nearing an agreement on what was termed Phase 1 of the seemingly never-ending US/China trade talks. The outlook improved to a degree so much that President Trump promised to delay the latest round of tariff increases. There were even rumours that he and Chinese President Xi Jinping would sign the agreement at the APEC meeting in Chile, on November 16-17. That is not going to happen, at least not in Chile according to the country’s President. He canceled the APEC gathering due to domestic protests.

There are other barriers to signing Phase 1. Trump’s many tweets about China’s plans of buying up to $50 billion in US Agricultural products are making Chinese officials uncomfortable. They are reportedly unwillingly to commit to buying products on that scale, fearing it would destabilize their domestic markets. In May, a US/China trade deal was reportedly ready to sign just before everything went pear-shaped. China is also balking at implementing long term structural changes and will insist on a repeal of all tariffs before the start of Phase 2 talks.

Linus never got any toys from the Great Pumpkin, but equity bulls and US dollar bears are getting gifts from the Great Bumpkins. No tricks, just treats.