By Michael O’Neill

“No need to raise a fuss and there’s no need to raise a holler. Cuz there ain’t no summertime blues for the Canadian dollar.”

A slate of better than expected Canadian economic reports has narrowed CAD/US interest rate differentials and fueled USDCAD selling. The Bank of Canada estimates it will produce growth close to “potential output” with increased exports. Under that scenario, the Loonie won’t be singing the Summertime Blues.

The monthly Survey of Manufacturing report released July 17 supported the BoC’s expectations for exports. Manufacturing sales rose 1.6% in May, representing 66.2% of Canadian manufacturing.

The Canadian dollar suffered a bit of a beating when the June inflation data was released. The data was expected to be soft due to energy price swings, and that is what occurred. The knee-jerk reaction was to sell Canadian dollars, but the sellers quickly became buyers. Statistics Canada said when energy prices were excluded, the Consumer Price Index (CPI) rose 2.6% year over year. More importantly, the data is slightly above the Bank of Canada’s inflation target.

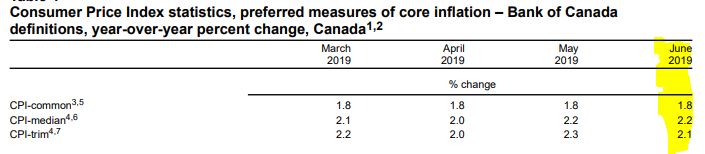

The Bank of Canada’s inflation strategy is at the core of its mandate “to conduct monetary policy to promote the economic and financial well-being of Canadians.” To achieve this objective the BoC monitors three measures of inflation: CPI trim, CPI median and CPI common. Trim excludes CPI components whose rate of change in a given month are volatile. Median corresponds to price change at the 50th percentile. (basket weight) Common uses a statistical procedure to track common price changes across the CPI basket.

The Canadian inflation report reduces the necessity for the BoC to lower domestic rates anytime soon. That is a big plus for USDCAD bears since among the major G-10 central Banks, (excluding the Brexit-challenged Bank of England) the BoC is the only one without a dovish bias or is actively easing.

Canadian employment growth continues to be robust. Statistics Canada noted that employment was up 421,000 or 2.3% year over year in June. The BoC Monetary Policy Report (MPR) described the domestic labour market as “healthy,” noting the unemployment rate is near an all-time low while participation of “prime-age” workers is near its historical high.

High employment, and rising inflation are typical triggers for rate increases which further suggests that the BoC would prefer to leave domestic interest rates at current levels. In the global rate cutting environment, that sentiment undermines USDCAD.

Oil prices have contributed to Canadian dollar strength as well. West Texas Intermediate prices climbed steadily in June, rising from $50.70/barrel to $60.80/b as tensions between Iran and the UK and Iran and the US escalated, sparking fears of Middle East supply disruptions. Recently, Tropical Strom Barry shuttered drilling rigs along the Gulf Coast adding to supply disruption concerns as did large drops in USD crude stockpiles. The Energy Information Administration reported that stockpiles shrunk 12.6 million barrels in the two weeks ending July 12. WTI oil prices have risen over 50% since the beginning of January and if the uptrend resumes, USDCAD will come under renewed downward pressure.

The Fed is dovish and unanimously expected to trim US rates by 0.25% on July 31. One or two more cuts could follow before year end. A “stand-pat” BoC outlook is a key driver of USDCAD weakness.

The unwinding of bullish speculative trades following the move below 1.3240 is another factor driving USDCAD since May. Speculators on the Chicago IMM have sold short Canadian dollar positions and are net long, as of July 12.

Everything is coming up roses for USDCAD bears but they before they stick their noses down to inhale the aroma, they need to be aware that Pepe le Pew is lurking in the garden.

The somewhat rosy Canadian outlook could turn into a stinker due to offshore issues. Fed Chair Jerome Powell calls them cross-currents. Market participants call them “President Trump.” The American President’s liberal use of trade tariffs is the eight-hundred pound gorilla, weighing on global growth and risk sentiment. The US/China trade talks have barely resumed, and Trump is already interfering. He threatened “We have a long way to go as far as tariffs where China is concerned. If we want, we have another $325 billion we can put a tariff on, if we want.”

The July BoC Monetary Policy Report warned of devastating consequences to the Canadian economy if, under a worst case scenario, the US/China trade war dramatically escalated. That scenario included the American’s raising tariffs on all imports to 25% and their trading partners responding with 25% on US imports.

US/China trade disruptions may be the biggest drag on USDCAD selling but they aren’t the only ones. Trump has threatened tariffs on cars imported from the European Union and the EU promised to retaliate. A “no-deal” Brexit could destabilize the entire European Union, not just the UK. The US and Iran war of words could become a war of bombs and bullets. Any or all of the above could lead to widespread risk aversion demand for safe-haven currencies.

The Canadian dollar is at cross-roads. A decisive break below USDCAD 1.3000 (CAD 80 cents) puts 1.2500 in play, which may occur on the back of a US/China trade deal. A failure to break below 1.3000 risks a rebound back to 1.3500. (CAD 74.0 cents) and a trade talk collapse or a war in the Middle east would be the catalyst.

Trade wars and shooting wars are risks but the better than expected Canadian economic data is a reality. Until that changes, the Canadian dollar won’t be singing the Summertime blues.