By Michael O’Neill

The Bank of Canada is seeing the domestic economy through rose-coloured glasses, even though they left interest rates unchanged at 1.75%. The January 9 policy statement was cautiously optimistic, noting “a Canadian economy that has been performing well overall. Growth has been running close to potential, employment growth has been strong, and unemployment is at a 40-year low. Looking ahead, exports and non-energy investment are projected to grow solidly, supported by foreign demand, the CUSMA, the lower Canadian dollar, and federal tax measures targeted at investment.” They said policy rates need to rise into a neutral range to achieve the inflation target. Last November, Mr Poloz said the neutral rate was 2.5% to 3.5%, leaving the door wide open for at least two rate hikes in 2019.

Those rose coloured glasses were smudged by oil. Low oil prices were a major concern in the policy statement as global benchmark prices were 25% lower than they were in October and they are responsible for an expected 12% drop in oil and gas investment in 2019. The Monetary Policy Report (MPR) highlighted several ways that the current level of prices affects the domestic economy. They include 1) Lower revenues for governments. 2) Lower oil and gas investment. 3) a negative impact on inflation

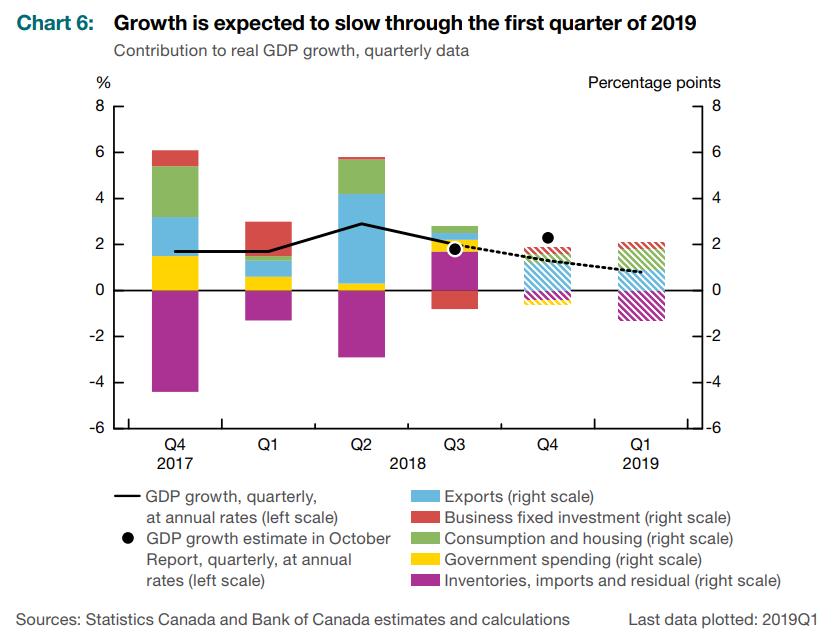

The BoC cut its 2019 Real GDP growth forecast to 1.7% from 2.1%, blaming energy sector developments and spending cuts in Ontario for the downgrade.

The oil market concerns should have led to a weaker Canadian dollar. They didn’t. Part of the reason is because the BoC expects Real GDP momentum to pick up in the second half of this year. They also raised their 2020 GDP growth forecast to 2.1 from 1.9%. The BoC statement closed by saying “Governing Council continues to judge that the policy interest rate will need to rise over time into a neutral range to achieve the inflation target.” Canadian interest rates may be going higher, but many economists believe a rate hike won’t happen until the second half of the year.

Oil prices have been good for the Canadian dollar in 2019. How long it lasts, remains to be seen. USDCAD fell 3.4% since January 3, fueled by a 15% jump in the price of crude oil. West Texas Intermediate, (WTI) the North American benchmark traded at $45.35/barrel on January 3 and $50.50/b on January 9. Even better for the Canadian dollar, the discount to WTI, charged against Alberta’s Western Canada Select (WCS) narrowed from $29.50 at the end of November to just $9.00/b on January 8. The oil market rally was sparked by a combination of Russia/Opec Production cuts that took effect at the start of this year, and higher confidence for a US/China trade deal. The prospect of higher Canadian interest rates and rising oil prices may undermine USDCAD in the coming week.

The Canadian dollar was also the beneficiary of a rebound in global risk sentiment triggered by the new Washington/Beijing negotiations and policy U-turn by Fed Chair Jerome Powell. The Fed raised interest rates on December 19 and predicted two more rate hikes in 2019, stressing that “gradual” rate hikes would be appropriate. Those words were coming after Wall Street plunged 2,151 points in December alone. During his press conference, Mr Powell sounded hawkish. He acknowledged financial market volatility but said it had not fundamentally altered the Fed’s outlook. The stock market tanked again as traders concluded that the Fed had its head in the sand.

Mr Powell changed his tune on January 4. He said the Fed could be patient with the pace of rate hikes. That’s what stock markets wanted to hear. Equities rallied, but they still have a long way to go to recoup all of December’s losses. The minutes of the Federal Open Market Committee (FOMC) were released on January 9. They also suggested that the Fed could be patient, saying “many participants expressed the view that, especially in an environment of muted inflation pressures, the Committee could afford to be patient about further policy firming.”

President Trump cannot be accused of wearing rose-coloured glasses when it comes to his demand for a Mexico border wall. That’s because he is wearing blinkers. His fixation on building a barrier across the American Southern border led to a partial shutdown of the US government. The President refuses to sign any legislation that would fund the government unless it includes money for his “wall. The Democrats refuse. The debate was elevated to a Kindergarten level on January 9. President Trump reportedly slammed his hand on a table and stormed out of a meeting with Democrat Senate Minority leader Chuck Schumer and House Speaker Nancy Pelosi. Trump summed up the meeting in a tweet: “Just left a meeting with Chuck and Nancy, a total waste of time. I asked what is going to happen in 30 days if I quickly open things up, are you going to approve Border Security which includes a Wall or Steel Barrier? +Nancy said, NO. I said bye-bye, nothing else works!” The US drama is just political theater for now, but a prolonged shutdown could be problematic for markets as scheduled government economic reports become unavailable.

2019 is not even two weeks old, but for Canadian dollar bulls, December was just a bad dream. The currency recouped all the losses that occurred since December 3. However, those expecting additional gains could be seeing things, like the BoC, through oil smudged,rose-coloured glasses.