By Michael O’Neill

There is plenty of weird goings-on in the fictional town of Hawkins, Indiana, but there are even more stranger things happening in global financial markets.

Oil prices in particular. West Texas Intermediate plunged twenty three percent in just over two weeks. That’s a sizeable decline in an unbalanced market where demand is outstripping supply. Geopolitical issues threaten a sizeable chunk of Russian crude exports, and civil turmoil in Libya reduced exports, even as Western and Chinese demand rebounds from the pandemic.

Opec promised to increase its production by 648,000 barrels per day in August, which sounds good but is really meaningless. The twenty-three member cartel cannot achieve its existing quota. In May, they missed the target by 2.6 million b/day.

So why did WTI plunge? One reason is that recession fears drove prices through the 2022 uptrend line in the $103.50-90/b area, which triggered stop-loss selling in a relatively thin market. The price drop is unlikely to last.

Russian oil sanctions are not likely to be lifted anytime soon which should underpin support at $78.50 (the pandemic low).

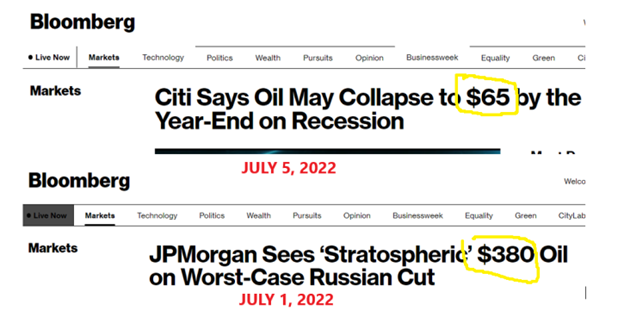

But maybe not, if Citibank economists are to be believed.

They warn that WTI could drop to $65.00/barrel if a recession hits and Opec doesn’t intervene to shore up prices.

JPMorgan economists disagree. They predict WTI at $380/b under a worst-case scenario which occurs if Russia reacts to western sanctions and cuts its own production by 5 million barrels/day. JPM suggests Russia’s economy would not be excessively damaged, but for the rest of the world, it would be disastrous.

Stranger Things indeed.

Source: Bloomberg

Another Stranger Thing is why did it take Fed Chair Jerome Powell so long to realize that rising inflation was a problem?

Mr Powell’s focus on inflation has all the fervor of a sports fan reacting to a referee’s missed call after US inflation surged to 8.3% in May.

The proof is in the pudding and in the FOMC minutes from the June 15 meeting. The minutes said. “Participants noted that the imbalance between supply and demand across a wide range of product markets was contributing to upward pressure on inflation. They saw an appropriate firming of monetary policy and associated tighter financial conditions as playing a central role in helping address this imbalance”

Policymakers said the risks for economic growth were skewed to the downside and that uncertainty about growth over the next couple of years was elevated. They agreed that moving to a “restrictive stance “was warranted and said that an even “more restrictive stance” could be appropriate.”

They raised the target for the federal funds rate by 0.75 bps and more hikes are coming. The CME Fedwatch tool shows the probability that Fed funds will be 3.5% at the December 14 meeting is 82.9%.

Investors fear the Fed is about to engineer a recession.

Any hopes of a “soft-landing” went out the window with the Fed’s tardy response to rising prices.

Mr Powell tacitly admitted that a recession was likely when he attended the ECB Conference at the end of June. He said there “was a risk” the Fed would slow the economy more than needed to drive inflation to its 2.0% target, then justified the outlook by saying, “The bigger mistake would be to fail to restore price stability.”

That’s Fed-speak for “A recession is coming-Deal with it!”

Canada is not immune.

A recession is just as likely in Canada and for the same reason as in America. Bank of Canada Governor Tiff Macklem missed the boat on inflation. He acknowledged the error at the end of April by saying, “We got a lot of things right, and we got some things wrong.”

The BoC is universally expected to raise interest rates by 0.75% next week and probably by another 0.75% on September 7. If so, it would lift the overnight rate to 3.0%, which is at the top of the 2.0-3.0% BoC neutral rate.

That is not likely to be the top.

At the beginning of June, Deputy Governor Paul Beaudry warned that if price pressures continued to rise, “it raises the likelihood that we may need to raise the policy rate to the top end or above the neutral range to bring demand and supply into balance.”

The Canadian economy has peaked. It has been operating at full capacity, which has pushed the unemployment rate to a record low of 5.1%.

The oil price shock and ongoing supply chain disruptions combined with rising inflation have many economists forecasting a Canadian recession by year-end. The only debate is its severity.

A recession is not good news for the Canadian dollar. Slowing global growth, lower commodity prices, and rising US interest rates will fuel demand for the greenback. The Canadian dollar will also suffer, but losses may be mitigated if oil prices remain elevated.

The only question is whether it will be a recession or depression.