By Michael O’Neill

The meek shall inherit the earth, but the doves have already inherited the central banks. The evidence is indisputable.

On March 27, the Reserve Bank of New Zealand predicted the next move for rates was down. Later that day, European Central Bank (ECB) President Mario Draghi doubled down on his dovish view from the March 7 meeting. That’s when the ECB pushed out their forecast for a rate increase from the end of the summer to “at least through the end of 2019.” Only three weeks later and Mr Draghi says he is prepared to delay rate moves deeper into 2020.

The Bank of Canada took a dovish turn in December following a hawkish outlook in October. They blamed the steep plunge in oil prices for their change in tune. Since then, West Texas Intermediate oil prices have recovered 88% of their October 25 levels but the BoC is even more dovish,and talk of rate cuts has entered the discussion.

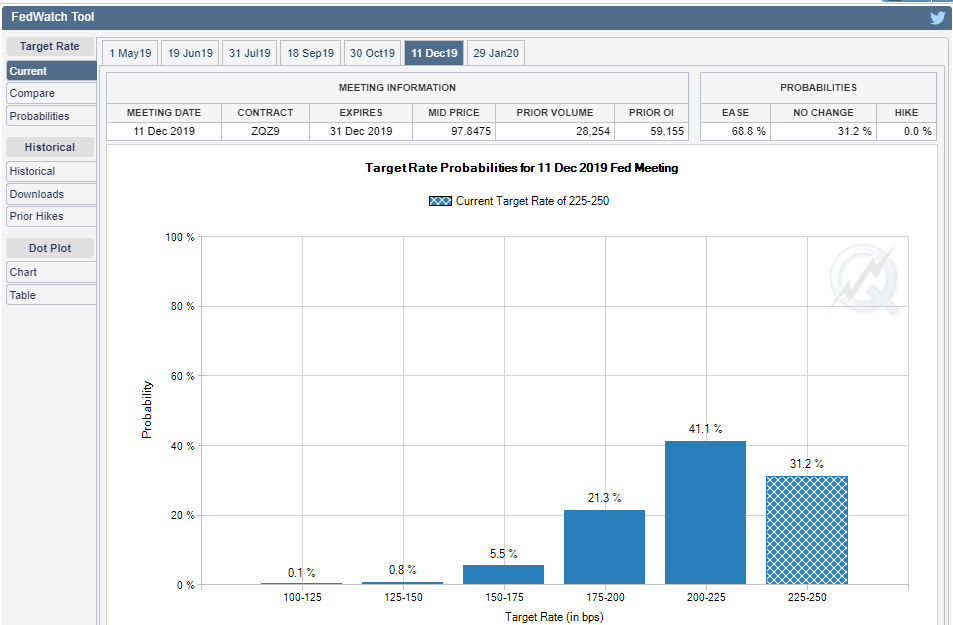

The US Fed came late to the “come as a dove” party. Six months ago, the Federal Open Market Committee (FOMC) interest rate projections for December and for 2019 were decidedly hawkish. The so-called “dot-plot” graph indicated a 0.25% rate hike in December followed by three additional increases in 2019. December came and went without any change in interest rates, and the 2019 dot-plot predications were trimmed to two. Last week, the Fed threw in the towel. They signaled that rates would be on hold for all this year. The market has taken it a step further and expects rates to be cut. The view was reinforced on March 28, when Vice Chair Richard Clarida warned that “prominent downside global risks” would keep the Fed “patient and data dependent.” The CME Group FedWatch tool shows a probability of 58.2% for September and at 71.9% in December.

CME FedWatch Tool rate probabilities for December 11 meeting.

Source: CMEgroup.com

Twenty-five years ago, moviegoers flocked to theaters to find out “What’s Eating Gilbert Grape?” Today, economists and analysts want to know “what is eating the central bankers? Why did they get their forecasts so wrong? The answer seems to be global growth or more accurately the risk that the global growth outlook is far worse than expected.

The BoC says “the slowdown in global growth has been more pronounced.” The ECB was more specific saying “persistence of uncertainties related to geopolitical factors, the threat of protectionism and vulnerabilities in emerging markets appears to be leaving marks on economic sentiment.” The RBNZ named names writing “The global economic outlook has continued to weaken, in particular amongst some of our key trading partners including Australia, Europe, and China.” The Fed is vague. The Federal Open Market Committee (FOMC) referred to “global economic and financial developments.”

More than a few central bankers point the finger at the US-led trade war for sparking the global malaise. President Trump has an itchy trigger-finger and fires tariffs at friend and foe alike. China, Canada, Mexico, Australia and the European Union have faced his wrath. Canada and Mexico capitulated to Trump’s trade demands and are worse for wear. The US has not repealed the 25% tariffs on Canadian steel and aluminum. Trump is also threatening to slap tariffs on imports of Eurozone cars to motivate the EU into trade talks. The China/US trade negotiations are on-going with markets hoping for a deal by the end of April.

Dovish central banks and talk of rate cuts have fueled a stock market rally. The S&P/TSX Composite is over 13% % since the beginning of the year. Oil prices have soared as well, posting a 36% gain, year to date. The Canadian dollar has underperformed gaining just 1.5%. The risk of the BoC cutting interest rates because of weaker than expected domestic growth and global trade worries has more than offset the benefits from resurgent crude prices. Canada still has major crude transportation issues, and China is blocking Canadian canola shipments because of its dispute with the Canadian government. The outlook for the Canadian dollar is negative, and further losses to 72.50 cents to the US dollar are in the cards.

Optimists don’t see it that way at all. They believe that the recent string of weak domestic economic reports from the US are a result of bad weather and lingering effects of the government shutdown. They think that China and the US will reach some sort of accord on trade as it is in the best interest of both nations. They point to the doom and gloom rhetoric around the Nafta negotiations before the USMCA rose from its ashes and believe the US/China talks are following the same course. The BoC believes that a resolution to the US/China trade dispute will go a long way in alleviating domestic and global downside risks.

The Fed believes that the economic risks are balanced and that the downward pressures on inflation are transitory. The doves may be in the central banks, but the hawks are lurking in the wings.