By Michael O’Neill

Nobel Prize-winning, singer and songwriter Bob Dylan sang (in the broadest definition of the term) these words fifty-three years ago. They are as relevant today as they were in 1964.

It has only been a few weeks since markets were scrambling to find safe-haven trades.

Traders were fearful that President Trump and North Korea’s Kim Jong-un would tire of trading insults and start trading missiles.

They were afraid that the Trump administration would act on the President’s threat to “shut down the government” if the debt ceiling negotiations didn’t go his way.

They were afraid that the Janet Yellen led Fed had elevated monetary policy caution to monetary policy inertia.

Traders were very concerned about the European Central Bank’s direction on monetary policy and the prospect of quantitative easing tapering.

In the UK, traders continued to deal with Brexit uncertainty and the Bank of England’s direction for monetary policy.

New Zealand trader’s started paying close attention to the upcoming September 23 election when various polls indicate that a Labour government was a possibility.

When geopolitical issues unnerve traders, they buy Swiss francs and Japanese yen. Swiss because it is a ‘neutral” country and seemingly above the petty skirmishes that occur around the world.

They buy Japanese yen because Japan has enormous foreign asset holdings. In times of turmoil, some of these assets tend to move back home. The Japanese yen is also a reserve currency and the third most liquid currency on the planet (behind the US dollar and Euro)

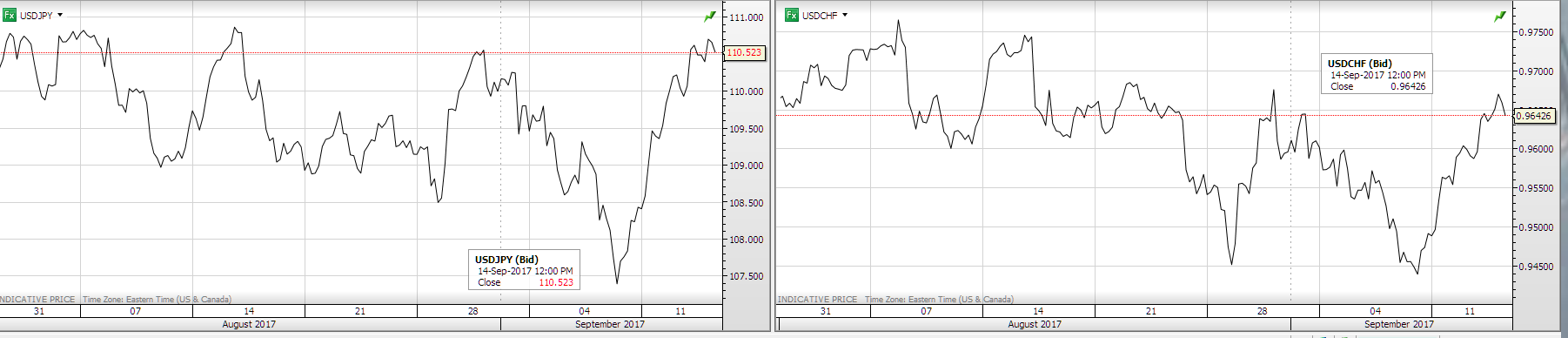

The following USDJPY and USDCHF charts show the FX price swings from August until today. For the most part, the down moves are due to risk aversion while up moves reflect the unwinding of those trades.

If August and the first few days of September were about fear and uncertainty, the second week of September, is about “The times, they are a-changing.”

The gust of wind you felt on September 11, didn’t have anything to do with Hurricane Irma. It was the huge sigh of relief from traders across the globe when the North Korean leader chose to party rather than test nuclear bombs.

USDJPY rallied and is trading where it was at the end of July. USDCHF rallied as well, but it still has room to go before it gets to the July 31 price. President Trump and Kim Jong-un have continued to trade threats this week, but until traders see mushroom clouds on the horizon, they are turning a deaf ear to them.

The Bank of Canada also signalled that the times were changing. Last week, they surprised 27 out of 33 economists, surveyed by Reuters, when they raised interest rates by 0.25 basis points. (1/4%)

More than a few economists got their noses out of joint, complaining that the Bank did not “telegraph” the move. That wasn’t an accurate complaint. BoC Governor Poloz and other officials said that monetary policy decisions were data dependent. The surprisingly strong Q2 GDP data, September 1, gave the BoC a green light to raise rates and they did.

President Trump did his part. On August 22, he threatened to close down the government over the debt ceiling. Earlier, he repeated his threat to tear up Nafta. August markets got spooked and sold dollars, and some of those dollars went to safe-haven currencies.

On September 6, President Trump put “The Art of the Deal” into practice. He realised that he was struggling to get his own party to work with him, so worked with the Democrats. They struck a bipartisan deal to increase the debt limit until the middle of December. Crisis averted. (deferred)

The European Central Bank’s (ECB) intentions were another source of concern for FX traders. Various ECB officials offered conflicting views about future monetary policy decisions. Most agreed that monetary stimulus needed to be reduced, but there wasn’t any consensus on the timing of such a move. All indications were that the issues would be resolved at the September 7 meeting. They weren’t.

However, ECB President Mario Draghi gave broad hints that a tapering announcement may occur in October.

In the UK, Brexit uncertainty is still a major issue, but Bank of England monetary policy direction isn’t. The September 14 monetary policy statement put a rate hike at the top of the agenda for the November meeting. If they raise rates by 0.25 bps, it will only replace the post Brexit Referendum cut of July 2016.

“The times they are a changing may be most clearly evident in New Zealand.” The National Party, led by Bill English has been in power since 2008. Their reign may be ending if the latest 1News Colmar Brunton poll is accurate. Jacinda Ardern’s Labour Party has a four point lead, and if that lead holds until September 23, she will be the next Prime Minister of New Zealand