By Michael O’Neill, Agility FX Senior Analyst

Bob Dylan, an American songwriter and “singer” and the 2016 Nobel Prize winner for Literature, released a song, “The times they are a-changin’ and album of the same title, in 1964.

Those words are as relevant today as they were fifty-three years ago and more so in the context of the Federal Reserve Open Market Committee. (FOMC)

In the middle of February, the CME FedWatch tool posted odds for a rate hike on March 15 at a mere 20%.

Since then, various Fed officials, from Fed Chair Janet Yellen, to noted dove, Cleveland Fed President Lael Brainard have signaled that a rate hike was a definite possibility in March. The odds are now at 80%.

What happened?

The robust US employment picture, a series of better than expected economic releases and hawkish comments from Fed officials gave the US dollar a boost while putting upward pressure on yields. On March 8th, the US 10-year yield had punched above resistance at 2.50% and was trading at 2.55%.

That is a big shift in sentiment and an even bigger leap of faith considering how rate hikes in 2016 played out.

The December 2015 Summary of Economic projections forecasted four, quarter point increases in 2016. They only hiked once and that wasn’t until December 2016. In between, various Fed officials signaled rate hikes for the June meeting and then again at the September meeting. Both times, the Fed stood pat and traders got burned.

The December 2016, Summary of Economic Projections, predicted three, quarter point rate increases in 2017

Traders were skeptical which is why the odds for a March rate hike were so low.

Now, instead of being skeptical, traders should be nervous. The 2016 “uber-cautious” FOMC may have transformed to a 2017 “Daredevil”

“Is this the FOMC’s alter-ego?” Source: Marvel Comics

A March 15 rate hike is just 2 ½ months into the year leaving plenty of room for further increases. A quarter point bump in June, September and December would push the target Fed funds rate range to 1.5-1.75%.

It could happen. US employment levels are at or very near, levels where many economists consider it to be ‘full-employment”. That is Mandate 1 of the Fed’s dual employment and price stability and it has been fulfilled.

Mandate 2, is inflation at 2%. That goal is expected to be achieved over the “medium term” according to the FOMC minutes although a downward shock in oil prices or other commodities would delay the move. If 2% inflation levels are hit sooner than expected, US interest rates could rise faster than expected.

A former Treasury employee, Aaron Klein told CNN on March 6, that the Fed was racing to get rates to 1.5% to provide them with “wiggle room” in the event of an economic slowdown”.

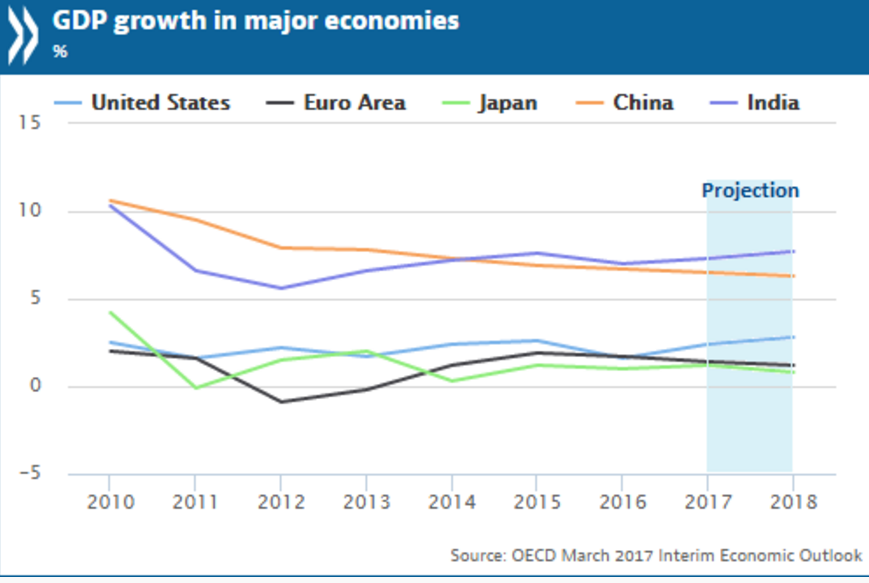

The prospect of four rate hikes in 2017 gets added support from an improving outlook for global growth. The Organization for Economic Cooperation and Development (OECD) have bumped their 2017 Global GDP forecast to 3.6% from 3.3% based on continuing and expected combined fiscal and structural initiatives in the major economies.

President Trump’s infrastructure spending plans and his corporate tax cut promises have the potential to make a bigger impact on US economic growth and inflation when the details get announced.

Nevertheless, if you want to make God laugh, tell him your forecasts.

Oil prices are under duress. Speculators bought contracts expecting that the oil price rally that occurred after the Opec production cuts would continue above resistance in the $56.00/barrel area. The rally stalled at the end of February and a spate of reports showing large increases in US crude inventories led to a price drop of 9% as of March 8.

Further oil price losses would have a negative impact on inflation and reduce the necessity for more US rate increases.

Geopolitical issues could derail global growth prospects and not just because of ongoing Middle East issues. Russia, China, North Korea, South Korea and the US are all exchanging pleasantries over recent developments.

The Vice Chairman of the US Joint Chiefs of Staff said that Russia has deployed a land based cruise missile that poses a threat to Nato. North Korea is dropping missiles into the Sea of Japan which Japan’s Prime Minister called a “serious violation of UN Security Council resolutions. The United States deployed a Thermal High Altitude Area Defense system (THAAD) in South Korea, much to China’s chagrin. China is very unhappy with some of the features of the weapon and threatened unspecified measures against South Korea.

Geopolitics, fiscal stimulus and monetary policies are always in a state of flux and this year will not be any different. The Times may be a-changing and 2017 could see some big ones.

.