August! It is the middle of summer. For many the hot, lazy days are spent hanging out on a beach, enjoying the warm weather and sunshine. FX traders refer to these kinds of days as the “summer doldrums.”

Those doldrums may not be anywhere to be found on Friday August 4. That’s because it is a big day for economic data. The monthly US nonfarm payrolls (NFP) report is released at 8:30 am EDT. The forecast is for an increase of 183,000 jobs in June, compared to a 222,000 gain in May.

Volatility in currency markets has been known to explode when the actual data shows a sizeable deviation from what the experts have predicted.

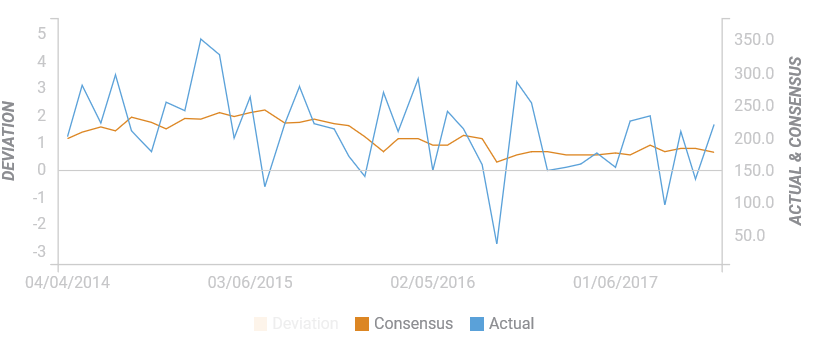

The following chart (Chart 1) shows the history of nonfarm payrolls forecasts, comparing the consensus estimate against the actual result, since April 4, 2014. Consensus is the orange line while the Actual result is in blue.

For FX traders, the current thinking for nonfarm payrolls is that it is a barometer for the health of the US economy. Large upside surprises from the forecast mean that the economy is growing faster than expected which if true has implications for interest rates and inflation. Conversely a downside surprise suggests that the economy is not as strong as previously thought.

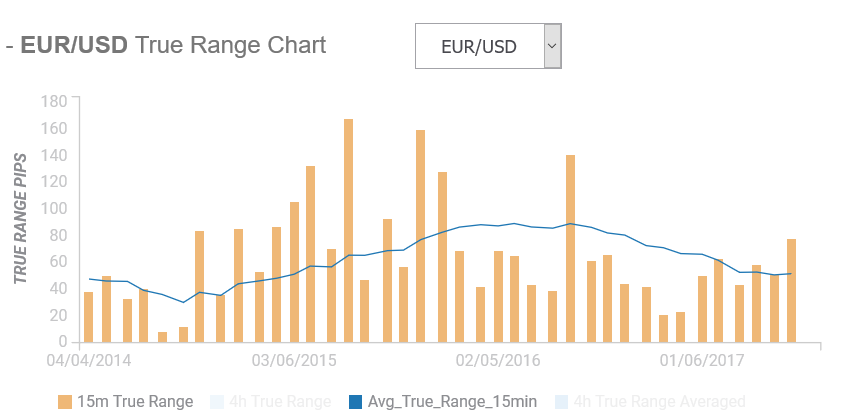

That thinking leads to some size able price swings. Chart 2 shows the number of points that EURUSD moved when NFP was released, over the same period as Chart: 1

The scale on the left represents the number of EURUSD points (20 is equal to 0.0020) that EURUSD moved, either up or down. The Orange bars show the 15-minute volatility while the Blue line is the normal 15-minute volatility.

There is a school of thought that suggests Friday’s data will have a bigger impact on FX markets from weak data than it would from strong data.

The Federal Open Market Committee met less than two weeks ago, and left interest rates unchanged. The policy statement said that “in view of realized and expected labor market conditions and inflation,” they would leave rate unchanged. They were far more concerned with the low rates of inflation, which is why analysts and economists downgraded expectations for another interest rate increase in 2017. Arguably a weaker, number is a big US dollar negative as it reinforces the “Fed is on hold view.”

Canada employment data is also released on Friday. This is a notoriously volatile series, oftentimes resulting in wild USDCAD price swings.

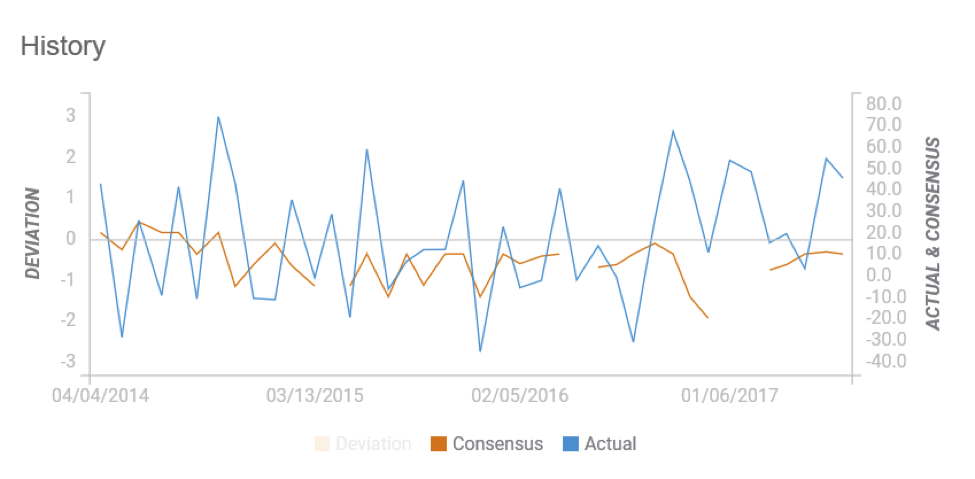

Chart 3 shows the Canadian employment results (Blue line) against the consensus forecast (Orange line)

Canada has posted job gains in nine consecutive months, starting in December 2016. That performance has led to Canadian bank economists predicting a flat to a small 12,500 rise in July jobs, well below the 45,300 jobs created in June.

Meanwhile, the Canadian dollar has been on a tear, rising from 74.25 cents to 80.55 cents against the US dollar since June 12. That was the day the Bank of Canada announced a hawkish shift to monetary policy. in a speech by Deputy Governor Carolyn Wilkins. A quarter-point rate hike followed on July 12.

Even as the domestic economic outlook had turned “perky,” a series of external influences combined to accelerate the Canadian dollar rally.

Opec and non-Opec production caps and talk that the production cuts would be extended beyond their March 2018 expiry date lifted oil prices. The prices got an added lift on news that Nigeria was on the cusp of agreeing to a production cap. Closer to home, US crude inventories were starting to decline. All the above contributed to the 20 percent rise in WTI oil prices from June 12.

President Trump’s dysfunctional administration added a layer of “political uncertainty” to global FX markets. His inability to repeal Obamacare, the relentless press coverage about his election campaign ties to Russia, and the revolving door of Senior White House Administrators led to broad US dollar selling. Traders no longer expect Trump’s tax cut/infrastructure spending promises to be fulfilled.

The European Central Bank undermined the greenback when various officials talked of the need to begin tapering the quantitative easing program. The prospect of the ECB tightening while the Fed was on hold led to an explosion of EURUSD demand which gained 7.2 percent since June 12.

None of the external influences are going away any time soon, which leaves the US dollar on the defensive. A weaker than expected NFP report and stronger than forecast Canadian jobs report would be an explosive combination for the Canadian dollar. That volleyball would be spiked so hard, Canadian dollar bears would be eating sand.