By Michael O’Neill

“A weaker dollar is good for us.” With these words, US Treasury Secretary Steven Mnuchin appears to have announced a reversal of America’s long-standing “strong-dollar” policy.

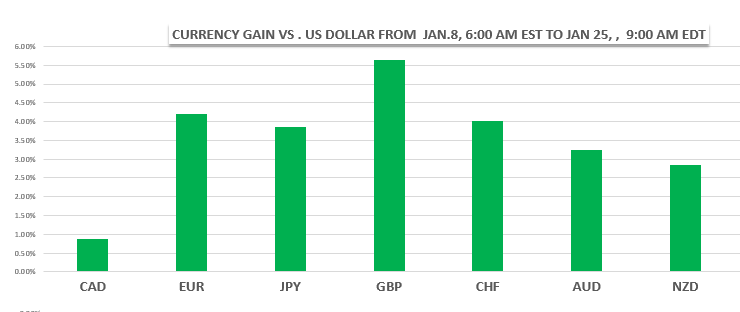

Currency markets certainly thought so. The words were barely out of his mouth when a fresh wave of US dollar selling occurred, intensifying the 2018 slide. The following chart highlights the US dollar losses which began on January 8, the first full week of trading.

Source: Saxo Bank/IFXA

The problem is, the US government strong-dollar policy was never a true policy, merely a phrase that came into vogue in 1995. Secretary of the Treasury Robert Rubin said that a strong exchange rate for the dollar was in the US national interest and the interest of the rest of the world. Since then, his words have been echoed by many government officials in various administrations. The result was the illusion of a substantive policy rather than the reality that the words were empty rhetoric. Simply put, it was all talk, no action.

A strong dollar policy would imply that the US would act to support the currency. They haven’t. The US government has not intervened in FX markets in 30 years. On June 17, 1998, they sold $833 million US dollars to buy Japanese yen. It was a coordinated effort at the behest of the Bank of Japan to shore Japan’s free-falling currency. That action did not have anything to do with a “strong dollar-policy.”

Treasury Secretary Mnuchin’s comments were not original. The real “weak dollar” chatter began in April 2017, when President Trump complained the dollar was too strong. Since then, the US dollar devalued 18.2% against the euro, 15.5 % against the British pound and 8.2% against the Canadian dollar.

A corner stone of President Trump’s election platform was trade reform. He believes the US is disadvantaged by current trade practices citing US trade deficits as evidence. He quit the TransPacific Trade Partnership and is renegotiating the North America Free Trade agreement. He has imposed new tariffs and countervailing duties on a host of imports from China, South Korea, and Canada. Talk of a “weak dollar” seems like just another negotiating ploy to win concessions from trade partners.

The Canadian dollar has been a victim of the President’s trade reform agenda. On January 17, the Bank of Canada raised the overnight rate by 0.25%, a move that usually results in Canadian dollar gains. After an erratic few hours, USDCAD settled into a 1.2390-1.2510 range until the Mnuchin’s comments in Davos. The Bank of Canada’s stated concern around the NAFTA talks overshadowed the rate hike.

There is a school of thought that the BoC’s Nafta concerns are valid. They believe that Justin Trudeau and his party changed their minds about signing up to the TransPacific Partnership because they think the Nafta agreement is headed to the shredder.

Another factor undermining the US currency is the perception that the US yield advantage will erode quickly as rates in other G-7 nations normalize policy.

That perception doesn’t hold up to scrutiny. The forecast for Fed funds at the end of 2018 is 2.5%. The ECB deposit rate is expected to be unchanged at -0.4%. Canadian rates will have risen to 1.75-2.0%, at, or below the expected US rate increase. In the UK, the forecast is for rates to rise just 0.5% in 2018.

European Central Bank President Mario Draghi seemed to confirm that outlook on January 25. The ECB left rates unchanged and issued a statement almost identical to December’s. Mr Draghi insists that the Eurozone needs “easy money” and will do so for a very long time. EURUSD traders are skeptical of Mr Draghi’s claims and have voted with their wallets, pushing the single currency to levels last seen in December 2014.

The US focus on trade and speculation about a “weak dollar’s bias for the US administration, has elevated the uncertainty around the Canadian dollar. The BoC expects Canadian GDP growth at 2.2% and with two or three rate increases this year, the Loonie should be expected to trend higher.

On the other hand, the new American tax reform policies which may lead to hundreds of billions of dollars being repatriated from offshore (creating US dollar demand) and the risk that Nafta gets revoked, limits Canadian dollar upside. WTI oil prices, which have climbed to $66.60/barrel from $59.00/b at the beginning of the year are not giving much of a benefit either. Part of the reason is that Western Canada select (Canada’s main crude export) is trading at a $28.31 discount to WTI.

The American “strong dollar “policy is just an idea that is all hole, no doughnut. So is the notion of a “weak dollar” policy. President Trump and Treasury Secretary Mnuchin may just be stirring the pot to improve their trade reform stance.