Photo: HSclipartall.com

January 30, 2023

- No shortage of market moving events this week

- Geopolitical tensions percolating

- US dollar opens mixed-CAD unchanged.

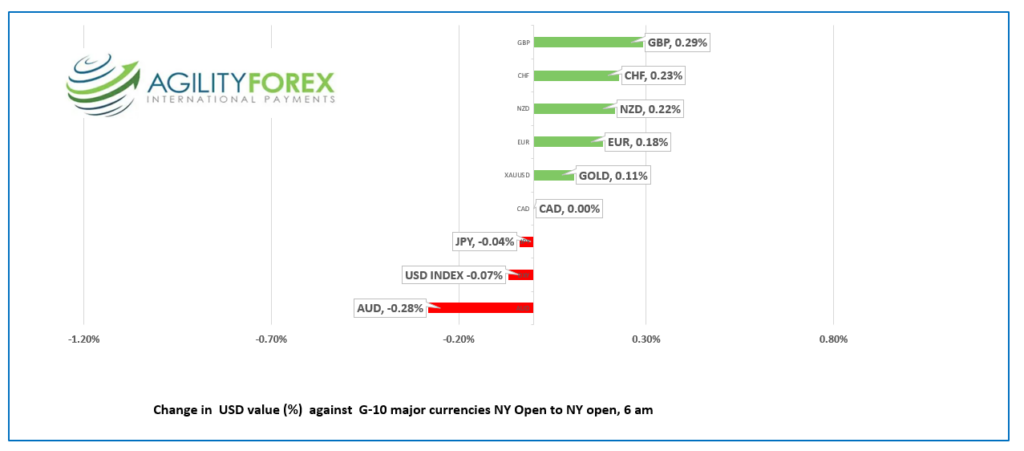

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3316-20, overnight range 1.3302-1.3352, close 1.3122

USDCAD opened today, unchanged from Friday’s opening level, after spending the overnight session bouncing in a 1.3302-1.3352 range.

USDCAD has a mildly bearish bias while traders await direction from Wall Street and the FOMC decision. The BoC decision to tell markets that rate hikes are on hold may lead to a higher USDCAD depending on the tone from the FOMC meeting.

WTI oil prices consolidated Friday’s losses in a $78.78/b-$80.48/b and are trading at $79.66/b in NY. Prices are defensive due to fears of renewed US dollar strength following a Fed rate hike, while losses are limited by hopes of Chinese demand, post Lunar New Year.

There are no Canadian economic reports today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish while trading below 1.3360, looking for a decisive break below the 1.3300-10 area to extend losses to 1.3250. A move above 1.3360 targets the daily downtrend line at 1.3400, which if broken, negates the downside pressure and targets 1.3500. A break below 1.3250 suggests further losses to 1.3080.

For today, USDCAD support is at 1.3300 and 1.3250. Resistance is at 1.3360 and 1.3380.

Today’s range 1.3280-1.3360

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Markets started the week as nervous as Nellie near a glue factory. There is a plethora of risk events staggered through the week, both market and geopolitical. Israel reportedly launched a drone strike on a military factory in Iran at the same time twitter reports a new wave of civilian protests in the country.

Turkey (a Russian ally) continues to thwart Sweden’s application into NATO, while a Senior Chinese diplomat, Wang Yi is visiting Putin in February.

US General Mike Minihan id his part to inflame tensions with China. He is charge of Air Mobility Command and he wrote a memo saying his gut tells him America “will fight China ins 2025.

WWW lll is just one item on the risk agenda this week. Traders have to deal with the usual month-end portfolio rebalancing adjustments along with three major central bank meetings, the Fed on Wednesday, and the BoE and ECB Thursday.

Thursday also brings quarterly earnings reports from the Triple-A’s, Apple, Amazon, and Alphabet.

The week ends with US nonfarm payrolls which are expected to rise by 175,000 compared to 223,000 in December.

Asia equity indexes closed mixed. Japan’s Nikkei 225 posted a tiny 0.10% gain, while Australia’s ASX 200 lost 0.16%. European bourses are trading with a negative bias. The German Dax is down 0.92%. S&P 500 futures have lost 0.93%

EURUSD dipped to 1.0854 in Asia then rallied to 1.0913 by the NY open, boosted by a surge in inflation in Spain (HICP actual 5.8% y/y vs 5.5% in Dec.). The results underscored expectations for the ECB to hike 50 bp and issue a hawkish outlook. Traders are ignoring the German Q4 GDP report which showed the economy contracting by 0.2% q/q, which was worse than expected. Euro area Economic Sentiment, Services Sentiment, and Business Climate improved in January.

The hourly EURUSD technicals are bullish above 1.0820, looking for a move above 1.0930 to extend gains to 1.1000.

GBPUSD traded choppily in a 1.2370-1.2416 range with prices little changed from Friday’s close. Most analysts expect the BoE to hike by 50 bps on Thursday, but others expect a 25 bp hike. GBPUSD is mildly bid above 1.2340, with a break above 1.2430 targeting 1.2500.

USDJPY traded in a 1.2922-130.28 range , dropping to the bottom in Asia, before climbing to 130.23 in NY. Prices are underpinned by the expectations for a hawkish FOMC meeting and the tick higher in the US 10-year Treasury yield, to 3.535% today from 3.518% at Friday’s close.

AUDUSD is at the bottom of its 0.7070-0.7119 range due to commodity currency bloc selling pressures ahead of the FOMC meeting.

NZDUSD traded in a 0.6474-0.6506 range. Prices were underpinned by news the trade deficit narrowed to NZD 475 million from -2.18 million in November, but those gains evaporated in early European trading.

There are no top tier US economic reports today.

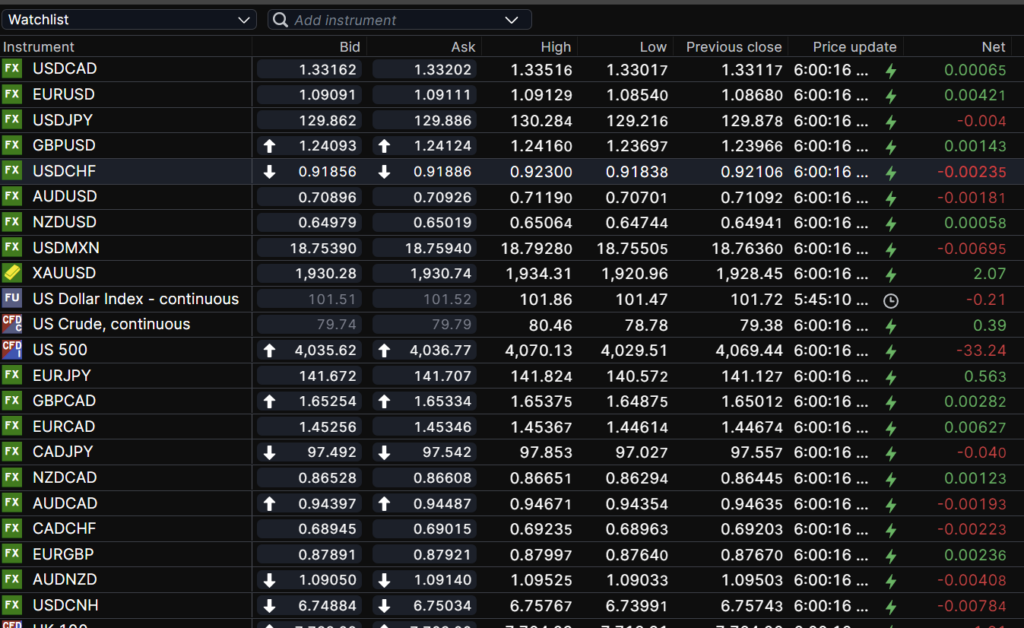

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Bank of China Fix: 6.7626, Jan. 20,2023, 6.7702,

Shanghai Shenzhen CSI 300, 4201.34 closed Jan 20, 4181.53.

PboC to extends carbon-reduction credit facility to the end of 2024.

State Council pledged to consolidate and expand the momentum of economic rebound, accelerate recovery in consumption, and stabilise foreign trade and investment.

China CDC said there was no significant Covid rebound during Lunar New Year.

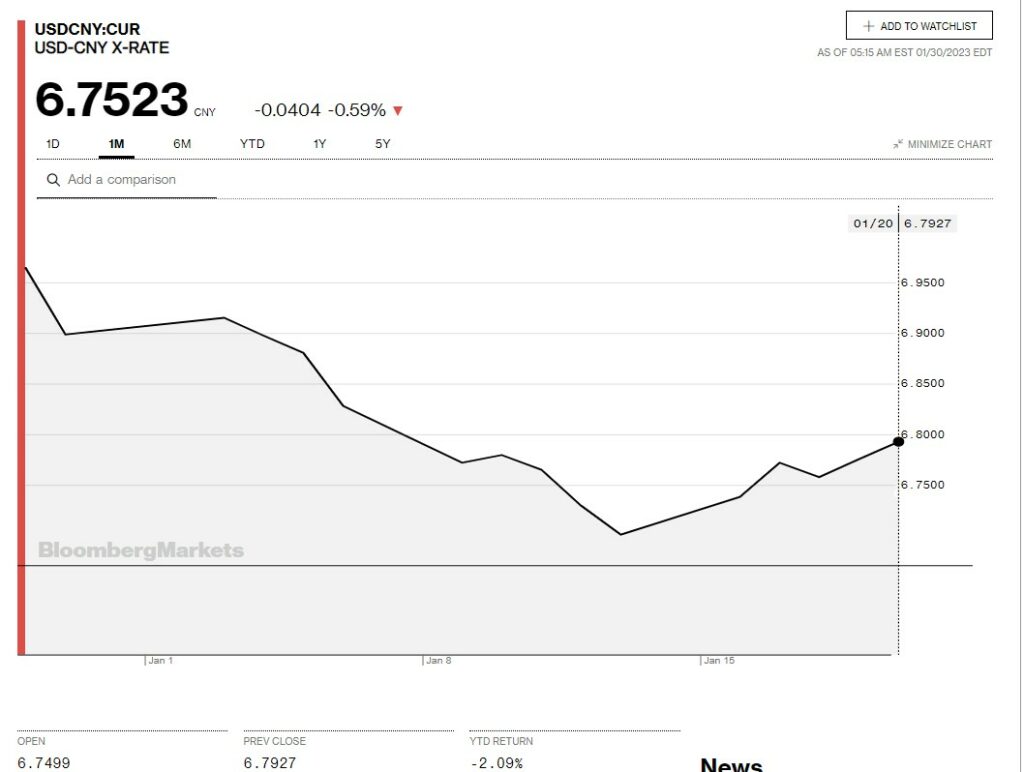

Chart: USDCNY 1 month

Source: Bloomberg