May 21, 2025

USDCAD: open 1.3888, overnight range 1.3868-1.3922, close 1.3918,

USDCAD retreated after Canadian headline inflation rose just 1.7% in April, a sharp drop from March’s 2.3% pace. The decline came courtesy of the federal government finally taking Pierre Poilievre’s advice and “scrapping the tax.” The irony is rich: during the post-COVID inflation crisis, the same Liberal government claimed to be doing everything possible to control inflation—when apparently, all it really needed to do was axe the carbon tax.

But that isn’t the biggest reason for USDCAD losses—the credit goes to Trump’s tariff and budget plans. Traders are voting with their wallets and dumping US bonds, and dollars.

The G-7 Finance Ministers are meeting in Banff and markets are wary of reports of currency valuation discussions.

WTI oil prices rallied from 62.24 to 63.69 after the API crude stocks report showed inventories rose by 2.49 million barrels. Prices consolidated the move overnight with prices underpinned by reports that Israel may bomb Iran’s nuclear sites.

The Canada New House Price fell 0.4% m/m in April. There are no top tier US economic reports today.

USDCAD Technicals

USDCAD snapped its weekly long uptrend on the break of 1.3910 and while prices are below 1.3960, the risk is for further losses to 1.3840, then 1.3805. A break above 1.3960 negates the downside and shifts the focus to 1.4000.

The medium term technicals are bearish while trading below 1.4020 but mixed momentum indicators suggest further consolidation,

For today, USDCAD support is at 1.3840 and 1.3805. Resistance is at 1.3920 and 1.3960.

Today’s Range: 1.3820–1.3920

Chart: USDCAD 4 hour

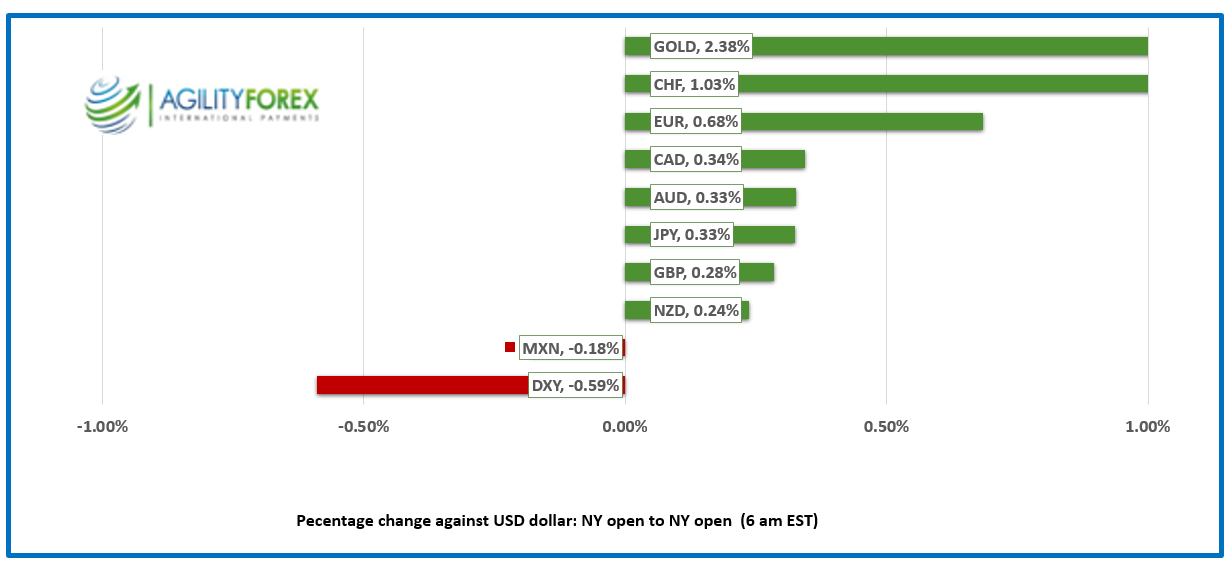

FX at a Glance

Going Nuclear

Oil prices climbed on reports that Israel is preparing to launch a strike on Iran’s nuclear facilities. China is conducting land invasion drills near Taiwan, Japan is showcasing next-generation missiles, rail guns and research into lasers, while Trump appears to have surrendered Ukraine to Russia. Meanwhile, Trump’s tariff strategy and budget bill is unnerving bond markets, who are driving yields higher across the board. In addition, traders are concerned that the G-7 Finance Ministers, who are meeting in Banff, Alberta, may have currency discussions on the agenda.

Global Equity Markets are Mixed – Greenback Falls

Wall Street snapped a 6-day winning streak yesterday. The S&P 500 led the major indexes lower, closing with a loss of 0.39%. Asian traders didn’t care and Australia’s ASX 200 gained 0.52%, while the Hang Seng added 0.62%. Japan’s Topix lost 0.22%.

European bourses are in negative territory. The French CAC-40 has lost 0.62%, while the German Dax is down 0.26%. The UK FTSE 100 is flat. S&P 500 futures are sliding and have lost 0.52 (as of 5:30am PT). Safe-haven demand for gold has lifted XAUUSD from yesterday’s low of 3204.71 to 3312.40 in New York. The US 10-year Treasury yield climbed to 4.54% from Monday’s low of 4.483%.

A slew of Fed officials speaking on Monday indicated little desire to ease monetary policy any time soon due to the uncertain economic outlook. They are concerned about the impact of Trump’s tariffs on inflation as well as instability in the Treasury market.

EURUSD

NY Open: 1.1334, Overnight Range: 1.1281-1.1353

EURUSD extended yesterday’s gains and climbed steadily due to more widespread US dollar selling on fears that Treasury Secretary Scott Bessent will tell G-7 Finance Ministers that the US wants a weaker dollar. The semi-annual EU Financial Stability Review warned that upbeat credit and stock markets appear to be out of sync with trade and geopolitical uncertainty, citing tariffs as a “major downside risk.”

GBPUSD

NY Open: 1.3411, Overnight Range: 1.3383-1.3469

GBPUSD rallied in Asia and peaked at 1.3469 when UK inflation jumped to 3.5% from 2.6% y/y in April. The increase was blamed on the government’s tax policies. Prices quickly dropped to the session low due to stagflation fears. Prices recovered somewhat because in the short term, the hotter inflation reading reduces the odds for further Bank of England rate cuts.

USDJPY

NY Open: 143.99, Overnight Range: 143.46-144.62

USDJPY dropped, popped, then dropped again as hopes for successful tariff negotiations and safe-haven demand for yen overshadowed surging Treasury yields. The selling pressure is also supported by earlier comments from BoJ Deputy Governor Shinichi Uchida, who told the Japanese parliament that rates would rise if inflation stays around its 2.0% target.

AUDUSD

NY Open: 0.6439, Overnight Range: 0.6417-0.6459

AUDUSD eked out small gains due to broad US dollar weakness stemming from comments by Fed policymakers warning of an uncertain economic outlook. Those comments pushed yesterday’s remarks by RBA Governor Michele Bullock suggesting more rate cuts to the back burner.

NZDUSD

NY Open: 0.5930, Overnight Range: 0.5918-0.5955

Kiwi got a lift from US dollar pressures and because of the higher-than-expected trade surplus, which rose to $1.42 billion from $794 million in March.

USDMXN

NY Open: 19.3003, Overnight Range: 19.2596-19.3072

USDMXN had a choppy session with domestic politics, increasing global trade tensions and a widespread flight out of US dollars roiling the market. Retail sales jumped to 4.3% in March compared to the 1.1% decline in February.

China Snapshot`

PBoC fix: 7.1937 vs exp. 7.2133 (Prev. 7.1931)

Shanghai Shenzhen 300 rose 0.47% to 3916.38

Chinese troops are practicing for what will be the inevitable invasion of Taiwan by holiding an amphibious landing drill in the Taiwan Strait on Tuesday,

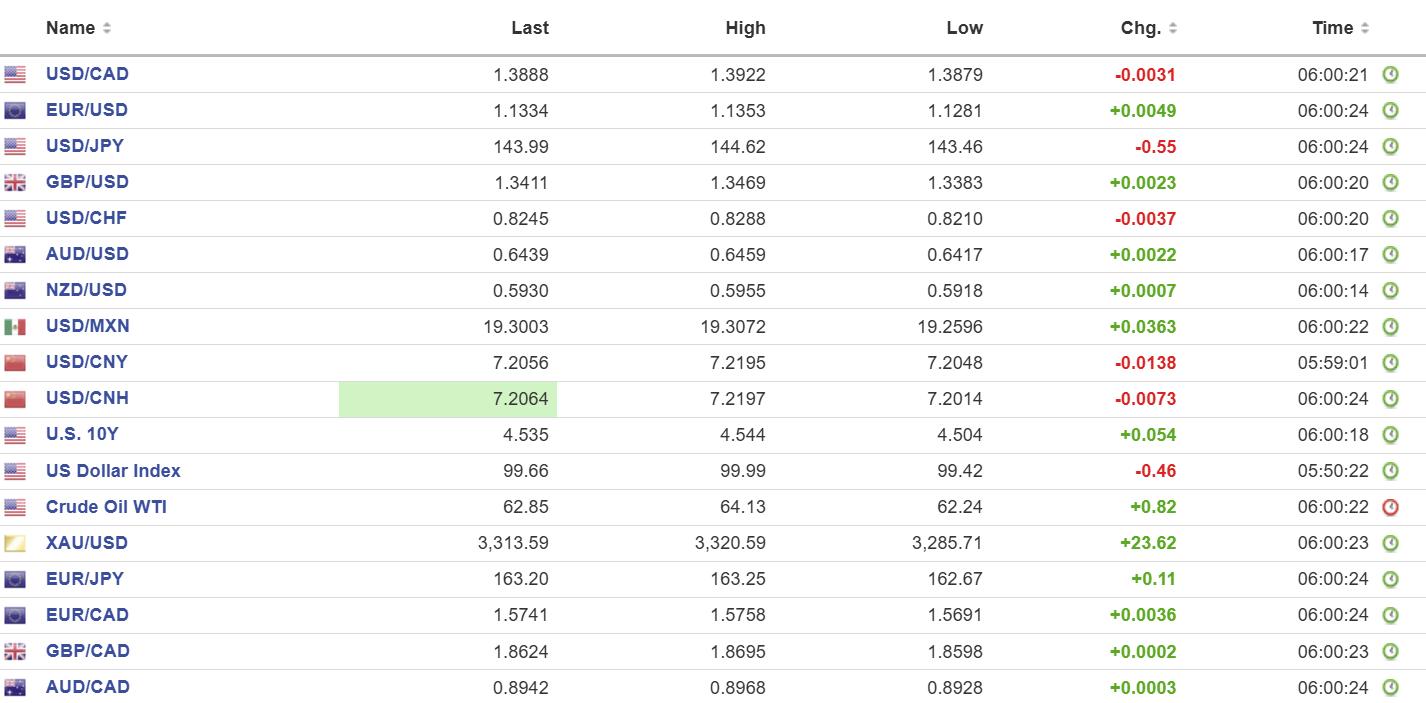

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.