Agility Daily FX Commentary

June 11, 2025

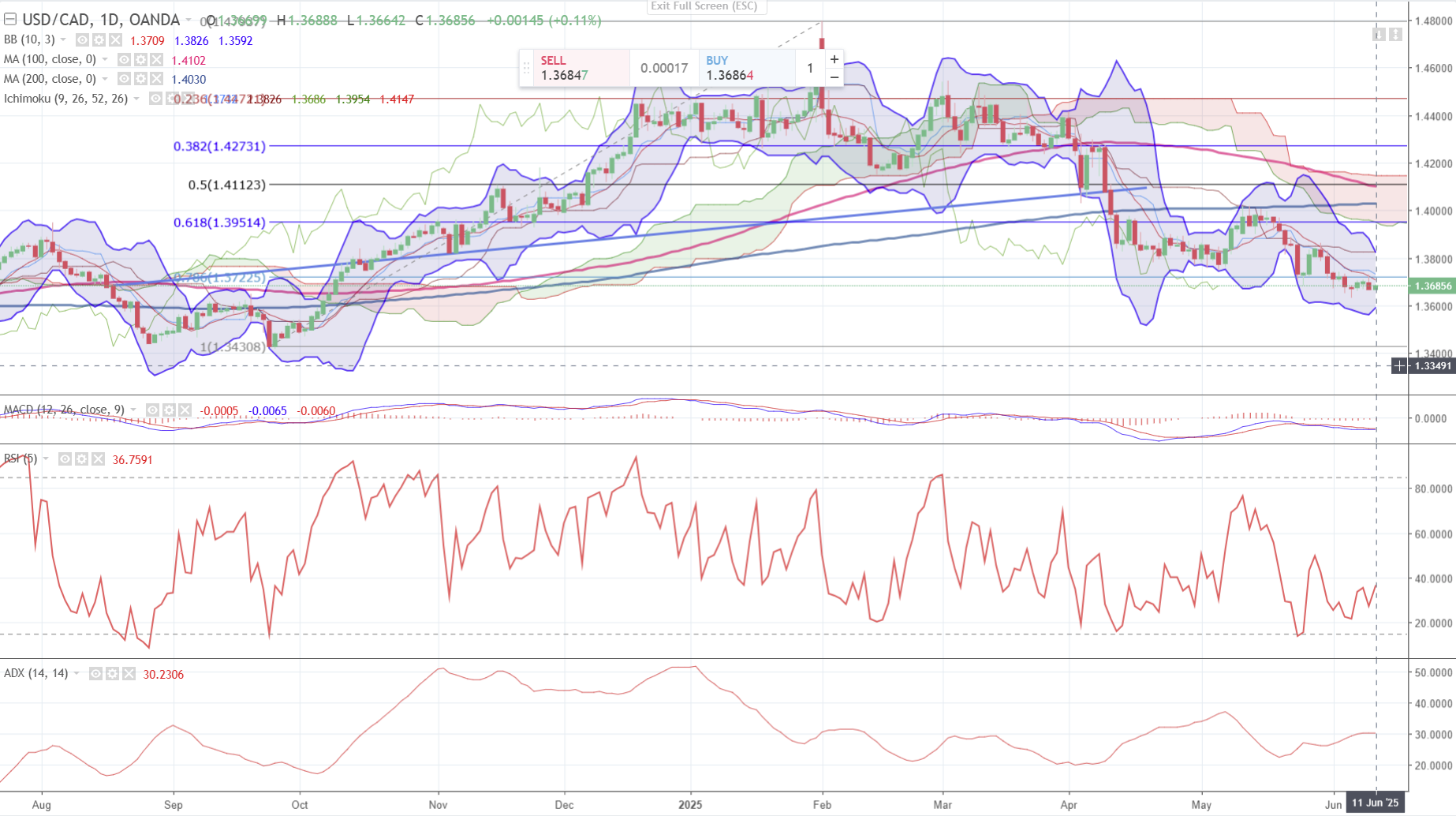

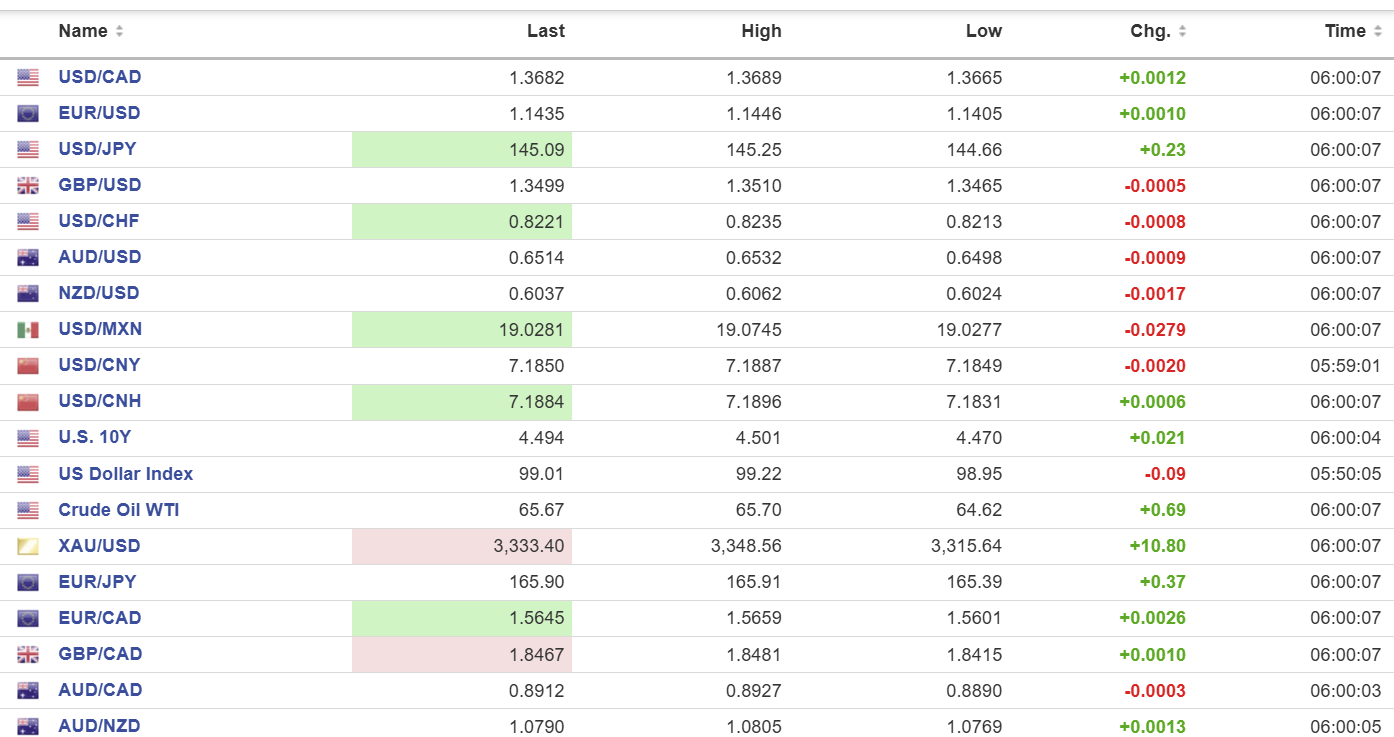

USDCAD: open 1.3682, overnight range 1.3665-1.3689, close 1.3674

USDCAD is marginally lower on the back of broad-based US dollar weakness and found a bottom at 1.3650 after this morning’s US inflation report. USDCAD may be weighed down on speculation that Trump and Prime Minister Carney may announce a bilateral trade deal at the G-7 summit.

The story broke last week and since then it has faded from the news wires. Yesterday’s news that Mexico and the US are discussing removing tariffs on steel up to a yet to be determined quota, suggests Canada and the US may be having similar discussions.

WTI oil traded in a 64.62-65.70 range overnight then climbed to 65.95 in NY trading. Prices were underpinned yesterday after the Secretary-General of Opec, Haitham Al Ghais told a Calgary audience that there was “no peak oil demand on the horizon.” He said that global investment needs for new oil and gas are $17.4 trillion while achieving the “net-zero emission” dream would cost $100 trillion over the next 25 years.

Canada Building Permits fell 6.6% in April

USDCAD Technicals

The intraday USDCAD technicals are bearish while prices are below the 1.3710-1.3750 area supported by bearish momentum indicators. A break below support in the 1.3630-1.3660 area would extend losses to 1.3580

The medium term technicals remain bearish with prices below the key moving averages and targeting the 2024 low of 1.3430 on a break below 1.3600.

For today, USDCAD support is at 1.3650 and 1.3610. Resistance is at 1.3710 and 1.3750

Today’s Range: 1.3630-1.3730

Chart: USDCAD daily

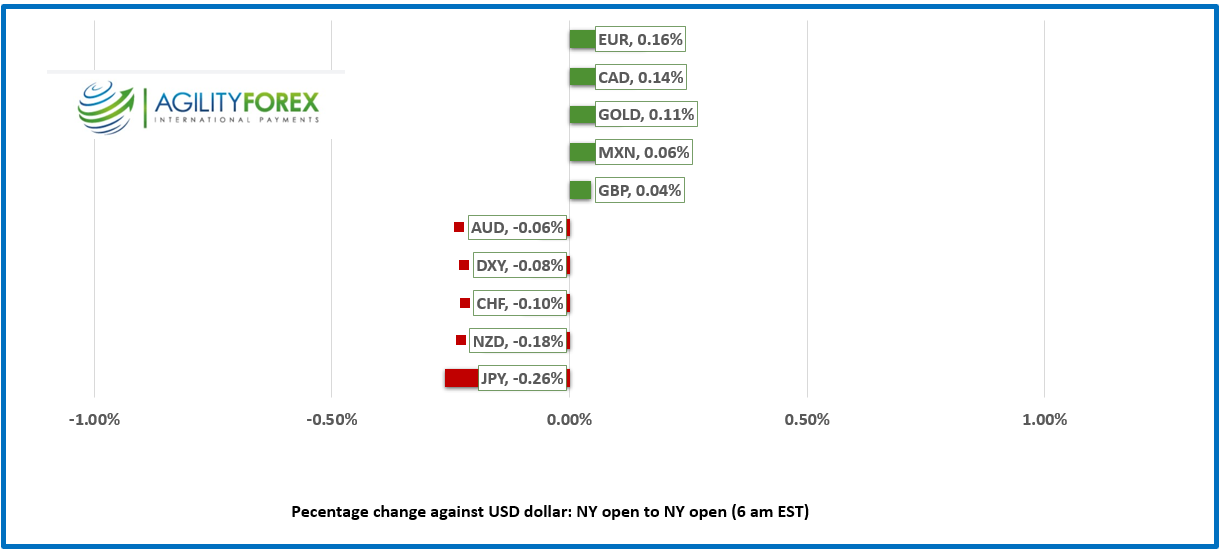

FX at a Glance

US/China “Framework” Light on Details

China’s top trade negotiator Li Chenggang told reporters, “The two sides agreed in principle a framework for implementing the consensus.” That is almost the identical language that US Commerce Secretary Howard Lutnik used to describe the outcome of the China/US trade talks in the UK. No further details were forthcoming, and traders quickly shifted their focus to today’s US inflation numbers.

Inflation Numbers More Noise Than Trend.

The impact of Trump’s Liberation Day tariffs on inflation did not live up to advance billing. Headline CPI would rose 2.4% y/y (forecast 2.5%, previous 2.3%). Core CPI rose 2.8% y/y (forecast 2.9%, previous 2.8% y/y). The month over month numbers showed Core CPI rising 0.1% compared to the forecast for a 0.3% m/m increase.

Analysts immediately dismissed the data as “noise” and not a trend. That makes sense as the US Court of Appeals ruled the Trump Liberation Day tariffs can remain until at least July 31, when arguments will be heard. Tariff inflation has more time to become entrenched.

Equities in the “Green”

US and China trade deal optimism helped Wall Street close with gains, and that continued overnight with news of a “framework.” Hong Kong’s Hang Seng Index rose 0.84%, while Australia’s ASX 200 and Japan’s Topix gained marginally. In Europe, the German DAX is up 0.54%, while the French CAC 40 has gained 0.18%. S&P 500 futures turned positive, post CPI and are up 0.26%. Gold (XAUUSD) is 3336.21and the US 10-year Treasury yield dropped to 4.433, post-CPI from 4.50% earlier. (as of 6:00 am PDT)

EURUSD

NY Open: 1.1435, Overnight Range: 1.1405–1.1446

EURUSD traded with a bit of a bid due to modestly bearish US dollar sentiment ahead of today’s US inflation data, which is expected to rise. EURUSD remains underpinned by a spate of somewhat hawkish comments from ECB policymakers in the wake of last week’s meeting. Analysts are anticipating that the ECB will remain on hold until September.

GBPUSD

NY Open: 1.3499, Overnight Range: 1.3465–1.3510

GBPUSD found a bottom in Europe which was close to the base of the April 10 uptrend line at 1.3435. GBPUSD lost upside momentum yesterday after the weaker-than-expected employment data, but it is US developments that are driving prices today. Longer term, GBPUSD gains may be harder to achieve as the Bank of England may turn dovish due to falling inflation and wages.

USDJPY

NY Open: 145.09, Overnight Range: 144.66–145.25

USDJPY drifted higher overnight, supported by improved risk sentiment from the China/US trade discussions and higher US 10-year Treasury yields. The Japanese PPI Index rose 3.2% y/y in May compared to the forecast for a 3.5% increase and 4.1% in April.

AUDUSD

NY Open: 0.6514, Overnight Range: 0.6498–0.6532

AUDUSD remained rangebound inside yesterday’s band and was unable to make additional gains despite the apparent thaw in China and US trade hostilities. The news of a US/China trade “framework” was light on details, which encouraged traders to remain on the sidelines.

NZDUSD

NY Open: 0.6037, Overnight Range: 0.6024–0.6062

NZDUSD had an uninspiring session and traders failed to be inspired by the news of a US/China “framework” on trade. New Zealand visitor arrivals data came in at a 2½-year low, which ASB Bank notes coincides with lacklustre domestic demand and suggests that the RBNZ will cut the OCR rate by 25 bps in August and October.

USDMXN

NY Open: 19.0281, Overnight Range: 19.0277–19.0745

USDMXN extended losses in early NY trading and touched 19.0093, with selling pressure stemming from reports that the US and Mexico are discussing steel and aluminum tariffs. A Reuters article claims that Mexico is close to achieving zero tariffs on a fixed quota of steel, then face a 50% tariff on any excess. Industrial output rise 0.1% m/m in April, compared to -1.2% in March.

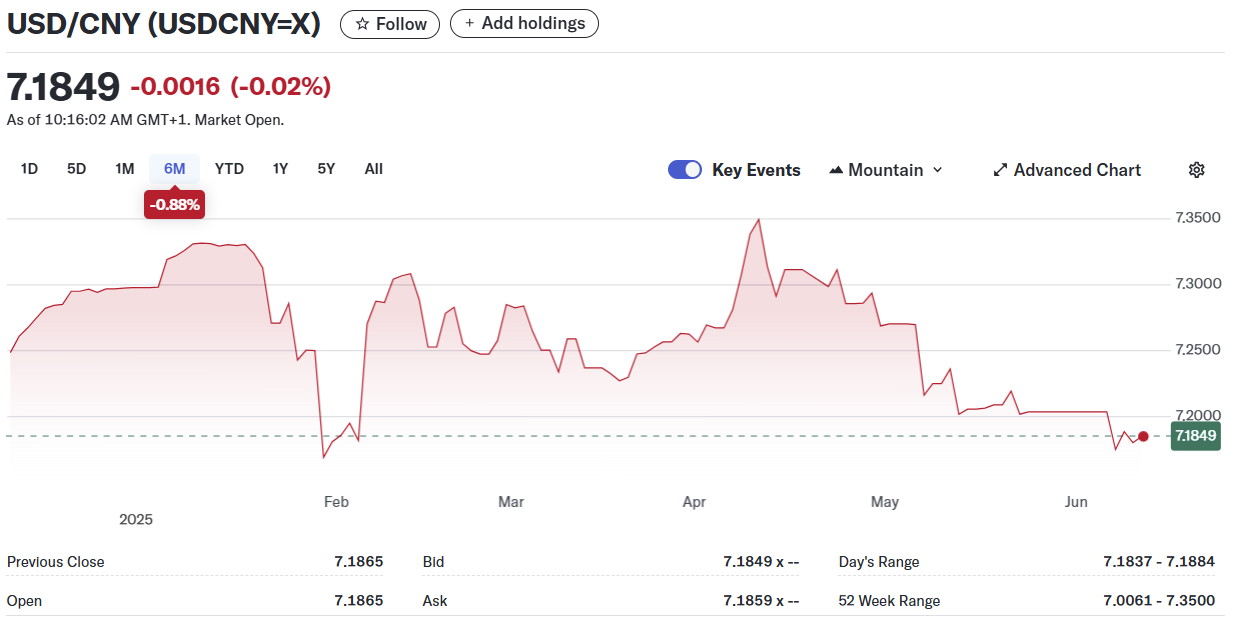

China

PBoC fix: 7.1815 vs exp. 7.1801 (Prev. 7.1840)

Shanghai Shenzhen 300 rose 0.75% to 3894.63

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.

–