June 13, 2025

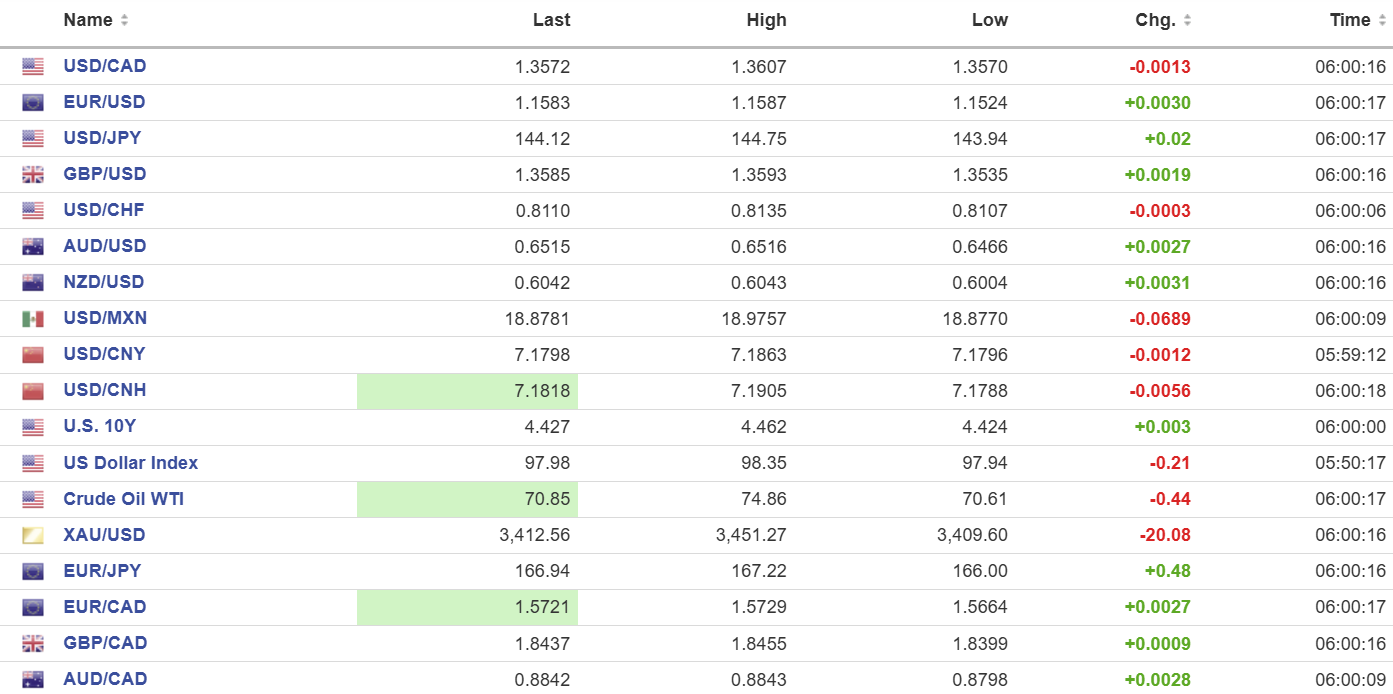

USDCAD: open 1.3572, overnight range 1.3559-1.3607, close 1.3582

USDCAD slid on Friday due to earlier soft US economic data reports, stop-loss selling following chunky option expiries in the 1.3590-00 area, and surging oil prices. It recouped some of those losses overnight as oil prices eased, but USDCAD continues to trade with a negative bias.

USDCAD is vulnerable to Canada/US tariff announcements from the Kananaskis G-7. There is speculation that Carney and Trump will announce some deal on tariffs, although Trump does not seem to be inclined to scrap levies on steel and aluminium.

WTI oil spiked to 77.62 last week when Israel bombed Iran, but prices have eased from that peak and are trading at 70.79 in NY. The oil price rally has underpinned USDCAD to a degree after the Carney government appears to be backtracking on the previous government’s anti-oil policies.

Canada May housing starts was flat (0.8%) in May (243,407 units), according to Canada Mortgage and Housing Corporation (CMHC).

US Empire State manufacturing index are on tap.

USDCAD Technicals

The intraday USDCAD technicals are bearish following the break of support at 1.3590 on Friday, but momentum indicators are at extreme oversold levels suggesting USDCAD is vulnerable to a bounce to 1.3650.

The medium-term technicals are bearish, but the decisive move below the 78.6% Fibonacci retracement level targets the 100% level at 1.3430.

For today, USDCAD support is at 1.3550 and 1.3510. Resistance is at 1.3620 and 1.3650.

Today’s Range: 1.3550–1.3650

Chart: USDCAD daily

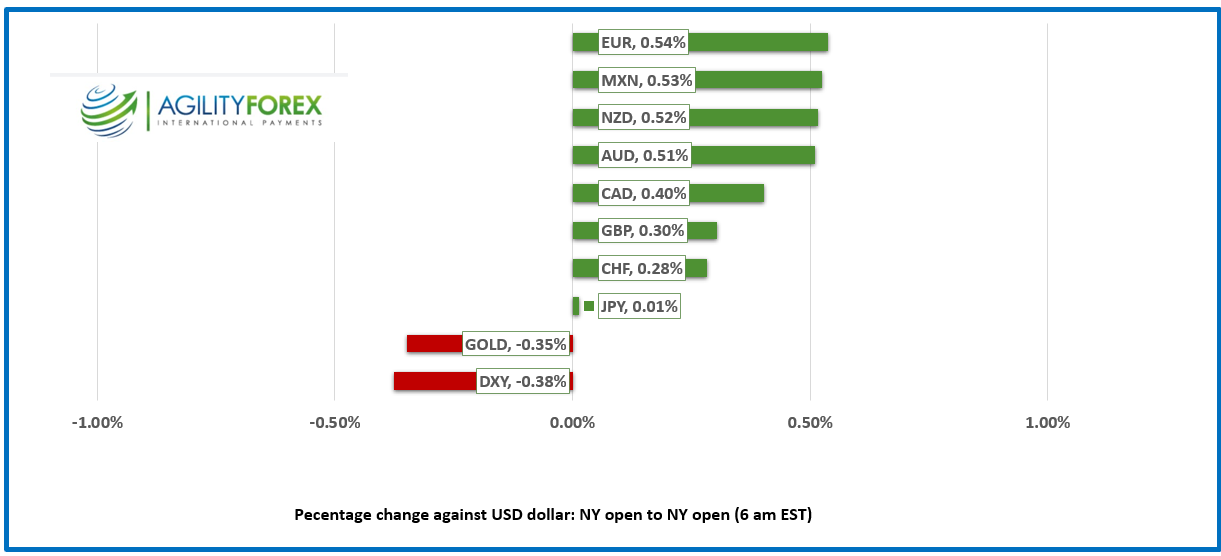

FX at a Glance

Trump vs G-7

The leaders of the G-7 have gathered in the foothills of the Canadian Rocky Mountains for the annual world-problem solving bun-fest. The top of the agenda is the Israel/Iran War, tariffs and stroking Trump. The US President reportedly vetoed Israeli plans to assassinate Iran’s leader, Ayatollah Khamenei, partly because he (and his 200-plus security team) did not want to give anyone ideas.

The meetings are not expected to result in anything more than indigestion because Trump opposes everything the other leaders support. All the leaders, except Trump, support Ukraine, while Trump believes Russia is the victim. Trump has declared economic war on every country whose leader is attending the Kananaskis summit.

And Trump is loving every minute of it. For the former reality TV star, a G-7 is his Oscars moment.

Global Stocks Drift Higher

The world is still turning and that was enough for equity optimism to return. The major Asian equity indexes closed with gains led by a 0.75% rise in Japan’s Topix. Hong Kong’s Hang Seng gained 0.70% while Australia’s ASX 200 was flat.

European bourses are firmer, led by the French CAC 40 index which has climbed 1.00% and the UK FTSE 100 index which has risen 0.45%. S&P 500 futures are up 0.68% and the US 10-year Treasury yield is 4.43%. Gold (XAUUSD) is off its recent peak and is sitting at 3413.72 as of 5:30 AM PDT.

EURUSD

NY Open: 1.1583, Overnight Range: 1.1524-1.1587

EURUSD is trading with a modestly bullish bias as it consolidates last week’s gains. Traders are biding their time and awaiting news from the G-7 while keeping an eye on oil prices and the Russian/Ukraine and Israel/Iran wars. ECB policymaker Luis de Guindos seemed rather blasé about tariffs and the recent bout of euro strength. On the inflation target, he said “The risk of undershooting is very limited in my view.” S&P reaffirmed Germany’s triple A credit rating.

GBPUSD

NY Open: 1.3585, Overnight Range: 1.3535-1.3593

GBPUSD is grinding higher with its uptrend from mid-April intact while prices are above 1.3490. Traders ignored the UK Rightmove House Price Index data (actual -0.3%, previous 0.6% m/m) and remained cautious due to geopolitical issues. Thursday’s Bank of England meeting is shaping up to be a non-event as rates will be left unchanged and no new forecasts will be released.

USDJPY

NY Open: 144.12, Overnight Range: 143.94-144.75

USDJPY remained choppy but rangebound due to shifting US Treasury yields and rising oil prices. Traders are awaiting the results of the Bank of Japan monetary policy meeting tomorrow which has the potential to impact global markets. No change in rates is expected but traders will be on alert for fresh guidance on interest rates and changes in its monthly JGB purchasing policy.

AUDUSD

NY Open: 0.6515, Overnight Range: 0.6466-0.6516

AUDUSD bounced erratically inside the well-defined range that has contained prices since the beginning of the month. The lack of follow-through safe-haven demand from the Iran/Israel war underpinned prices.

NZDUSD

NY Open: 0.6042, Overnight Range: 0.6004–0.6042

NZDUSD recouped some of Friday’s losses in a quiet session with traders awaiting news from the G-7. Prices were marginally supported by the better-than-expected China retail sales data.

USDMXN

NY Open: 18.8781, Overnight Range: 18.8770–18.9757

USDMXN continues to be pressured by broad-based US dollar weakness and hopes that the US and Mexico will reach an agreement on tariffs. President Claudia Sheinbaum is expected to meet with Trump at the G-7.

China

PBoC fix: 7.1789 vs exp. 7.1854 (prev. 7.1772)

Shanghai Shenzhen 300 rose 0.25% to 3873.80

May House Prices -3.5% y/y (Prev. -4.0%), Industrial Output 5.8% y/y (forecast 5.9, previous 6.1%)

May Retail Sales 6.4% y/y (forecast 5.0%, previous 5.1%)

ING economists suggest that the data leaves the economy on track to meet its target for H1 GDP.

Premier Li Qiang reaffirmed China’s goal of halting the decline and stabilizing the property market.

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.

–