June 17, 2026

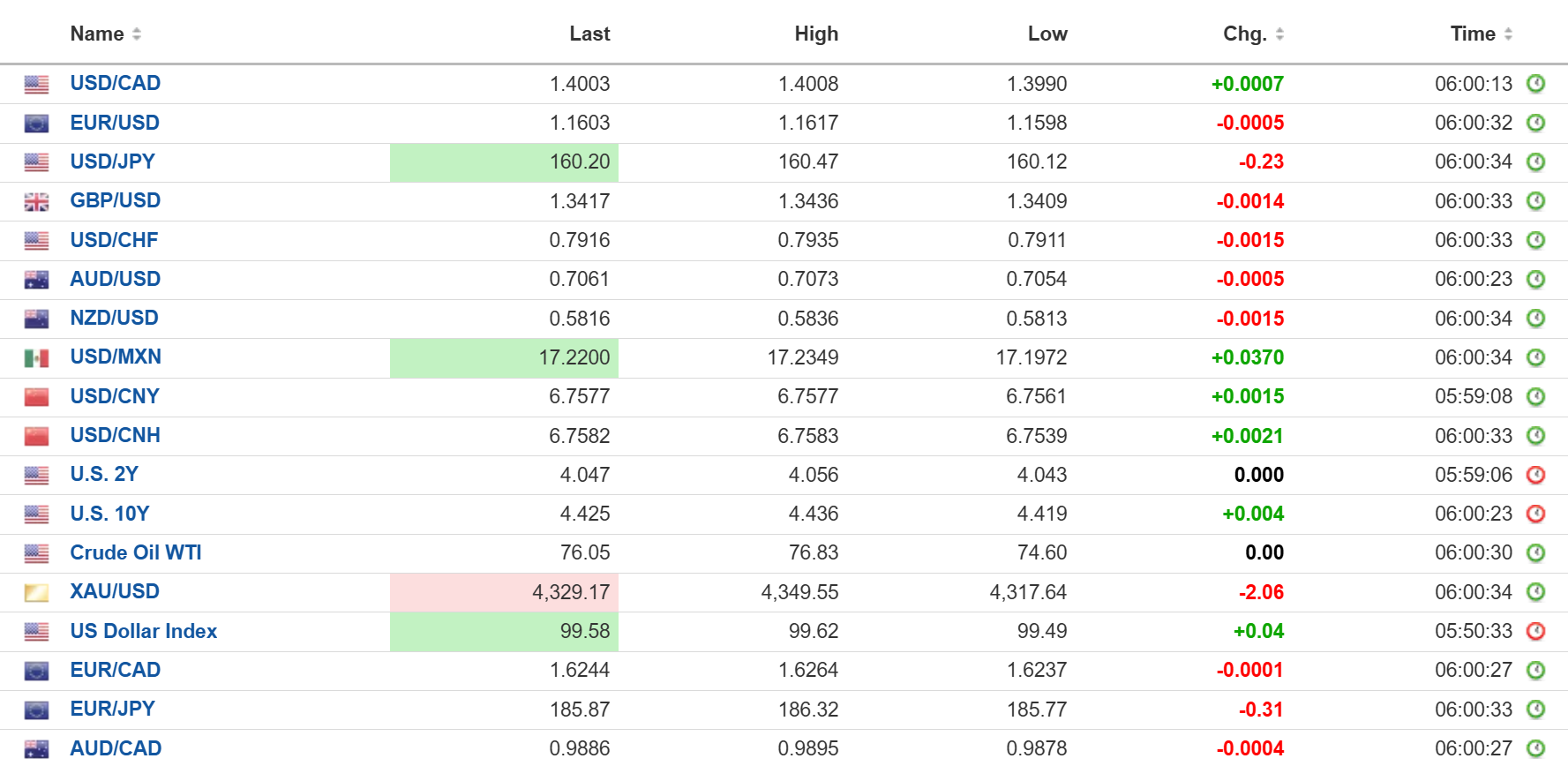

USDCAD open: 1.4003, overnight range 1.3990-1.4017, close 1.3997

USDCAD drifted aimlessly due to the elevated level of uncertainty surrounding today’s FOMC meeting then drifted higher in early NY trading. That move came on the heels of a hotter than expected Retail Sales number (actual 0.8% m/m (forecast 0.5, vs April 0.7%) which reinforces the resilient US economy story.

It is Kevin Warsh’s first as chair and since he is Trump’s pick, analysts are wondering if he will use today’s press conference to set the stage for lower rates in the future. However, recent comments by FOMC members suggest a hawkish bias in the statement.

WTI oil prices traded in a 74.60-76.83 range and are scraping the bottom of its recent range. The slide is because the US will allow Iran to sell oil immediately. In addition the International Energy Agency (IEA) is forecasting a significant oil surplus in 2027 as the world slowly recovers from the closure of the Strait of Hormuz.

Canada New House Price index fell 0.3% (forecast 0.5%). Still to come: US Business Inventories and Pending Home Sales.

USDCAD Technical Outlook

The intraday technicals are bullish above 1.3970 but the rally has stalled below 1.4025. The 4-hour chart shows USDCAD pinned near the upper 3rd SD Bollinger Band at 1.4023 after pushing to fresh highs. The 4-hour RSI and the MACD are signalling that USDCAD is consolidating its gains rather than extending. A break below 1.3970 targets the rising channel support near 1.3905, with the 100-period moving average at 1.3848 beneath that.

Longer term, USDCAD is bullish above 1.3810, the 200-day moving average, with the ascending channel from the May low still firmly intact. The daily MACD confirms the bullish bias, but the daily RSI is once again extremely overbought. As long as channel support holds, the uptrend targets the upper daily Bollinger Band at 1.4050.

For today: USDCAD support is at 1.3970 and 1.3910. Resistance is at 1.4030 and 1.4050. Today’s expected range is 1.3960-1.4030.

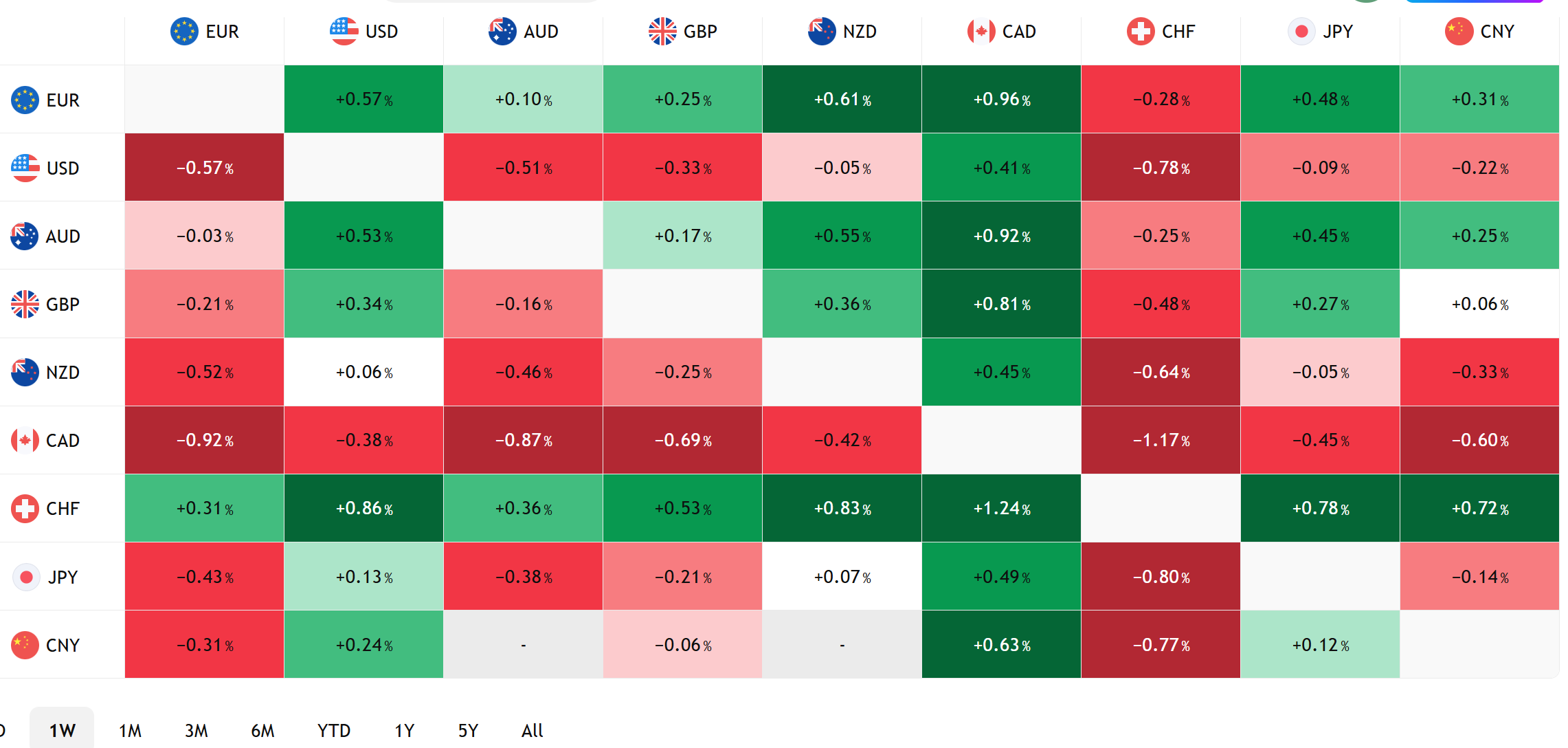

FX Heat Map

FX open high low 6:00 am

Schooled!-Iran Teaches Trump The Art of the Deal

The US and Iran signed a Memorandum of Understanding to end the war, and the details of that MOU clearly explain how Trump managed to bankrupt six casinos. As a manager he is a great reality TV host.

Trump is celebrating the reopening of the Strait of Hormuz, even though it was open before the war. He is also hailing a deal that gives Iran access to billions in previously frozen assets, sanctions relief, and an oil-export waiver, benefits Tehran did not enjoy before the conflict. Most remarkably, Iran never accepted Trump’s zero-enrichment demand and retains its enrichment capability. After months of war, Iran emerges with more concessions and fewer restrictions than when the fighting began. Making Iran Great Again.

Welcome Mr. Warsh

Kevin Warsh begins his reign at the top of the financial news cycle when he presides over his first FOMC press conference today. No one expects the Fed to cut rates today, but in light of the Iran war ending and the plunge in oil prices, Warsh could adopt a dovish bias during the Q and A. Today’s statement includes a new Summary of Projections and many analysts believe Warsh will not participate in the dot-plot projections.

Taking Stock

Asian equity markets closed on a mixed note. Japan’s Topix rose 0.55%, the Hong Kong Hang Seng Index fell 0.74%, and the Australian ASX 200 rose 0.55%.

As of 6:40 am, the French CAC 40 has gained 0.40%. Meanwhile, the German DAX, UK FTSE 100, and S&P 500 futures are flat. The 10-year Treasury yield is 4.425%, the DXY is 99.61, and gold (XAUUSD) is 4,331.42.

EURUSD | Range 1.1585-1.1617

EURUSD price action was contained ahead of today’s FOMC meeting. Headline Core Harmonized Index of Consumer Prices (HICP) rose 2.6% y/y (forecast and previous 2.5%) which added another layer of support to the ECB decision to raise rates last week. EURUSD is getting some support from the drop in oil prices.

GBPUSD | Range 1.3400-1.3436

GBPUSD drifted aimlessly as the looming FOMC meeting overshadowed a slew of economic releases. UK headline inflation rose 2.8% y/y, unchanged from April, while Core CPI ticked up to 2.6% from 2.5% previously, but that was less than forecast. May PPI rose 8.7% (forecast 8.8%, April 7.9%) while Retail prices rose 3.1% compared to 3.0% last month. The Bank of England monetary policy meeting is tomorrow.

USDJPY | Range 160.12-160.47

USDJPY drifted down from its session peak as traders jockey for position ahead of the FOMC meeting. Analysts continue to expect a somewhat hawkish outcome to today’s FOMC which is underpinning USDJPY despite the BoJ hiking rates by 25 bp to 1.00% yesterday.

AUDUSD | Range 0.7054-0.7073

Aussie traded narrowly but with a modest bid. The RBA left rates unchanged at 4.35% but Governor Michelle Bullock delivered some rather hawkish remarks. She said that the economy faces a tough couple of years in order to bring inflation down from its current level of 4.2%.

USDMXN | Range 17.1972-17.2349

USDMXN continued to be weighed down by easing geopolitical tensions with the signing of the MOU between the US and Iran. However, the downside faces hurdles stemming from the ongoing USMCA trade talks.

CHINA

- PBoC Fix: 6.8096 vs exp. 6.7569 (prev. 6.8108)

- Shanghai Shenzhen CSI 300 rose 0.97% to 4,931.39

PBoC hinting at a shift towards an overnight interest rate policy and move away from the 7-day repo rate, which brings it closer to other central banks.

PBoC announced a new repo facility that will let foreign monetary authorities, including sovereign wealth funds obtain yuan liquidity from the PBoC. It Is also launching an off-shore yuan (USDCNH) FX trading facility in Shanghai.

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview