July 9, 2028

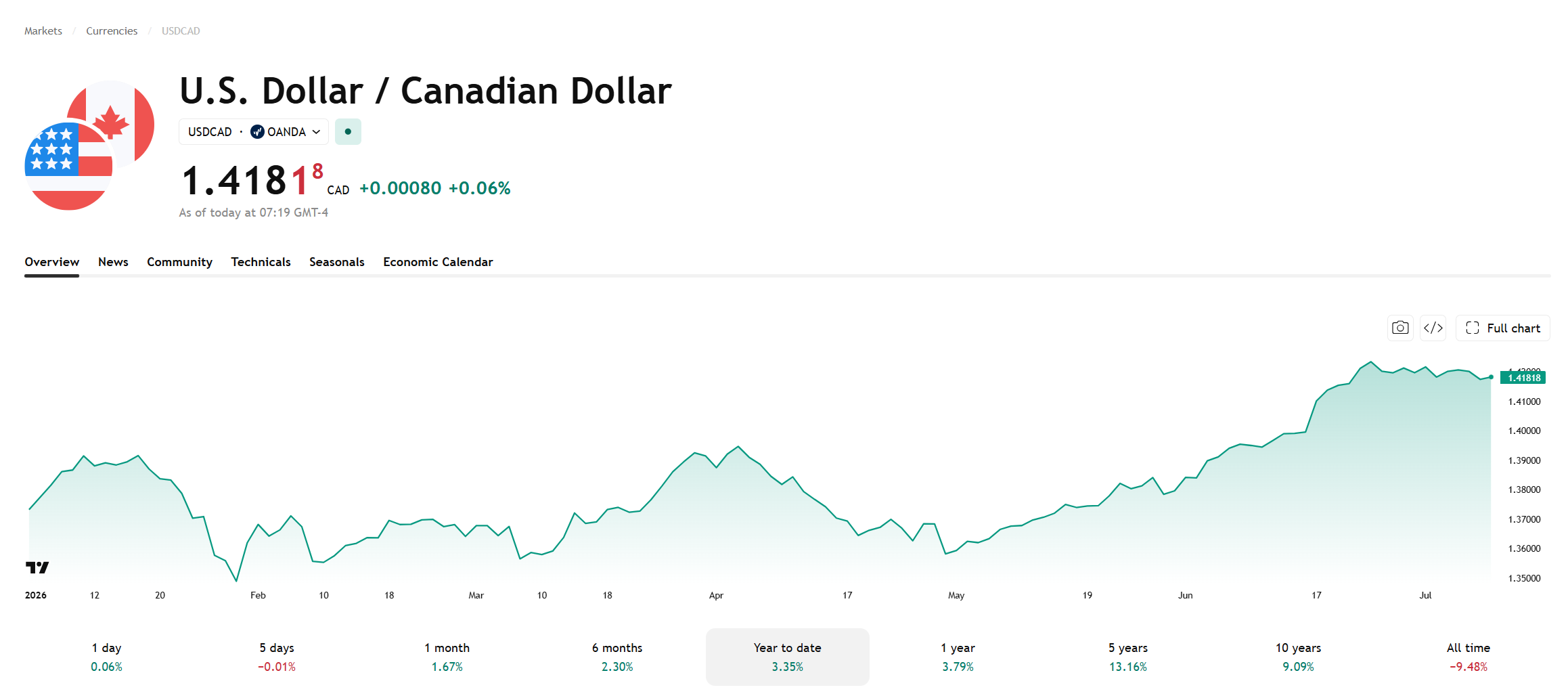

USDCAD open: 1.4179, overnight range 1.4153-1.4190, close 1.4172

USDCAD is consolidating yesterday’s losses with the move below 1.4200 keeping an intraday bearish bias to the currency pair. The FOMC minutes were not any more hawkish than previous expected which helped narrow CAD/US interest rate spreads and that weighed on prices.

WTI oil prices have ticked up modestly rising to 73.82, since touching 72.47 in Europe and the 7.43% gain in the past 5 days has contributed to the USDCAD retreat. Oil prices are underpinned by renewed Iran and US attacks. The drama has not really impacted global markets where tech and AI stock price action has garnered all the attention.

The are no Canadian economic reports on tap today.

USDCAD Technical Outlook

The intraday USDCAD technicals are little changed from yesterday. They are bearish below the 1.4200 pivot although the hourly RSI is above its moving average, suggesting sellers are losing conviction near this level. A decisive break below 1.4150 targets 1.4100, while a move back above 1.4200 shifts the focus to 1.4250.

The longer-term outlook remains bullish above 1.4150, where the ascending channel from the June low guards the broader uptrend. The daily RSI and MACD remains negative which is consistent with an ongoing correction.

For today: USDCAD support is at 1.4140 and 1.4110. Resistance is at 1.4200 and 1.4230.

Today’s expected range is 1.4140-1.4210.

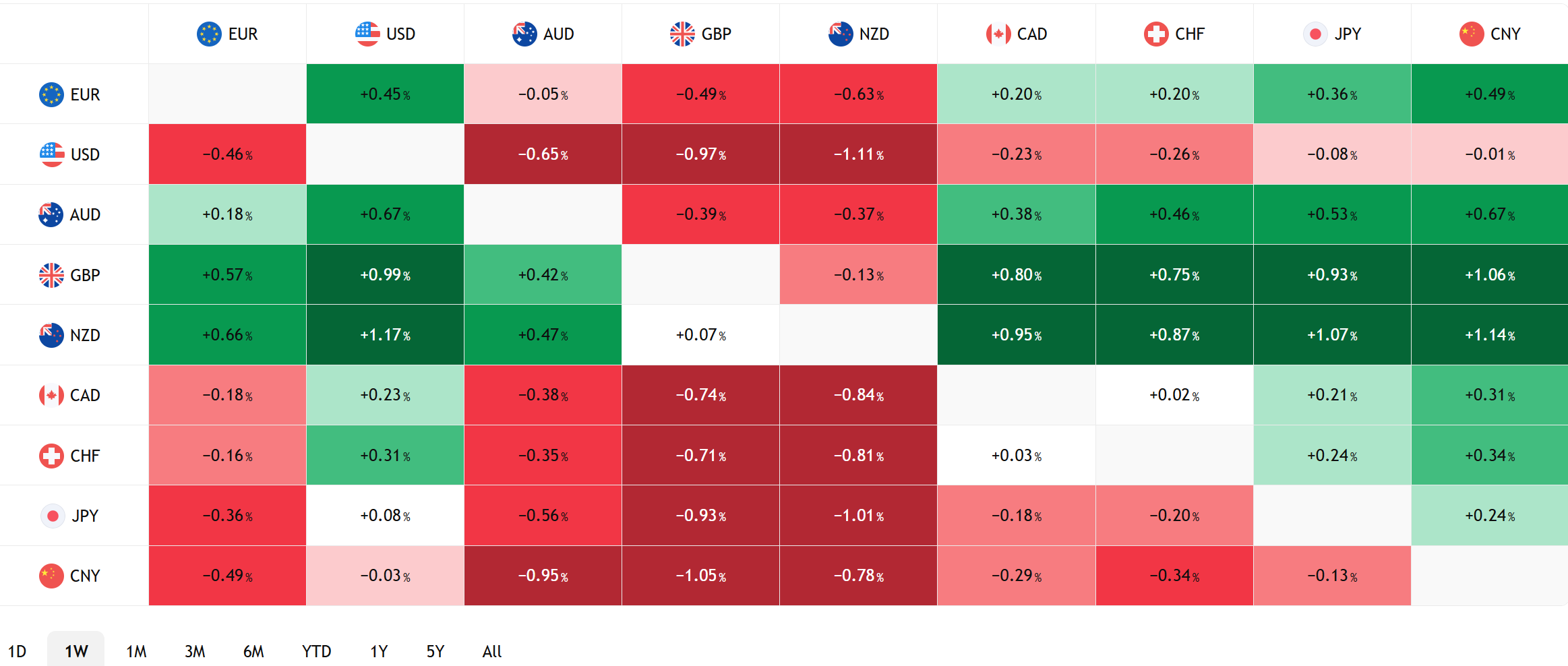

FX Heat Map

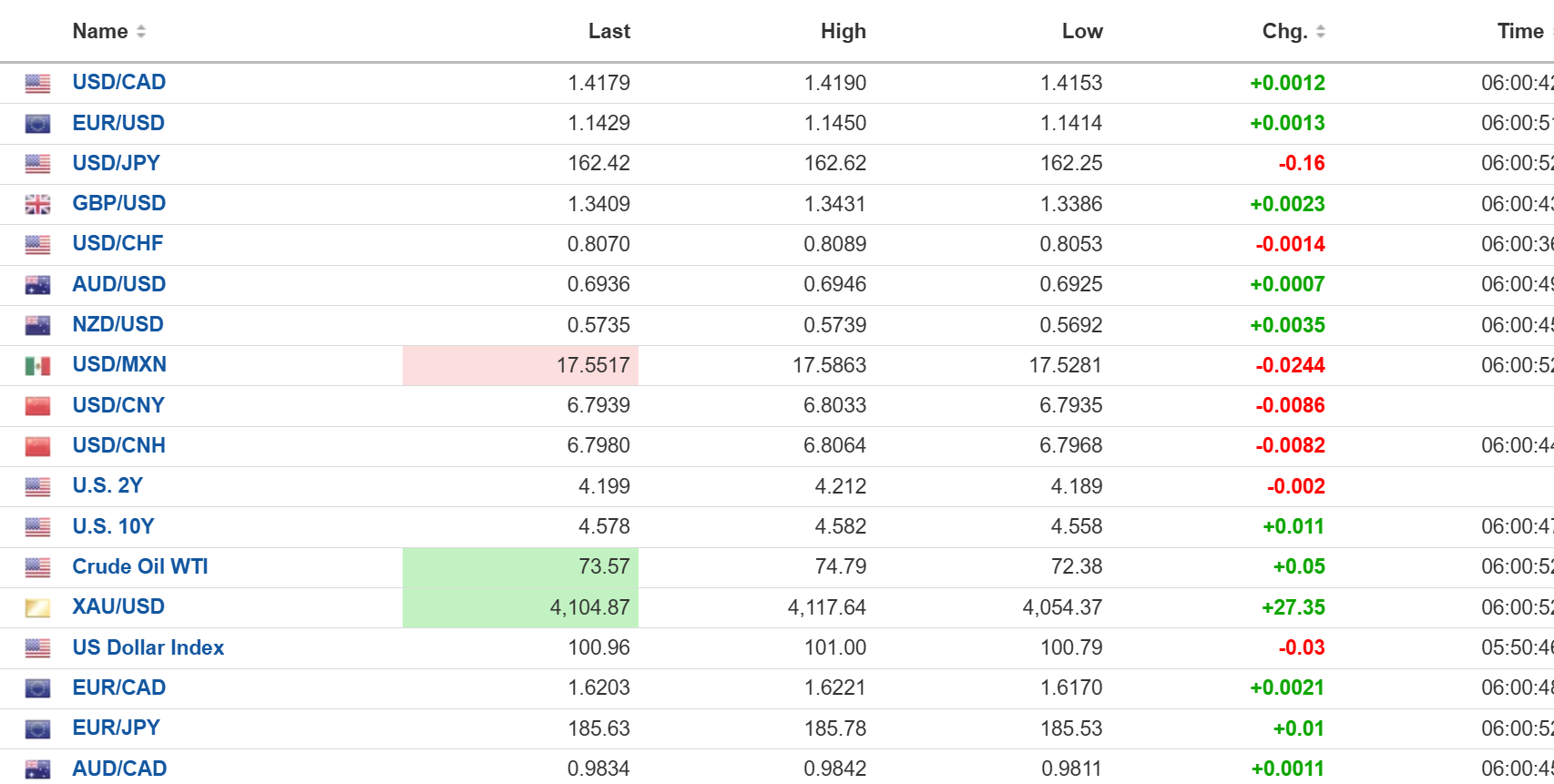

FX open high low 6:00 am

No Surprise from FOMC Minutes

The FOMC minutes came and went, and when the dust settled following the initial knee-jerk reactions, markets were left relatively unchanged. The minutes revealed that rates could go higher if inflation remains stubbornly high, or rates could be cut if inflation eases. Nothing new there.

Todays weekly jobless claims were 215,000 (forecast 218,000 , last week 217,000.

Trump Turns NATO Summit into the Donnie Show

Trump’s bipolar personality was on full display in Ankara. He kicked off his tour by reopening the Greenland annexation can of worms, but then seemed to forget it. The US president berated delegates for failing to support his war with Iran, complaining that Britain only offered to help after the fighting was over while France was of no help at all. Yet, just a few hours later, he told reporters there was “tremendous love in the room.” He completely misread the mood. What he took for “love” was really a collective hope that he would simply leave.

Meanwhile, the US attacked Iran for the second consecutive day and Iran retaliated by striking at US military bases in Kuwait and Bahrain. Traders mostly ignored the news, viewing it as a regional issue, and the specter of Iran and US hostilities was already baked into crude prices.

Taking Stock

Asian equity indexes closed with Japan’s Topix gaining 0.35%, while Australia’s ASX 200 lost 0.26% and Hong Kong’s Hang Seng fell 0.70%.

As of 7:15 am, the German Dax is flat, the French CAC is up 0.24%, while the UK FTSE 100 has dropped 0.76%. S&P 500 futures are close to unchanged; the 10-year Treasury yield is 4.589%, the DXY is 101.01, and gold (XAUUSD) is 4,103.14.

EURUSD | Range 1.1414-1.1450

EURUSD inched higher on renewed speculation that the ECB would raise rates as early as September. Prices got some additional support after oil prices slipped from yesterday’s peak. However, the ECB rate hike story is stale while there is a lot of shelf-life left in the Fed rate hike narrative, which may cap EURUSD gains in the near term. EURUSD technicals are bearish below 1.1500.

GBPUSD | Range 1.3385-1.3431

GBPUSD caught a bid from the renewed Iran-US hostilities and the inflammatory rhetoric from both sides. Steady to higher oil prices could force the Bank of England to hike rates, but ongoing political uncertainty may limit gains. Andy Burnham has already been anointed the next UK Prime Minister and will likely take office on July 30. A committed socialist, he has never met a taxpayer’s pound that wouldn’t be better spent by the government.

USDJPY | Range 162.25-162.62

USDJPY continued to trade with a bid after the FOMC minutes failed to dissuade many of the Fed’s hawkish bias. Steady to firm oil prices, and Japanese government fiscal policies, more than offset intervention risks.

AUDUSD | Range 0.6906-0.6947

The Australian dollar drifted higher and attempted to claim the peaks seen after the weak US NFP report last Friday. The rally was supported by the lack of any surprises from the FOMC minutes and hawkish comments from RBA officials earlier this week.

USDMXN | Range 17.5281-17.5863

USDMXN released from yesterday’s 17.6422 peak due to improved risk sentiment stemming from a lack of escalation in the ongoing Iran-US conflict. Mexican headline inflation fell 0.27% m/m in June, deeper than forecast, pulling the annual rate down to 3.37% versus the 3.52% consensus, while core inflation held steady at 0.24% m/m, just below expectations.

The faster-than-expected cooling in headline inflation alongside contained core price pressure gives Banxico more room to keep cutting rates.

The minutes from the recent Banxico meeting are released this afternoon

CHINA

- PBoC Fix: 6.8036 (prev. 6.8077)

- Shanghai Shenzhen CSI 300 rose 2.54% to 4,876.31

June CPI fell 0.3% m/m (forecast -0.2%, May -0.1%, Annual CPI rose 1.0%, (forecast 1.1%, May 1.2%). June PPI rose4.1% /y, as expected. It is the highest reading since 2022.

The CSI 300 soared due a mix of dovish signals from PBoC and a bounce in chipmaker stocks

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics, Tradingview