September 19, 2025

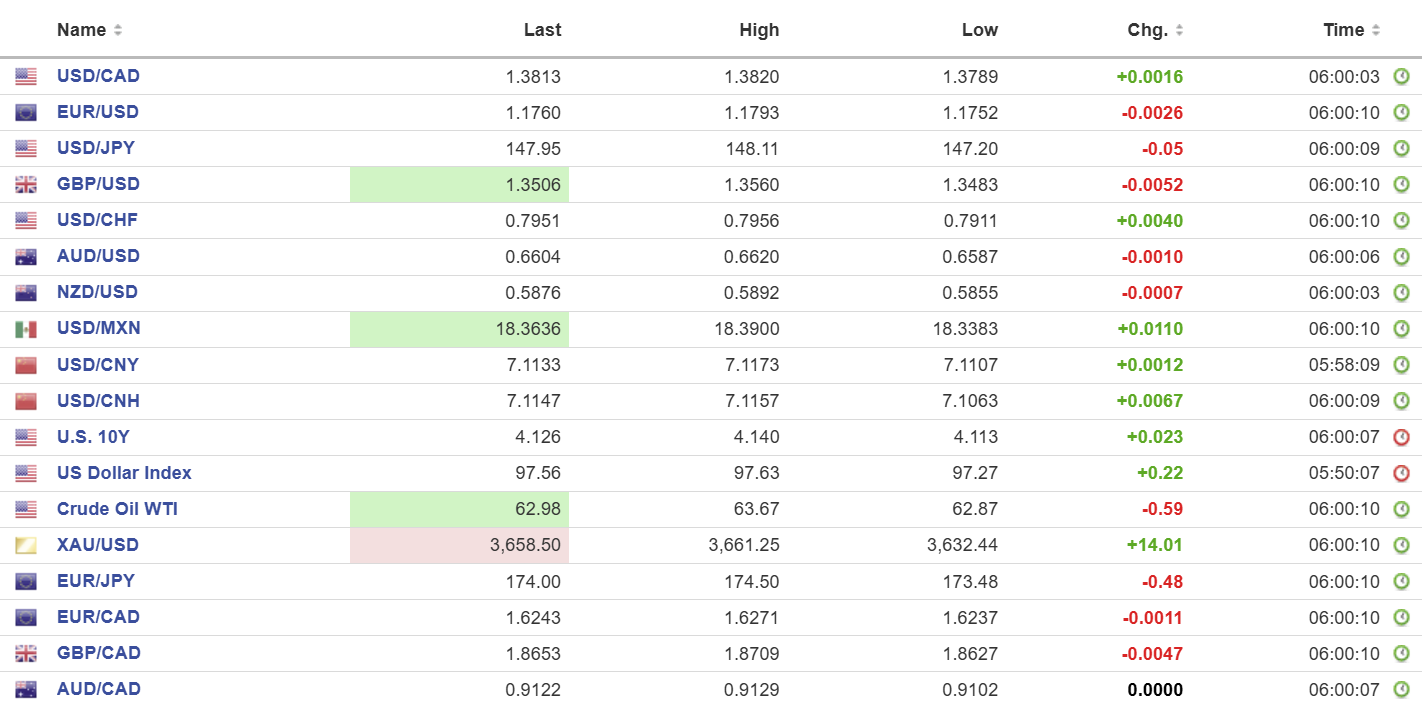

USDCAD open 1.3813, overnight range 1.3789-1.3823, close, 1.3797

The USDCAD focused quickly shifted from the Bank of Canada to the Fed and the outlook for interest rates on Wednesday. The Fed rate cut was partly due to a faltering employment market, but that notion was disabused yesterday with the weekly jobless claims and Philly Fed data. USDCAD caught a bid and blew through stops in the 1.3780 area with prices consolidating the gains overnight.

Prices bounced from 1.3810 to 1.3823 after July Retail Sales-ex-autos fell by 1.2% which was more than the expected 0.7% decline and well below the 2.0% m/m increase in June. The advance Retail sales projection for August is for a rise of 1.0%.

Prime Minister Carney met with Mexican President Claudia Sheinbaum yesterday and they agreed to close coordination in upcoming negotiations of the pending US-Canada-Mexico trade pact.

USDCAD is expected to test support in the 1.3770-80 level today, partly because there are at least $1.3 billion of 1.3785-1.3800 option strikes rolling off at 10”00 am EDT.

WTI oil prices traded in a 62.84-63.87 range as they continued to slide after peaking at 64.75 on Tuesday, although they are still higher then they were last Friday. Prices are trading defensively despite the 9.285-million-barrel drop in US crude inventories last week.

There are no US economic report of note today.

USDCAD Technical Outlook:

The intraday technicals are mildly bullish above 1.3770 but the failure to break above 1.3820 risks a drop to 1.3770, which if broken targets 1.3730. A break above 1.3820 targets 1.3860 then 1.3900.

The medium-term technicals suggest that the break above the 100-day moving average at 1.3762 puts the 200-day moving average at 1.4002 in play. However, the medium-term bias is negative while trading below 1.3960 which is guarded by 1.3950, the 61.8% Fibonacci level of September 2024-February 2025 range.

For today, USDCAD support is 1.3770 and 1.3740. Resistance is 1.3820 and 1.3850. Today’s Range: 1.3760-1.3850.

Greenback Rallies

The FOMC cut rates because President Trump wanted them to. No, that’s not true. They said the rates were lowered because “job gains slowed and the unemployment rate edged up.” Yesterday’s weekly jobless claims data and the Philadelphia Fed Manufacturing Survey suggested that the employment picture may not be all that weak. The surge in weekly claims in the prior week was reportedly due to employment fraud in Texas. The Manufacturing survey reported that “the employment index remained mostly unchanged and continued to reflect overall increases in employment.”

The US dollar caught a bid and rallied across the board. However, there was likely an element of short-squeezing involved as prior to the FOMC meeting, many traders were hoping for a far more dovish outcome than what occurred.

Taking Stock

Asian equity indexes closed mixed. Japan’s Topix dropped 0.35% following the BoJ decision while Australia’s ASX 200 followed Wall Street’s lead and rose 0.32%. The Hong Kong Hang Seng closed unchanged.

As of 7:30 am EDT, European equities are mixed. The French CAC 40 is up 0.22%. The DAX has shed 0.22%, while the UK FTSE 100 and S&P 500 futures are flat. The US Dollar Index (DXY) is 97.60, Gold is 3649.15 and the US 10-year Treasury yield sits at 4.138%.

EURUSD

EURUSD traded sideways in a 1.1752-1.1793 range due to broad-based US dollar strength and a lack of EU-specific drivers. Traders remain cautious around French politics and the sting of the Fitch downgrade of French debt a week ago still lingers. The EURUSD uptrend remains intact while prices are above 1.1750.

GBPUSD

GBPUSD is having another bad day, falling from 1.3560 to 1.3483 before grinding back to 1.3505. Traders were blasé following the BoE monetary policy meeting. Policymakers left rates unchanged and were ambivalent to further rate cuts. This morning UK debt woes took center stage after the Office of National Statistics (ONS) reported “Public sector net borrowing excluding public sector banks was £18.0 billion in August 2025.” From April to August, borrowing now totals £83.8bn, £16.2bn more than in the same five-month period of 2024. The light at the end of the tunnel is UK Prime Minister Keir Starmer wrangled US investment and new partnership agreements with Trump. Better-than-expected UK Retail Sales data was overshadowed by the news on borrowing. The GBPUSD medium-term uptrend remains bid while prices are above 1.3420.

USDJPY

USDJPY is consolidating its post-FOMC gains in a 147.20-148.11 range. The low was seen after the Bank of Japan left rates unchanged but with two members voting for a 0.25% rate hike due to rising inflation. Markets were also surprised with the announcement that the BOJ would begin selling its massive ETF and REIT holdings to the tune of Yen 330 billion/year. At that rate it would take over 100 years to sell them all.

AUDUSD

AUDUSD traded in a 0.6587-0.6620 range as it continued its post-FOMC slide due to renewed US dollar demand after yesterday’s weekly jobless claims.

USDMXN

USDMXN traded sideways in a 13.3383-13.3900 band but has a bearish bias while trading below 18.5100, a level guarded by resistance at 18.4250. USDMXN remains pressured by Mexican and US interest rate differentials.

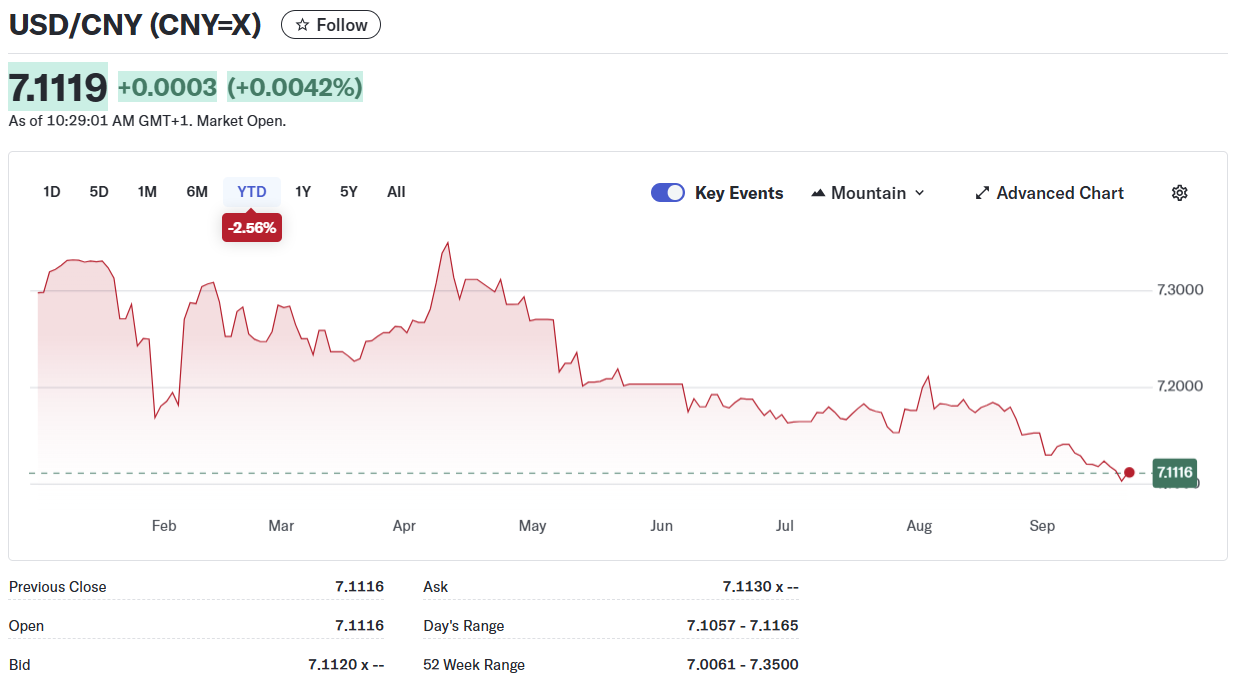

USDCNY

PBoC fix: 7.1128 vs exp. 7.1174 (Prev. 7.1085).

Shanghai Shenzhen CSI 300 rose 0.08% to 4501.92.

President Trump and Xi Jinping are speaking today and are expected to discuss the sale of TikTok, and an agreement is seen as a prelude to improving trade negotiations.

There is ongoing speculation that China’s US Treasury-selling program is transferring proceeds to EU assets and gold. Bloomberg reports that China’s July Treasury holdings were at the lowest level since 2009. The sales are meant to counter fears that the US is weaponizing the US dollar.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics