November 13, 2025

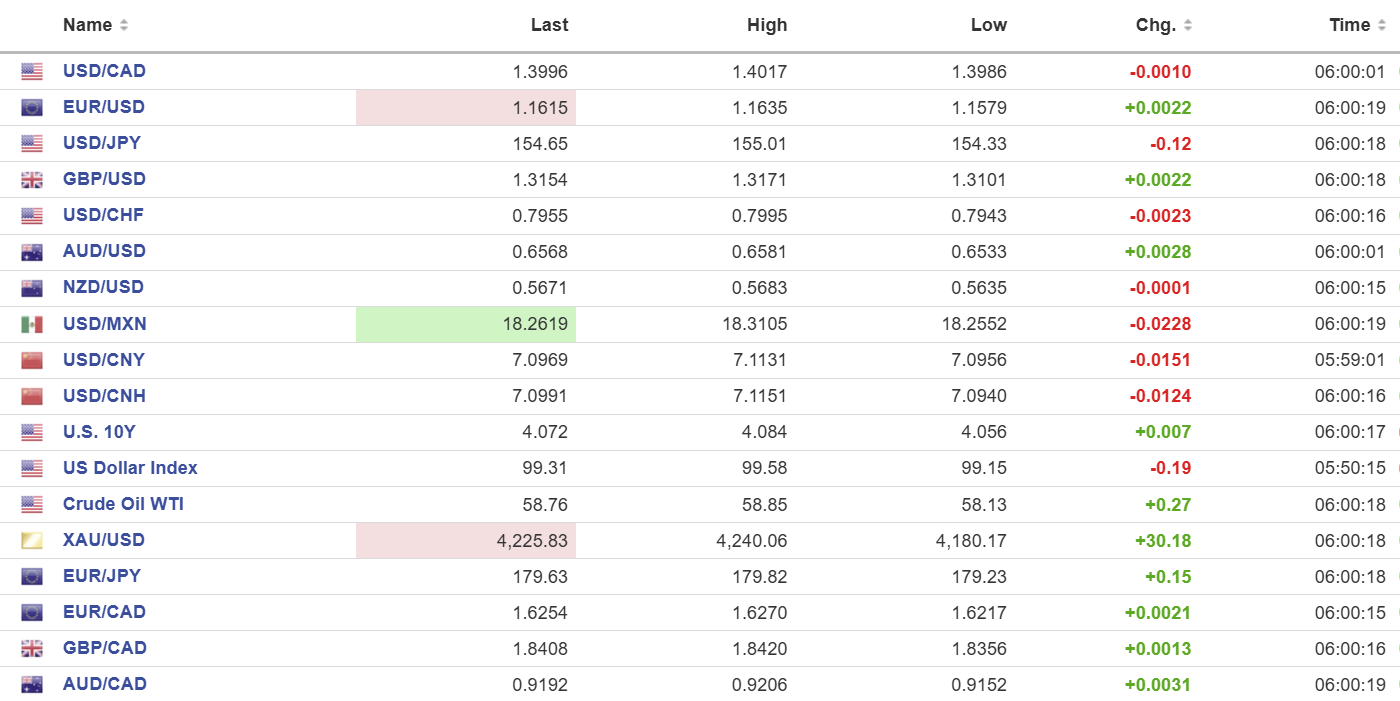

USDCAD open: 1.3996, overnight range 1.3986-1.4017, close, 1.4007

USDCAD is trading defensively on the back of broad-based US dollar selling pressure following the news that the US government shutdown has ended. However, the CAD gains lagged those of AUD and NZD, due to the ongoing US and Canada trade war, a sluggish domestic economy, weakening oil prices, and a government still fixated on hiking carbon taxes.

USDCAD direction remains at the mercy of prevailing US dollar sentiment and although the government is reopening, it will take a while for accurate economic data to start flowing.

WTI oil is at the top of its 58.13-58.90 range with prices pressured by the latest International Energy Agency (IEA) report warning of an oil surplus of over 4.0 million barrel/day in 2026. Canada’s largest oil export is Western Canada Select (WCS) and it is trading at $12.76 discount to WTI today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish while trading below 1.4030, and has room to extend toward the 1.3975 area and the heavier support band created by the 200-day MA at 1.3935. However, momentum indicators are approaching oversold levels which may act as a drag on the downside. A move above 1.4030 negates the negative pressure.

The medium term uptrend remains bullish as long as USDCAD holds above the 1.3840 to 1.3940 support zone 100-day MA (1.3835), and the 200-day MA (1.3945). This area has repeatedly contained corrective dips and preserves the medium-term pattern of higher lows. A sustained move above 1.4100 would target the 1.4180–1.4250 area.

For today, USDCAD support is at 1.3980 and 1.3954. Resistance is at 1.4020 and 1.4050.

Today’s Range: 1.3960-1.4020.

Trump Signs Bill to Reopen Government

The 43-day US government shutdown ended last night when the Democrats posted 20,000 of Jeffrey Epstein’s emails. No, it didn’t that was just a coincidence. The shutdown ended when President Trump signed the new spending bill. But it is too late for major October economic data like CPI and nonfarm payrolls reports. The September NFP data will get released but October’s may never be.

Nevertheless, it was good news for stocks and bad news for the greenback and a tad embarrassing for Trump.

Most Fed Officials Sound Hawkish

Bank of Boston Fed President Susan Collins said she is unlikely to vote for another rate cut this year. “Absent evidence of a notable labor market deterioration, I would be hesitant to ease policy further, especially given the limited information on inflation due to the government shutdown.”

Atlanta Fed President Raphael Bostic said that labour market conditions did not warrant a rate cut and that inflation was too high. Then he announced his retirement effective February 28, 2026.

Temporary Fed Governor Stephen Miran disagreed. He said the Fed is too restrictive.

Taking Stock

Asian equity markets are mostly higher except Australia’s ASX 200 which fell 0.52% due to the robust employment report which lowered rate cut odds. Hong Kong’s Hang Seng rose 0.56% and Japan’s TOPIX gained 0.67%.

As of 75:30 am PT, European bourses are mixed. The German DAX is down 0.58%, the UK FTSE 100 has lost 0.78% while the French CAC 40 is up 0.35%. S&P 500 futures are down 0.17%, the U.S. Dollar Index (DXY) is 99.28, and the U.S. 10-year Treasury yield is 4.09%. Gold (XAUUSD) is 4225.84

EURUSD

EURUSD rallied from 1.1579 to 1.1635 then consolidated the gains into the NY open. The gains were on the back of the US government reopening news. Eurozone industrial production rose 0.2% m/m in September (forecast 0.7%, previous -1.7%) and 1.2% y/y (forecast 2.1%, previous 1.1%) with the results impacted by US tariffs.

GBPUSD

GBPUSD popped to 1.3171 from 1.3101 after the US government reopening news and remained near the session peak despite a slew of weaker-than-expected economic reports. UK Q3 GDP rose 0.1% compared to 0.3% in Q2. The UK Guardian reported ONS Director of Economic Statistics Liz McKeown saying: “Across the quarter as a whole manufacturing drove the weakness in production. There was a particularly marked fall in car production in September reflecting the impact of a cyber incident as well as a decline in the often erratic pharmaceutical industry.”

USDJPY

USDJPY dropped to the bottom of its 154.33 to 155.01 range on the US government reopening but bounced to 154.71 in NY as traders appear to defy Ministry of Finance warnings about intervention risks. Analysts are arguing that Prime Minister Sanae Takaichi’s government does not have an appetite for intervention ahead of plans for fiscal stimulus.

AUDUSD

AUDUSD traded with a bid in a 0.6533 to 0.6581 range supported by improved risk sentiment after the US government reopened and by robust employment data. Australia added 42,200 jobs in October (forecast 20,000) and the unemployment rate dropped to 4.3% from 4.5%. The news reduced the odds for further easing from the RBA.

USDMXN

USDMXN traded lower in an 18.2150 to 18.3105 range with improved risk sentiment and MEX to US interest rate differentials fueling the retreat.

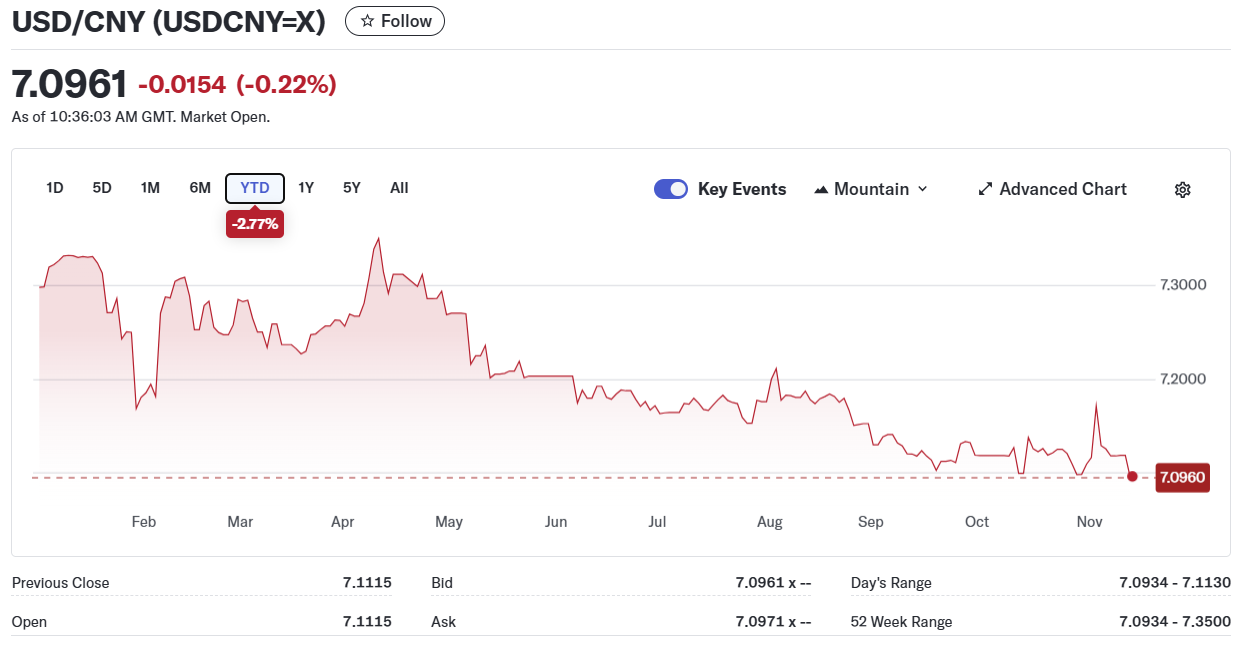

China

PBoC Fix: 7.0865 vs exp. 7.1156 (Prev. 7.0833).

Shanghai Shenzhen CSI 300 rose 1.21% to 4702.07.

China is still annoyed that Japanese Prime Minister Takaichi met with a Taiwan official. Today, China’s foreign ministry said ““If Japan dares to use military force to intervene in the Taiwan Strait, that will constitute an act of aggression, and China will strike back forcefully.”

China’s purchases of soybeans have reportedly stalled despite Trump’s claim that Beijing promised to buy 12 million tons.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics