July 23, 2025

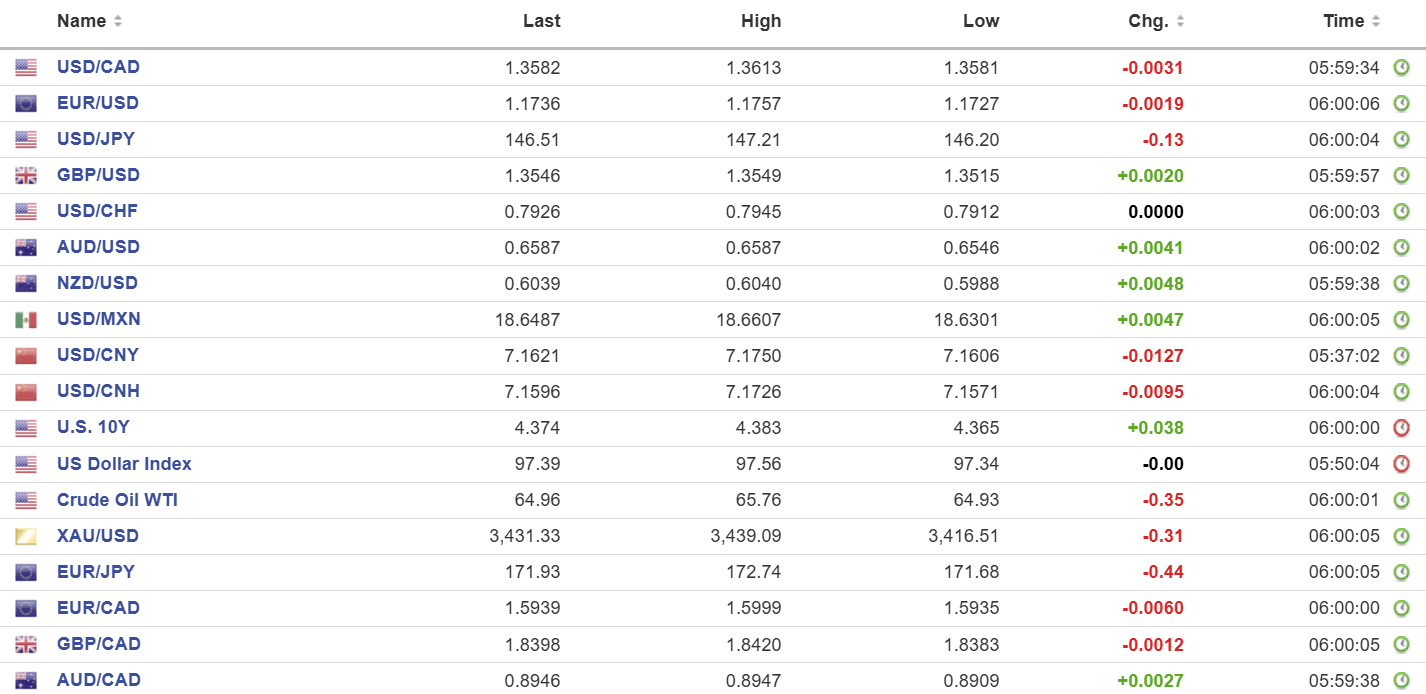

USDCAD open 1.3582, overnight range 1.3575-1.3613, close 1.3606

USDCAD dropped on broad US dollar weakness after Trump’s trade deal announcements lifted global risk sentiment. Trump raved about how he negotiated trade deals with Japan, the Philippines, and Indonesia. Can you imagine how excited he will be if he can come to terms with Mark Carney, since trade with Canada is 66% higher than that trio of Asian countries combined?

Prime Minister Carney does not seem to care about Trump’s August 1 deadline, and many, if not most, provincial premiers agree. Carney admitted that any new deal would include tariffs but said “he did not want an agreement at any cost.” Ontario Premier Doug Ford wants Carney to adopt a more aggressive stance by matching US tariffs “dollar-for-dollar.”

WTI oil is trading negatively, falling from 65.76 to 64.76 in early NYT trading before grinding back to 65.10. The promise of increased crude demand from tariff deals has offset concerns about reduced supply due to more aggressive EU sanctions on Russian crude.

Canada housing price index fell 0.2% in June, the same as in May. US existing Home sales are released later today.

USDCAD Technical Outlook:

The intraday technicals are bearish below 1.3610 and looking for a test of support in the 1.3540-50 area. A topside break should stall at resistance in the 1.3640-60 zone.

The medium-term technicals are bearish as multiple technical signals converge to point toward downside risks. Price action has been dominated by a series of lower highs and lower lows since the mid-April peak near 1.3845, and the latest breakdown below support in the 1.3660–1.3610 zone has further reinforced the negative momentum. Rallies will be corrective if they fail to break above 1.3660.

For today, USDCAD support is 1.3550 and 1.3510. Resistance is 1.3610 and 1.3640. Today’s Range: 1.3540-1.3620.

Dog Day’s of Summer Still Barking

President Trump tweets “We just completed a massive Deal with Japan, perhaps the largest Deal ever made.” And for once, Trump wasn’t exaggerating—if history began yesterday, he is 100% correct. The reality is that the Canada US Mexico Agreement on Trade (is exponentially larger and far more encompassing. Nevertheless, it was enough to inject a bit of positive sentiment into the “summer markets.” Traders are looking ahead to the Monday and Tuesday US and China trade talks in Sweden and are encouraged by Treasury Secretary Bessent suggesting that the August 1 tariff deadline may be extended.

Taking Stock

The Japan/US trade announcement fueled an Asian equity index rally led by a 3.18% auto-stock-fueled surge in Japan’s Topix. Hong Kong’s Hang Seng index rose 1.62% while Australia’s ASX 200 gained 0.69%.

European bourses are also feeling frisky. The French CAC 40 index has climbed 1.21%, the German Dax is up 0.64% and the UK FTSE 100 index has risen by 0.54%, all of which are below their peak levels. S&P 500 futures are up 0.38%. The US 10-year Treasury yield is steady at 4.37%. Gold (XAUUSD) consolidated yesterday’s gains in a 3416.51–3439.09 range as of 5:30 am PDT.

EURUSD

EURUSD is consolidating yesterday’s gains in a 1.1727–1.1757 range due to modestly improved risk sentiment due to tariff deal announcements. Traders are mostly sidelined ahead of tomorrow’s Eurozone PMI data dump and the ECB monetary policy meeting. The ECB is expected to leave rates unchanged.

GBPUSD

GBPUSD traded in a 1.3515–1.3549 range with support from renewed positive risk sentiment offset to a degree by ongoing UK debt concerns. Chancellor Rachel Reeves is feuding with BoE Governor Andrew Bailey. Ms. Reeves claims banking regulations are “a boot on the neck of businesses” while Mr. Bailey said the ring-fencing (separates banks’ consumer lending from investment banking) is necessary.

USDJPY

USDJPY bopped and weaved in a 146.20–147.21 range as traders digested the news of the latest US/Japan trade deal and rumors that Prime Minister Shigeru Ishiba would resign. The PM denied the rumours. BoJ Deputy Governor warned that monetary policy needs to remain accommodative due to uncertainty around trade.

AUDUSD

AUDUSD rallied in a 0.6546–0.6587 range due to positive developments on the US tariff front with Philippines and Japan bending the knee to Trump. More importantly, the news of another round of US and China trade talks and talk that Trump’s August 1 tariff deadline would be extended for Beijing supported the gains.

NZDUSD

NZDUSD climbed from 0.5988 to 0.6039 due to improved risk sentiment following the Japan/US trade deal news. The break above 0.5950 snapped the July downtrend and prices are targeting gains to 0.6120.

USDMXN

USDMXN drifted sideways in a 18.6301–18.6607 range. Traders largely ignored yesterday’s inflation data which came in as expected and left the door open for further Banxico easing. Prices climbed from the low after Mexico’s economy showed no growth in May 2025 (month-over-month), with services dragging while agriculture and manufacturing posted gains.

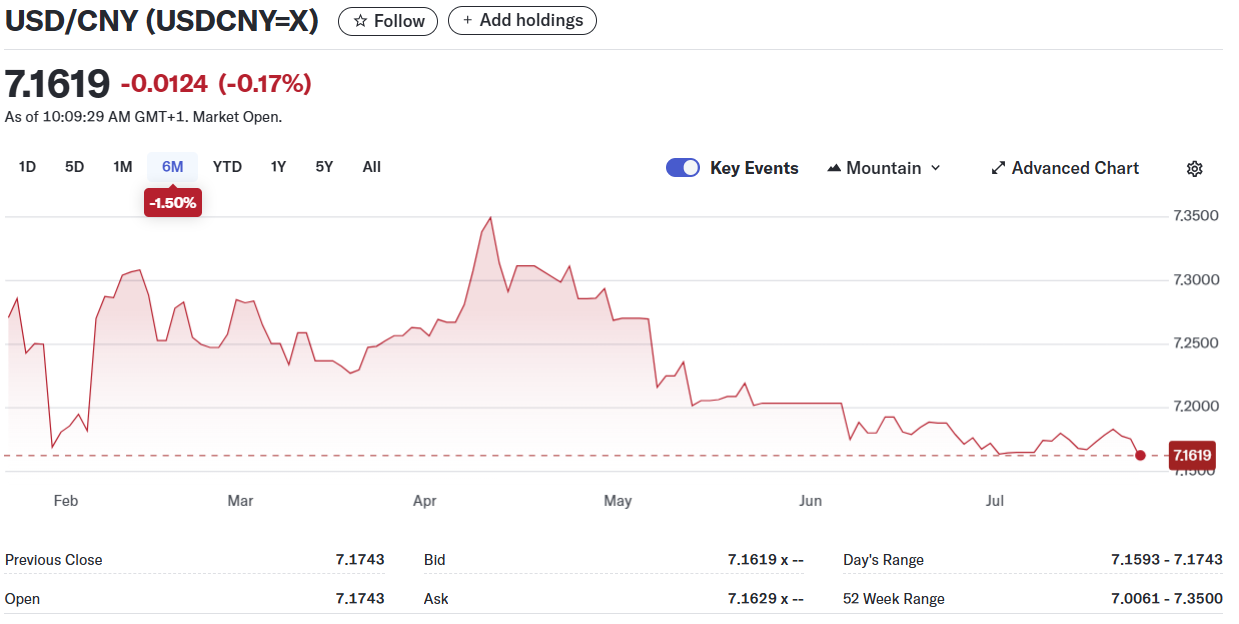

USDCNY

PBoC fix: 7.1414 vs exp. 7.1596 (Prev. 7.1460)

Shanghai Shenzhen 300 rose 0.02% to 4119.77

China’s support for Russia suggests low odds of a trade deal arising from Thursday’s EU/China meeting.

US Treasury Secretary Scott Bessent said China/US trade talks will occur in Sweden on Monday and Tuesday.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau