July 25, 2025

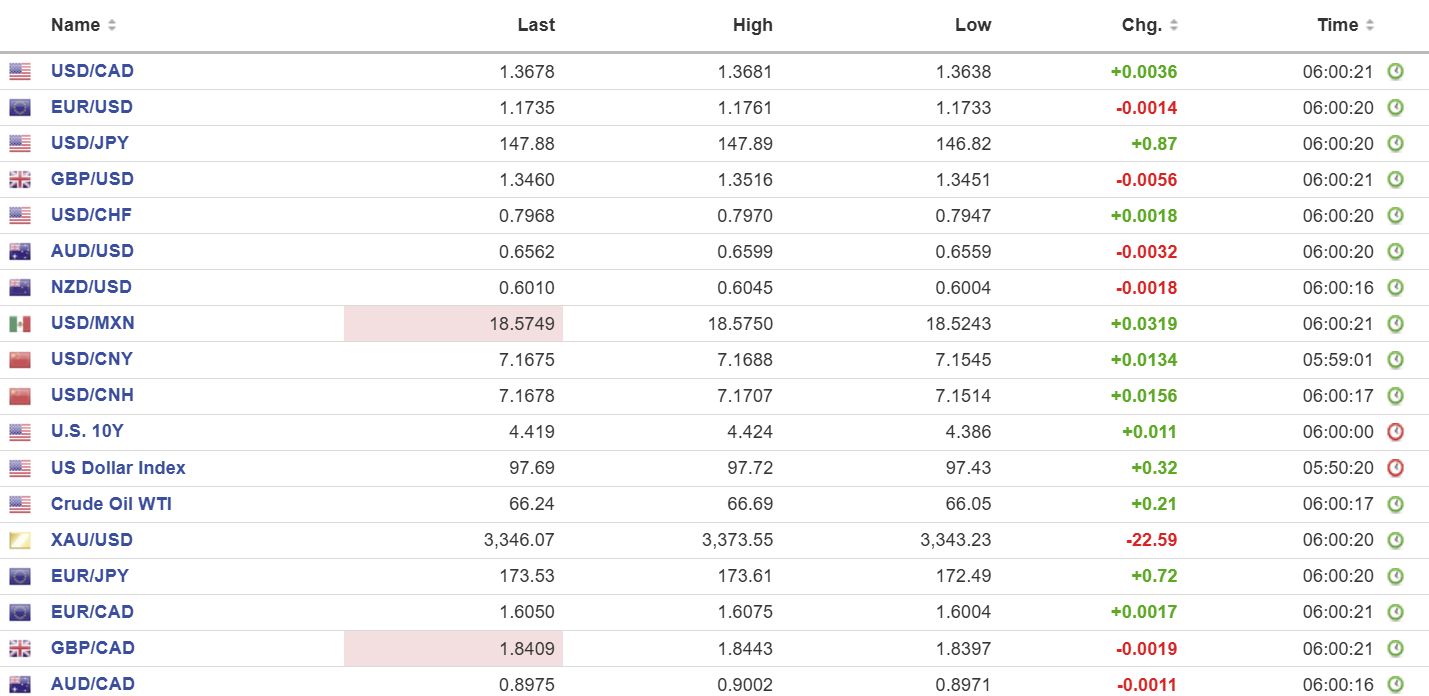

USDCAD open 1.3678, overnight range 1.33638-1.3687, close 1.3637

USDCAD extended yesterdays gains overnight on the back of broad US dollar demand with a dash of concern about the ongoing Canada/US tariff negotiations. Canada’s auto exports are at the heart of the dispute as Trump is pushing to have production moved to the US.

The Canadian government is making things worse. They remain committed to the Trudeau era mandate that 20% of all passenger vehicle sales must be zero emission by 2026 and 100% by 2035. Canadian’s do not want EV’s and the government knows it. An internal document claims hat EV sales would plummet with the removal of subsidies.

WTI oil consolidated yesterdays gains in a 66.05-66.69 range as traders felt slightly optimistic that trade deals would improve global demand for crude.

USDCAD trading could be messy around the 10:00 am EDT option expiry window. There are reportedly $1.4 billion of 1.3620-1.3630 and $940 million of 1.3600 strikes rolling off. The top side sees $1.0 billion of 1.3670-80 and $1.1 billion of 1.3700 strikes expiring.

US Durable goods orders fell 9.3% in June (-16.5% in May) and ex-transportation rose 0.2% compared to 0.6% previously

USDCAD Technical Outlook:

The intraday technicals are bullish while trading above 1.3630 and are looking for a break above 1.3700 to target 1.3750. A move below 1.3630 puts 1.3580 in play.

Longer term, USDCAD remains rangebound, trapped in a 1.3550-1.3800 band. However, the longer-term trend is bearish with the April 10 downtrend line intact while prices are below 1.3820.

For today, USDCAD support is 1.3630 and 1.3580. Resistance is 1.3700 and 1.3750. Today’s Range: 1.3630-1.3720

Powell trumps Trump

President Trump toured the Fed’s building site with the idea of embarrassing Fed Chair Jerome Powell into lowering interest rates. The Fed’s renovation project is over budget, and Trump and his cronies want to use it as an excuse to fire Powell for cause. Of course, all the problems go away if the Fed cuts rates. Trump, playing to the media, claimed the project was now estimated to cost $3.1 billion. Powell said he was not aware of that, and then when Trump produced a piece of paper to prove his accusations, Powell said, “You just added in a third building,” which had been completed five years ago. Trump has since fled to Scotland for a five-day golf boondoggle and to get away from the Epstein files.

Taking Stock

Wall Street closed mixed, but Trump’s latest Powell interaction and firmer US Treasury yields unnerved Asia traders, and the major indexes closed in the red. Hong Kong’s Hang Seng index fell 1.09%, Japan’s Topix lost 0.86%, and Australia’s ASX 200 fell 0.49%.

European bourses are dropping as well, and as of 5:40 a.m. PDT, the German DAX is down by 0.66 % while the UK FTSE 100 has lost 0.43%. The French CAC 40 index flat while S&P 500 futures are up 0.12%. Gold (XAUUSD) dropped from a peak of 3373.55 and is sitting at 3337.74. The US 10-year Treasury yield is 4.42%.

EURUSD

EURUSD is at the bottom of its 1.1716–1.1761 range. Yesterday, the single currency popped to 1.1789 on the heels of the ECB rate decision (unchanged) and President Christine Lagarde’s somewhat hawkish comments in her press conference where she described the Eurozone economy as resilient and doing better than expected. The focus shifted to the Fed and Trump, and EURUSD retreated. German Ifo data (Business Climate 88.6, Current Assessment 86.5, and Expectations 90.7) were a touch below forecasts but a non-issue for traders who are more cautious due to tariff concerns.

GBPUSD

GBPUSD is under pressure and trading in a 1.3428–1.3516 range, undermined by weak data and EURGBP demand as traders reduce bets for ECB rate cuts. Weak PMI data yesterday, soft consumer confidence, and slightly lower-than-expected retail sales data weighed on prices. UK Prime Minister Starmer is hoping to convince Trump to finalize tariffs on steel during Trump’s visit to Scotland.

USDJPY

USDJPY rallied from 146.82 to 147.94and is sitting near the top of that range in NY. The positive sentiment from the US/Japan trade deal is history, and traders are focused on inflation and next week’s BoJ meeting. Tokyo CPI, ex fresh food, rose 2.9% y/y (forecast 3.0% and previous 3.1%), which gives BoJ policymakers another excuse to delay hiking rates. JPMorgan analysts are predicting that the BoJ will raise inflation forecasts next week, which sets the stage for an October rate cut.

AUDUSD

AUDUSD fell in a 0.6555–0.6599 range due to a slight deterioration in global risk sentiment. Traders ignored news that Australia would allow US beef imports, but President Trump sure was. He tweeted, “Now, we are going to sell so much to Australia because this is undeniable and irrefutable proof that U.S. Beef is the Safest and Best in the entire World. Beef.” The president is obviously unaware that Australia is the second-largest beef exporter and the Americans are the largest consumer of US beef.

USDMXN

USDMXN traded sideways in a 18.5243–18.5855 range. President Claudia Sheinbaum said she was confident that Mexico would reach a trade deal with the US and avoid 30% tariffs. In addition, Mexico is holding talks with Brazil to expand its trade relationship.

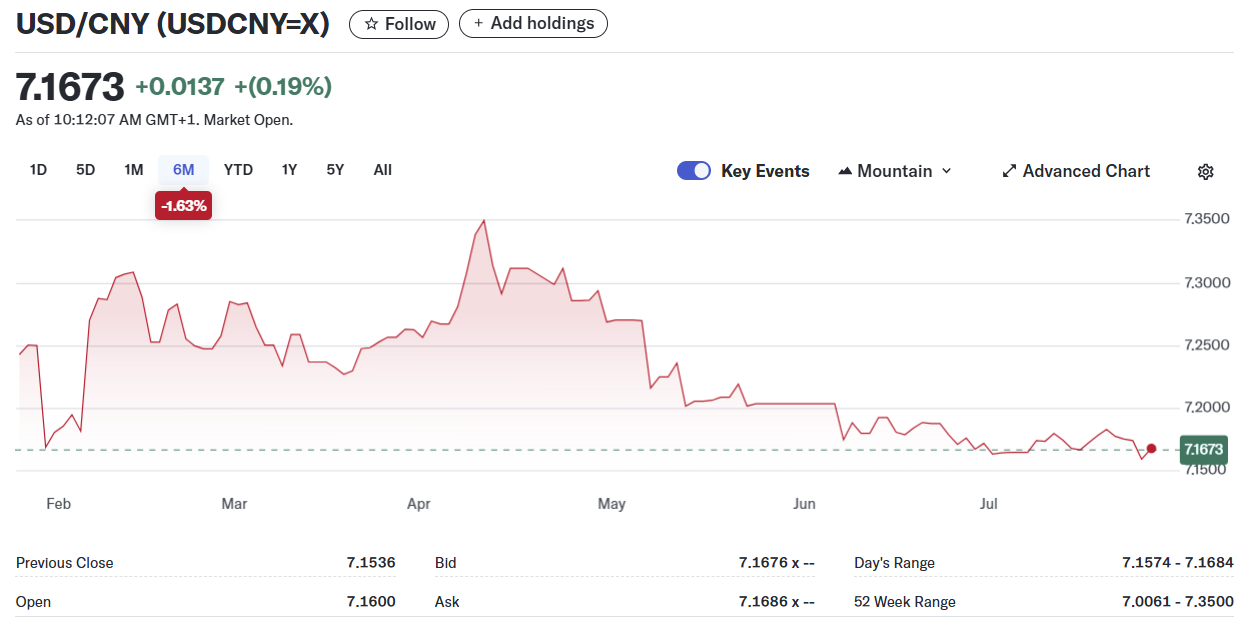

USDCNY

PBoC fix: 7.1419 vs exp. 7.1609 (Prev. 7.1385).

Shanghai Shenzhen 300 fell 0.53% to 4127.16.

US Treasury Secretary implied that US and China trade talks were proceeding well, saying, “We are in a pretty good place with China on trade.”

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau