Agility Forex Daily Commentary

August 5, 2025

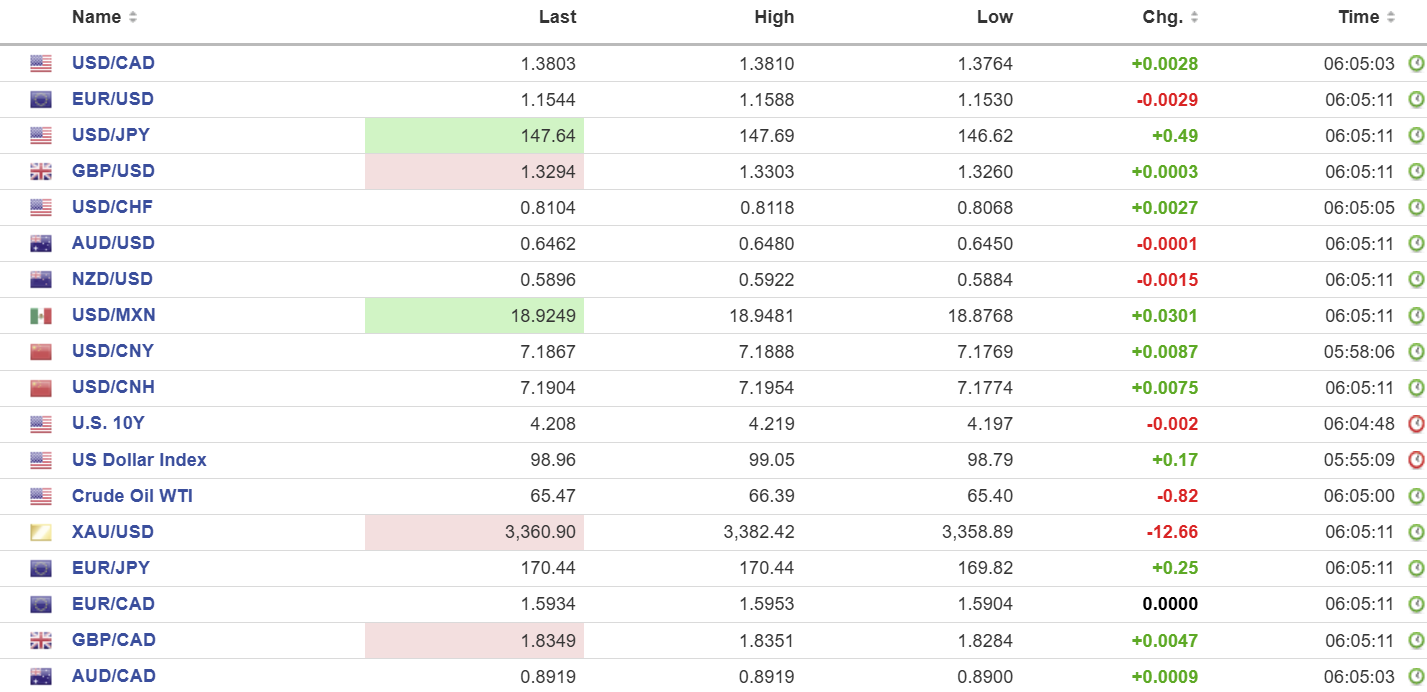

Tuesday USDCAD open 1.3803, overnight range 1.3764-1.3810, close 1.3780

Monday USDCAD open 1.3778, overnight range 1.3763-1.3881, close 1.3787.

USDCAD is consolidating Friday’s losses but with a bit of a bid. Now, a September 25 bp rate cut by the Fed is almost a sure thing which may light the path for timid Bank of Canada policymakers. The BoC will get fresh employment data on Friday (forecast 14,500) which should support further easing.

USDCAD is also underpinned by Trump’s tariff hike to 35%. Although the increase reportedly only impacts 10% of Canadian exports, just because the US Mexico Canada Agreement on trade is in effect, it doesn’t mean Trump can’t unilaterally void it.

WTI oil dropped from 69.58 Friday to 65.40 overnight and are 65.56 in NY. Opec’s decision to boost production by 547,000 bpd beginning September more than offset talk that Trump’s threatened tariff increase on India would curb its purchases of Russian crude.

Canada’s trade deficit iin June was as expected at $5.8 billion while the US trade deficit narrowed to $60.2 billion from $71.5 b.

ISM services PMI is expected to be 51.5 compared to 50.8.

USDCAD Technical Outlook:

The intraday technicals are bullish above 1.3760 looking for a break above 1.3820 to retest resistance in the 1.3870 area. A move below 1.3760 targets 1.3610.

Longer term, USDCAD is bullish but needs a sustained break above the 100 day moving average resistance at 1.3847 or risk further consolidation in a 1.3680-1.3870 band. Furthermore, the downtrend from March remains intact while prices are below 1.3900.

For today, USDCAD support is 1.3760 and 1.3730. Resistance is 1.3840 and 1.3870. Today’s Range: 1.3770-1.3870

Wall of Noise

Welcome back, Canada. While you were away, Friday’s drama became Monday’s comedy with Wall Street recovering its post-NFP losses. Traders believe a Fed rate cut to 42.5% in September is close to a sure thing, followed by another rate cut before year-end. San Francisco Fed President Mary Daly agrees, saying yesterday that “two rate cuts is appropriate.”

Trump was apoplectic with the Bureau of Labor Statistics nonfarm payrolls revisions. How dare they report that the job market was far weaker than they previously stated? The number of new jobs reported in May and June was revised lower by 258,000, a sure sign that Trump’s tariff policies were hurting workers. Trump howled, “In my opinion, today’s Jobs Numbers were RIGGED in order to make the Republicans, and ME, look bad.”

It is the start of the “Chinafication of Stats,” where economic data is skewed to favourably support the President’s agenda lest the statisticians get fired or receive a visit from ICE.

Trump went after India and Switzerland. He said he would substantially raise tariffs on India for buying Russian oil. He levied a 39% tariff on Switzerland because of its massive trade surplus, all due to US purchases of gold bullion.

Today, the focus is back on Trump and who he will nominate to replace Fed Governor Adrian Kugler, who resigned Friday, and BLS Head Erika McEntarfer, who he fired Friday.

Taking Stock

Asian equity traders followed Wall Street’s lead from Monday and closed with gains across the board. Australia’s ASX 200 closed up 1.23%, Japan’s Topix rose 0.70%, and Hong Kong’s Hang Seng gained 0.68%.

European traders are adding to Monday’s gains, with the German Dax rising 0.76%, the UK FTSE 100 climbing 0.37%, and the French CAC 40 posting a 0.24% gain. S&P 500 futures are up 0.15%, while the US 10-year Treasury yield is steady at 4.210%. The US dollar index traded sideways in a 98.16–99.14 range yesterday and today. Gold (XAUUSD) is sitting at its session low of 3364.85 as of 5:40 am PDT

EURUSD

EURUSD consolidated Friday’s NFP gains in a 1.1530–1.1588 range. Services PMI was a tad weaker than expected (actual 51 vs forecast 51.2 and June 51.2), but the news was largely offset by better-than-forecast Composite PMI, which was 50.6 compared to 50.3 in June. The uptrend line from February remains intact while prices are above 1.1370.

GBPUSD

GBPUSD drifted aimlessly in a 1.3260–1.3303 range, supported by broad US dollar weakness on Fed rate cut speculation and caution ahead of Thursday’s Bank of England meeting. A 25 bp rate cut is largely priced in, but additional rate cuts are still debatable. UK Services and Composite PMI readings were firmer than expected (51.5 and 51.8, respectively), which also underpinned prices.

USDJPY

USDJPY is consolidating post-NFP losses in a 146.62–147.77 range, and prices are at the top of that band in NY. The steep plunge in the US 10-year Treasury yield from 4.41% pre-NFP to 4.212% today is pressuring prices. The BoJ minutes from the end-of-July meeting showed policymakers were concerned by rising inflation but handcuffed by tariff uncertainty.

AUDUSD

AUDUSD is at the top of its 0.6459–0.6480 range in NY due to US dollar weakness on Fed rate cut speculation. Gains are limited due to rising risks of RBA rate cuts because of Australia’s soft economic growth data and declining inflation. Australian Services PMI was 54.1 compared to expectations and the June reading of 53.8.

USDMXN

USDMXN traded choppily but with a bid in a 18.8768–18.9481 range as US dollar weakness from increased odds of Fed rate cuts clashes with expectations for a 25 bp Banxico rate cut on Thursday. Mexico also reported that incoming remittances fell by 16.2% y/y in June.

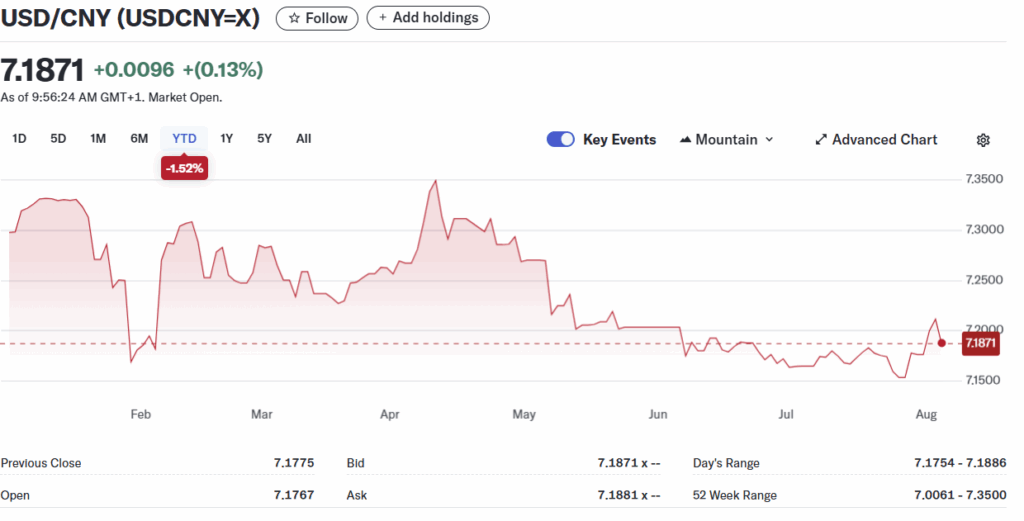

USDCNY

Monday: PBoC fix: 7.1496 vs exp. 7.2033 (Prev. 7.1494).

Tuesday: PBoC fix: 7.1366 vs exp. 7.1667 (Prev. 7.1395)

Monday: The Shanghai Shenzhen CSI 300 rose 0.39% to 4070.70

Tuesday: The Shanghai Shenzhen CSI 300 rose 0.80% to 4103.45

Chinese July S&P Services PMI 52.6 vs. expected 50.4 and previous 50.6).

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics